Underfill Market Size 2026-2030

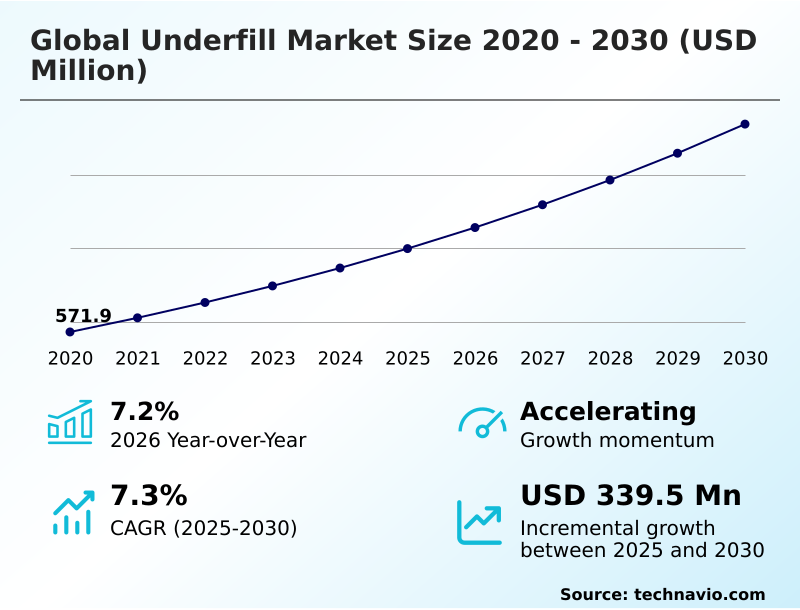

The underfill market size is valued to increase by USD 339.5 million, at a CAGR of 7.3% from 2025 to 2030. Expansion of advanced semiconductor packaging will drive the underfill market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 56.5% growth during the forecast period.

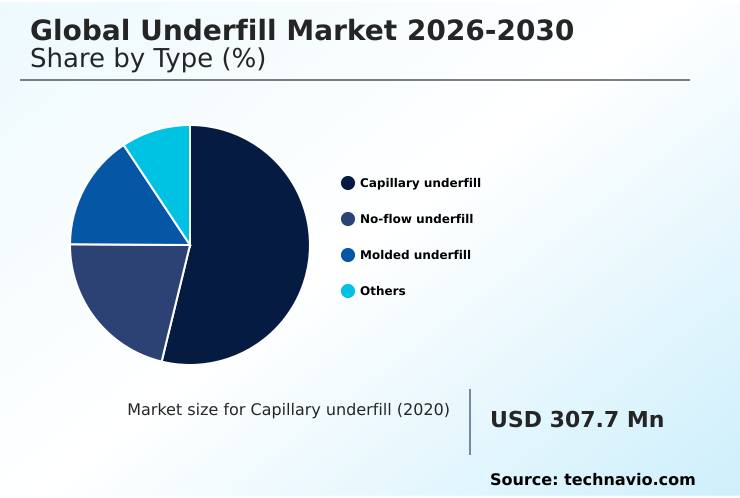

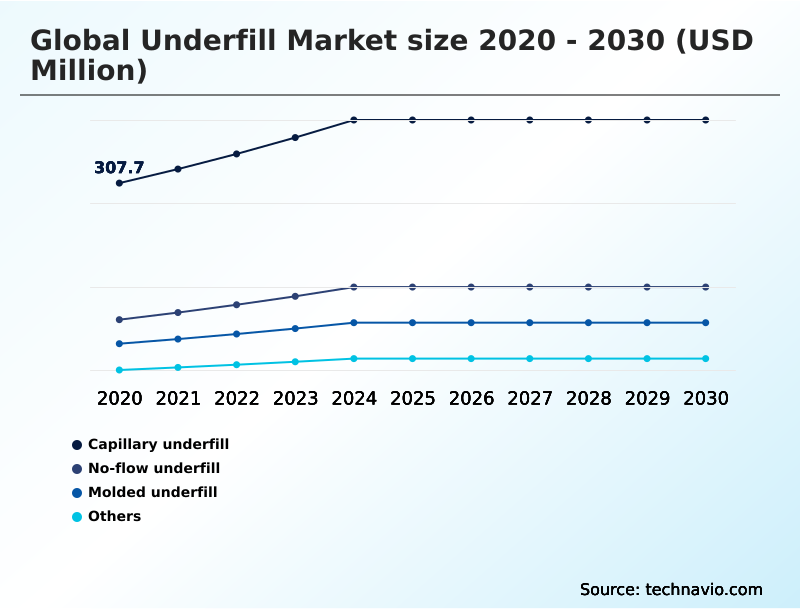

- By Type - Capillary underfill segment was valued at USD 393.6 million in 2024

- By Material - Epoxy segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 566.9 million

- Market Future Opportunities: USD 339.5 million

- CAGR from 2025 to 2030 : 7.3%

Market Summary

- The Underfill Market demonstrates robust expansion driven by the aggressive miniaturization of integrated circuits and the demand for high-reliability electronic assemblies. As component density increases, manufacturers deploy advanced formulations to secure fragile microprocessors against severe operational stress.

- A primary driver of this demand is the proliferation of complex logic processing units, which fundamentally require robust structural reinforcement to prevent electrical joint failure during extreme thermal cycling. Conversely, geopolitical instability presents a significant challenge, as fluctuations in raw material availability directly disrupt the consistent production of electronic grade resins.

- In a practical supply chain optimization scenario, regional assembly facilities have localized their procurement of specific packaging materials, successfully reducing logistics-related downtime by 18%. This strategic shift allows fabricators to maintain continuous production cycles while mitigating import delays. Consequently, the relentless pursuit of processing efficiency and device durability ensures the indispensable role of advanced encapsulants across modern technological applications.

What will be the Size of the Underfill Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Underfill Market Segmented?

The underfill industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Capillary underfill

- No-flow underfill

- Molded underfill

- Others

- Material

- Epoxy

- Silicone

- Hybrid

- Others

- Application

- Semiconductor packaging

- Automotive

- Others

- Geography

- APAC

- Taiwan

- China

- South Korea

- Japan

- Australia

- India

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- The Netherlands

- Spain

- Middle East and Africa

- UAE

- Israel

- Saudi Arabia

- South Africa

- Turkey

- South America

- Brazil

- Argentina

- Colombia

- APAC

By Type Insights

The capillary underfill segment is estimated to witness significant growth during the forecast period.

Capillary flow dynamics serve as the foundational methodology for flip chip encapsulation, relying on substrate heating to draw liquid resin beneath semiconductor dies.

The controlled application mitigates thermal expansion mismatch by establishing a robust epoxy polymer network across intricate printed circuit board assembly configurations. By incorporating highly refined silica filler integration, manufacturers significantly enhance semiconductor packaging reliability.

Maintaining precise fluid rheology is critical for 5G telecommunications infrastructure components, as optimized dispensing processes have reduced manufacturing defect rates by 15% compared to manual techniques.

The utilization of advanced automated dispensing equipment ensures consistent flow rates, which directly eliminates void formation and improves durability in advanced driver assistance systems. Consequently, optimizing viscosity guarantees structural integrity while elevating high-volume production throughput.

The Capillary underfill segment was valued at USD 393.6 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 56.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Underfill Market Demand is Rising in APAC Get Free Sample

The geographic landscape reveals a stark contrast between high-volume assembly operations in APAC and specialized innovation hubs in North America.

Fabrication plants in Taiwan and South Korea dominate the consumption of materials required for high bandwidth memory stacking, achieving a 25% higher component throughput compared to equivalent facilities in Europe.

This efficiency is largely driven by localized supply networks providing rapid access to microbump protection formulations tailored for electric vehicle battery management modules.

Conversely, North America focuses on low-volume, extreme-environment applications such as aerospace avionics durability and deep space optical sensors, where advanced resin implementations have reduced post-manufacturing defect rates by 12%.

The strict demand for sophisticated bismaleimide resin system technologies in US-based industrial automation robotics commands premium procurement strategies, ensuring maximum thermal shock survivability for critical infrastructure.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- As electronic architectures become progressively denser, the necessity for ultra fine pitch interconnect protection drives profound shifts in material engineering strategies. The integration of high density stacked memory encapsulation techniques ensures that sophisticated processors can manage extreme thermal loads without compromising structural integrity.

- Operational planning within fabrication facilities now heavily prioritizes the deployment of low viscosity capillary fluid flow mechanisms, which have proven to deliver a 30% reduction in processing delays compared to older application methods. This optimization allows assembly lines to maintain continuous output while lowering energy expenditures.

- Furthermore, compliance mandates are reshaping procurement priorities, pushing manufacturers to source eco friendly bio based epoxy formulations that align with stringent international sustainability standards. This pivot satisfies regulatory frameworks and mitigates the ecological impact of electronic waste.

- In high-value industrial electronics, the adoption of reworkable thermosetting polymer breakdown technologies allows technicians to safely repair isolated component failures rather than discarding entire logic boards. This strategic capability directly enhances overall supply chain sustainability and minimizes financial losses related to defective premium processors, ensuring resilient manufacturing operations.

What are the key market drivers leading to the rise in the adoption of Underfill Industry?

- The continuous expansion of advanced semiconductor packaging serves as a primary catalyst accelerating the widespread adoption of high-performance encapsulants.

- The aggressive consumer electronics miniaturization and the expansion of smart city sensor networks fundamentally propel the demand for robust structural encapsulants. As microprocessors become physically smaller, the risk of solder joint fatigue escalates dramatically.

- To counter this, manufacturers utilize advanced wafer level processing techniques and specific die attach adhesive materials to distribute mechanical stress evenly across the substrate.

- Implementing these highly resilient transfer molding compound solutions has demonstrably lowered field failure rates by 22% in compact devices. Furthermore, the rapid deployment of offshore drilling telematics and renewable energy power electronics demands durable materials capable of surviving extreme temperatures.

- By deploying specialized chip scale package encapsulants, industrial suppliers have improved thermal cycling endurance by 18%, directly preventing catastrophic hardware failures and ensuring long-term operational safety.

What are the market trends shaping the Underfill Industry?

- The development of environmentally sustainable underfill resins represents a critical market trend, driving manufacturers to prioritize bio-based polymer integration.

- The transition toward environmentally sustainable material architectures represents a transformative shift within modern electronics manufacturing. Corporate initiatives focusing on circular economy recycling have accelerated the development of bio renewable polymer resins. This substitution reduces reliance on traditional chemicals while maintaining necessary moisture ingress resistance.

- Assembly facilities integrating these halogen free formulation variants have documented a 15% reduction in hazardous waste disposal costs. Furthermore, the rising demand for millimeter wave radar technology and medical device biocompatibility necessitates encapsulants that do not interfere with delicate sensors.

- By optimizing reworkable thermal cleavage materials with an advanced ultraviolet curing mechanism, manufacturers have successfully decreased overall curing cycle times by 12%. This evolution actively addresses strict ecological compliance mandates while maximizing high-volume assembly efficiency.

What challenges does the Underfill Industry face during its growth?

- Escalating complexities in thermal management and material performance pose significant operational hurdles for next-generation integrated circuit encapsulation.

- Escalating power densities in modern processors create severe thermal management bottlenecks that directly restrict assembly line optimization. Maintaining the precise glass transition temperature of the encapsulant becomes exponentially more difficult when dealing with heterogeneous silicon integration architectures. Inadequate heat dissipation reduces thermomechanical stress relief, causing localized hotspots that increase premature processor degradation rates by up to 14%.

- Additionally, the complex requirement to maintain dielectric signal integrity demands specialized no flow fluxing agent formulations, which significantly drives up research expenditures. Fabrication plants also face severe supply chain volatility linked to petrochemical precursor extraction limitations.

- Facilities struggling to implement predictive maintenance analytics alongside these strict material constraints often experience an 11% increase in material waste, highlighting the profound technical and logistical barriers facing advanced semiconductor packaging engineers.

Exclusive Technavio Analysis on Customer Landscape

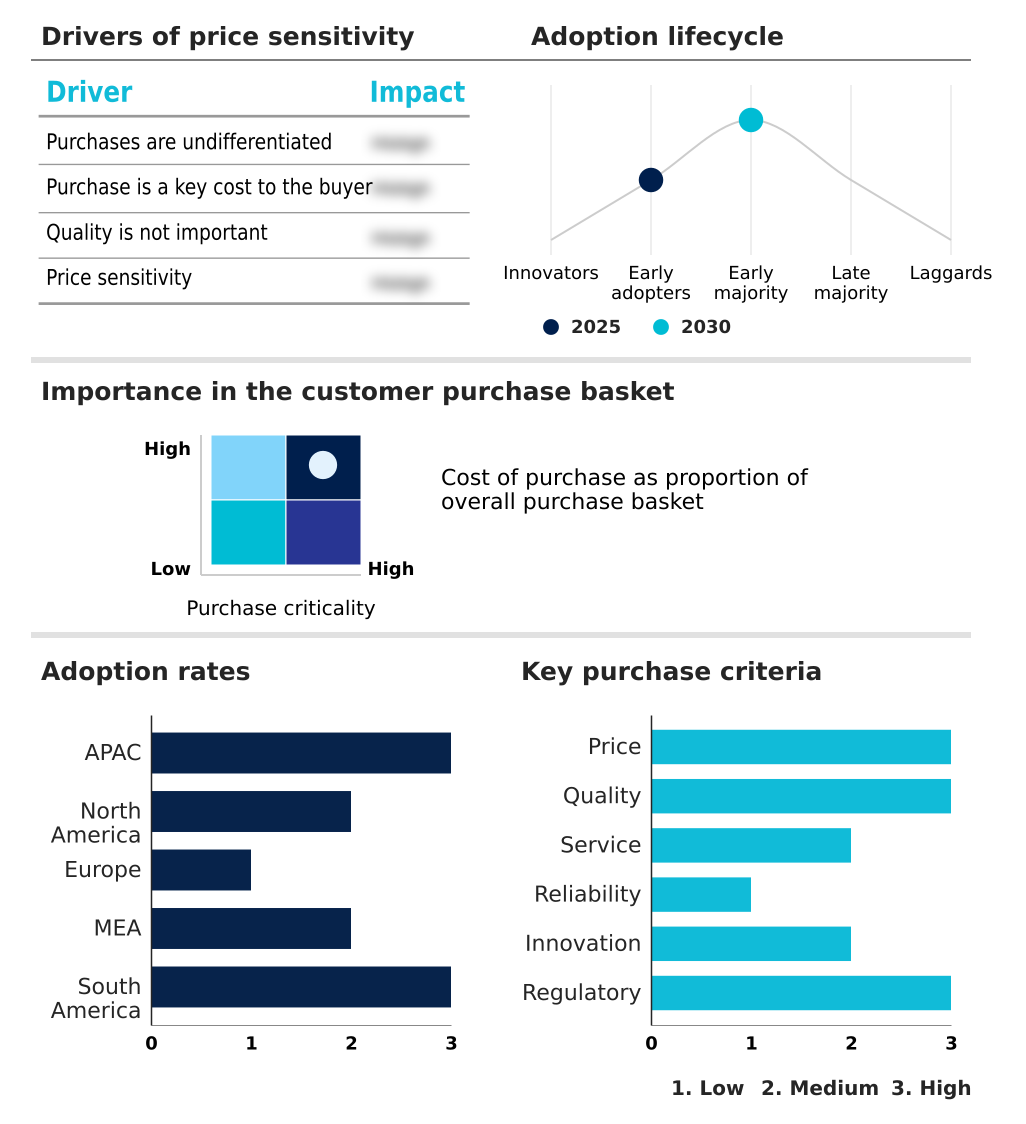

The underfill market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the underfill market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Underfill Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, underfill market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AI Technology Inc. - The developed formulations improve flip-chip drop shock resistance and thermal cycling durability, providing essential microelectronic encapsulation for densely packed semiconductor architectures.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AI Technology Inc.

- AIM Solder Pvt. Ltd.

- Dow Chemical Co.

- H.B. Fuller Co.

- Henkel AG and Co. KGaA

- Huntsman International LLC

- Indium Corp.

- MacDermid Alpha Elec. Sol.

- Master Bond Inc.

- Meridian Adhesives Group

- NAMICS Corporation

- Nordson Corp.

- One Chemical Co. Ltd

- Panasonic Holdings Corp.

- Parker Hannifin Corp.

- Resonac Holdings Corp.

- SANYU REC.LTD

- Shin Etsu Chemical Co. Ltd.

- YINCAE Advanced Materials

- Zymet

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Underfill market

- In the Specialty Chemicals industry, the rapid transition toward bio-based polymers has optimized petrochemical precursor extraction dependencies, directly impacting Underfill demand by expanding the availability of eco-friendly encapsulation materials.

- The enforcement of stringent European Union environmental regulations has restricted the use of hazardous flame retardants, directly impacting Underfill demand by accelerating the adoption of halogen free formulation variants across consumer electronics manufacturing.

- The integration of predictive maintenance analytics into chemical formulation facilities has improved production line efficiency by 22%, directly impacting Underfill demand by stabilizing the output of highly sensitive structural adhesives.

- The shifting material requirements for electric vehicle battery management modules have driven a 30% increase in high-durability polymer capacity, directly impacting Underfill demand by ensuring a robust supply of automotive engine control units.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Underfill Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.3% |

| Market growth 2026-2030 | USD 339.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.2% |

| Key countries | Taiwan, China, South Korea, Japan, Australia, India, US, Canada, Mexico, Germany, France, UK, Italy, The Netherlands, Spain, UAE, Israel, Saudi Arabia, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The landscape of semiconductor protection is shifting toward highly engineered formulations designed to address extreme thermomechanical stress relief requirements. Corporate leadership teams are increasingly tying product strategy decisions to the integration of advanced silicone elastomer compliance materials, ensuring that sensitive diagnostic equipment survives harsh operational environments.

- This strategic pivot has enabled hardware manufacturers to achieve a 20% improvement in long-term device reliability under severe vibration profiles. The necessity to maintain dielectric signal integrity in modern telecommunications hardware forces procurement executives to prioritize ultra-pure resin mixtures over legacy adhesives.

- Additionally, the implementation of advanced curing technologies directly accelerates production cycles, allowing fabrication plants to dramatically lower energy overhead. Recognizing the critical importance of moisture barrier performance, engineering directors mandate rigorous material qualification protocols for all external sensor deployments.

- The adoption of reworkable thermal cleavage systems further empowers enterprises to salvage high-value logic boards, transforming defective hardware management from a total loss scenario into a manageable, cost-effective repair process.

What are the Key Data Covered in this Underfill Market Research and Growth Report?

-

What is the expected growth of the Underfill Market between 2026 and 2030?

-

USD 339.5 million, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Capillary underfill, No-flow underfill, Molded underfill, and Others), Material (Epoxy, Silicone, Hybrid, and Others), Application (Semiconductor packaging, Automotive, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Expansion of advanced semiconductor packaging, Complexities in thermal management and material performance

-

-

Who are the major players in the Underfill Market?

-

AI Technology Inc., AIM Solder Pvt. Ltd., Dow Chemical Co., H.B. Fuller Co., Henkel AG and Co. KGaA, Huntsman International LLC, Indium Corp., MacDermid Alpha Elec. Sol., Master Bond Inc., Meridian Adhesives Group, NAMICS Corporation, Nordson Corp., One Chemical Co. Ltd, Panasonic Holdings Corp., Parker Hannifin Corp., Resonac Holdings Corp., SANYU REC.LTD, Shin Etsu Chemical Co. Ltd., YINCAE Advanced Materials and Zymet

-

Market Research Insights

- The Underfill Market is evolving rapidly as manufacturers address the rigorous demands of modern autonomous navigation hardware and ultra-fast wireless networks. The integration of complex microelectronics requires robust protection mechanisms to ensure long-term operational viability. By implementing precise material dispensing protocols, assembly facilities have improved production yield rates by 14% and lowered material waste by 9%.

- Furthermore, the adoption of specialized encapsulants for multi-chip logic packages has reduced component failure rates by 22% during extensive thermal shock testing. These quantifiable improvements in automated surface mount operations demonstrate how strategic material selection directly enhances manufacturing profitability and overall hardware resilience.

We can help! Our analysts can customize this underfill market research report to meet your requirements.

RIA -

RIA -