APAC Plasterboard Market Size 2026-2030

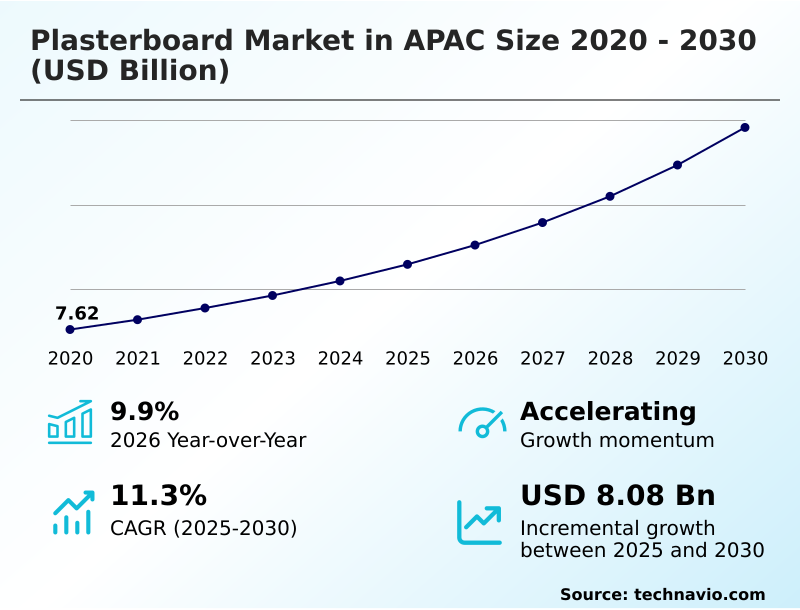

The apac plasterboard market size is valued to increase by USD 8.08 billion, at a CAGR of 11.3% from 2025 to 2030. Rapid urbanization and infrastructure development will drive the apac plasterboard market.

Major Market Trends & Insights

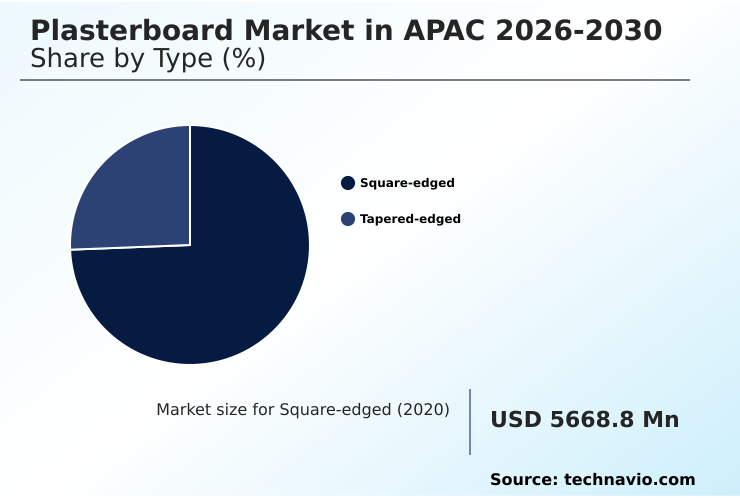

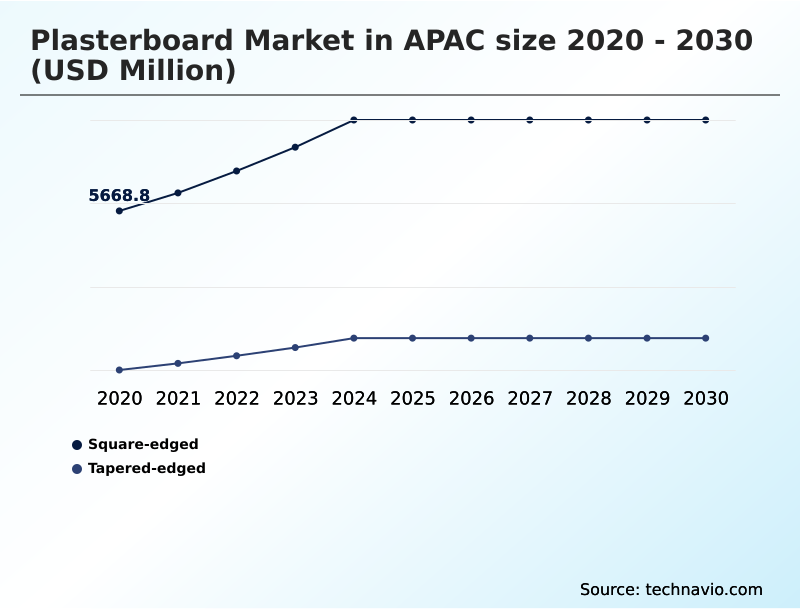

- By Type - Square-edged segment was valued at USD 7.79 billion in 2024

- By End-user - Residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 11.93 billion

- Market Future Opportunities: USD 8.08 billion

- CAGR from 2025 to 2030 : 11.3%

Market Summary

- The Plasterboard Market in APAC is defined by a rapid transition from traditional wet masonry to advanced dry construction techniques. Escalating urban migration acts as a primary driver, compelling real estate developers to utilize dry-lining installation because it accelerates project delivery schedules significantly.

- Conversely, fluctuating energy costs required for calcination thermal inputs create a persistent challenge, forcing producers to optimize operational overheads to maintain profitability. In a practical supply chain scenario, manufacturers are aggressively integrating synthetic chemical gypsum to mitigate raw material scarcity, a strategy that has reduced aggregate production costs by 15% compared to relying strictly on imported natural minerals.

- This operational shift directly supports circular economy compliance by repurposing industrial waste. The continuous adoption of automated building information systems further enhances on-site efficiency, streamlining panel layout procedures. As institutional architecture increasingly mandates uncombustible structural barriers and specialized moisture-resistant treatment, the structural dependence on high-performance technical plasterboard deepens, effectively transforming regional infrastructure protocols.

What will be the Size of the APAC Plasterboard Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the APAC Plasterboard Market Segmented?

The apac plasterboard industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Square-edged

- Tapered-edged

- End-user

- Residential

- Non-residential

- Product type

- Fire-resistant plasterboard

- Impact-resistant plasterboard

- Others

- Geography

- APAC

- China

- Australia

- Japan

- South Korea

- APAC

By Type Insights

The square-edged segment is estimated to witness significant growth during the forecast period.

Square-edged plasterboard panel adoption directly influences the operational speed of the Plasterboard Market in APAC. Because these panels offer direct edge-to-edge load distribution without secondary wet trades elimination, contractors utilize them heavily for foundational interior space partitioning.

This straightforward design simplifies the alignment process, thereby improving installation speed by 22% compared to traditional masonry. High-density structural gypsum is often utilized to ensure robust performance across budget-conscious institutional projects.

Furthermore, substituting carbon-heavy material substitution with lightweight prefabricated components drives efficiency in high-rise load reduction. By utilizing synthetic chemical gypsum sourced as a flue-gas desulfurization byproduct, manufacturers enhance circular economy compliance.

This dynamic lowers overall material scrap rates and optimizes raw material procurement within automated manufacturing automation workflows, shaping segment growth.

The Square-edged segment was valued at USD 7.79 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

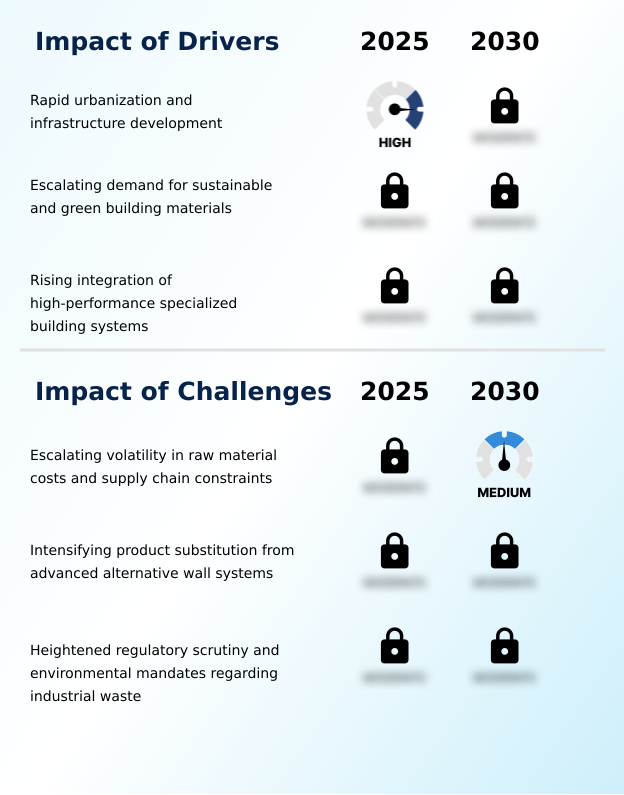

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolving architecture of the Plasterboard Market in APAC necessitates highly specialized components to address complex structural and environmental challenges. As urban densification pushes commercial structures vertically, the deployment of fire resistant high rise partition systems has become non-negotiable for achieving stringent building safety compliance.

- These robust systems utilize a fire-resistant core formulation that demonstrably outperforms standard masonry by reducing heat transfer rates by over 40%, a critical factor in emergency risk mitigation. Concurrently, the rising demand for premium commercial and hospitality spaces drives the specification of high performance acoustic plasterboard panels, which effectively suppress noise transmission across adjacent interior environments.

- To optimize manufacturing sustainability, producers are rapidly transitioning toward flue gas desulfurization synthetic gypsum, a strategy that lowers reliance on raw mining and aligns with progressive ecological mandates. The integration of automated robotic drywall layout devices further revolutionizes on-site logistics by translating complex digital blueprints into precise floor mappings, cutting material scrap by a significant margin.

- Additionally, the development of moisture resistant coastal construction materials incorporates advanced fiberglass reinforcement mesh and specialized water-repellent treatments, preventing structural degradation in humid regional zones. This holistic advancement across material science and installation technology ensures that modern drywall configurations deliver unmatched durability and operational efficiency.

What are the key market drivers leading to the rise in the adoption of APAC Plasterboard Industry?

- Rapid urbanization and large-scale infrastructure development serve as the primary catalysts driving high-volume consumption of lightweight interior wall systems.

- Severe urban migration and strict green building certifications act as foundational drivers propelling the Plasterboard Market in APAC.

- Because traditional wet plastering cannot meet the aggressive timelines of modern infrastructure megaprojects, developers prioritize lightweight prefabricated components that drastically accelerate rapid project execution.

- This shift allows construction firms to lower on-site labor costs by 24% and decrease structural load engineering expenses by 15%. Furthermore, strict environmental protection protocols are forcing carbon-heavy material substitution.

- Manufacturers utilize synthetic chemical gypsum derived from industrial emissions, which reduces reliance on domestic mineral extraction. This sustainable raw material procurement strategy lowers manufacturing energy use by 12% by optimizing calcination thermal inputs.

- Consequently, compliance transitions from a structural hurdle into a primary catalyst for technological innovation.

What are the market trends shaping the APAC Plasterboard Industry?

- An accelerating transition toward factory-finished and pre-decorated panels represents a primary trend reshaping modern dry construction methodologies.

- The widespread integration of pre-decorated panel lamination and digital twin spatial mapping represents a massive technological shift within the Plasterboard Market in APAC. Because severe skilled labor shortages inflate construction overheads, contractors are rapidly adopting factory-finished boards that bypass secondary wet trades elimination. This operational pivot reduces overall project downtime by 35% and improves installation forecast accuracy by 18%.

- The effect is profoundly lucrative for high-speed commercial office retrofits, where rapid project handover directly equates to accelerated corporate revenue generation. Furthermore, utilizing automated building information systems allows for precise millimeter accuracy pre-cutting in controlled off-site environments. This eliminates on-site guesswork, driving a 20% reduction in material scrap.

- Consequently, modern drywall installation transitions from a manual craft into a highly predictable, technology-driven assembly process that maximizes job-site installer productivity and architectural aesthetic requirements.

What challenges does the APAC Plasterboard Industry face during its growth?

- Escalating volatility in core raw material costs and intensifying supply chain constraints present significant operational hurdles for regional manufacturers.

- Escalating volatility in maritime freight logistics and intensifying product substitution severely constrain the Plasterboard Market in APAC. Because regional coal-fired power plants are phasing out, the domestic supply of flue-gas desulfurization byproduct is declining, forcing manufacturers to rely heavily on imported natural minerals.

- This supply chain disruption drives up landed feedstock pricing, squeezing profit margins for regional producers and inflating raw material procurement costs by 22% compared to historical averages. Concurrently, high-durability substitutes like alternative fiber cement and magnesium oxide substitution are eroding market share in high-humidity zones.

- Because these alternatives offer superior immunity to water damage, buyers frequently opt against standard panels, compelling manufacturers to invest heavily in moisture-resistant treatment to remain competitive.

Exclusive Technavio Analysis on Customer Landscape

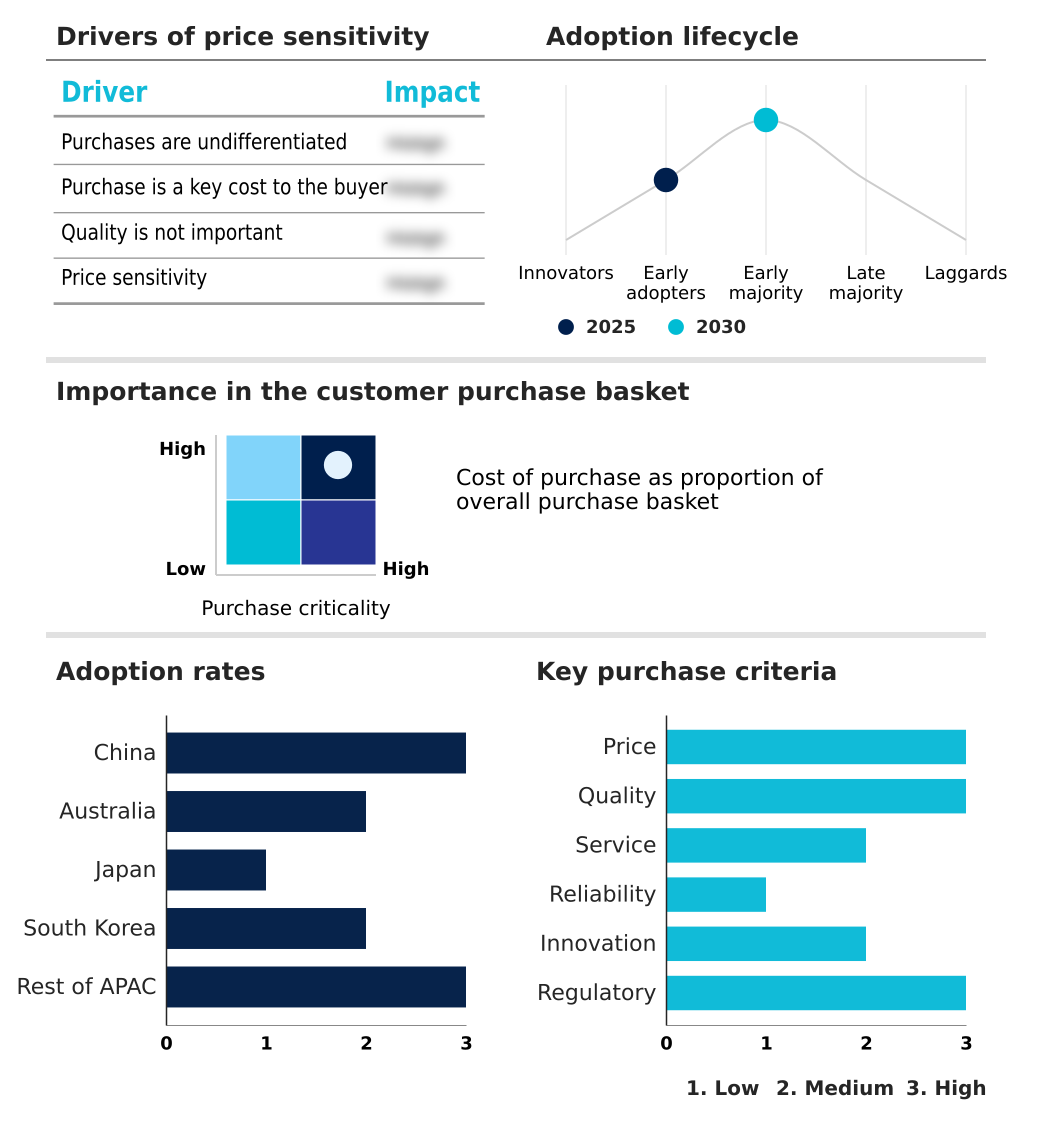

The apac plasterboard market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the apac plasterboard market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of APAC Plasterboard Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, apac plasterboard market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Beijing New Building Materials - The vendor provides advanced plasterboard systems engineered for superior fire resistance, thermal insulation, and acoustic performance, supporting lightweight construction and modern interior drywall partitioning applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Beijing New Building Materials

- BGC Australia Pty Ltd

- Chiyoda Ute Co. Ltd.

- Compagnie de Saint Gobain SA

- CSR Gyprock

- Etex Building Performance N.V.

- Etex NV

- Gypsemna Co. LLC

- Holcim Ltd.

- India Gypsum Pvt. Ltd.

- Jason Gypsum Board China Co

- KCC Co. Ltd.

- Knauf Digital GmbH

- National Gypsum Co.

- SCG International Corp Co. Ltd.

- Siam-Indo Gypsum Industry

- Thai Gypsum Product Pcl

- USG Corp.

- Yoshino Gypsum Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Apac plasterboard market

- In the Building Products industry, stringent green building certifications mandating a 30% reduction in carbon emissions have accelerated carbon-heavy material substitution, directly increasing Plasterboard demand for eco-friendly lightweight prefabricated components.

- The widespread adoption of automated building information systems by commercial contractors has optimized interior space partitioning layouts, improving millimeter accuracy pre-cutting workflows and subsequently reducing Plasterboard material waste by 18%.

- Elevated maritime freight logistics costs and raw material procurement bottlenecks have forced a structural shift toward domestic mineral extraction, impacting Plasterboard supply chains and driving the usage of synthetic chemical gypsum.

- Stringent healthcare hygiene compliance standards requiring uncombustible structural barriers have prompted manufacturers to upgrade drywall surface finish capabilities, elevating the consumption of specialized Plasterboard systems with multi-layered composite system profiles.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled APAC Plasterboard Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 200 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.3% |

| Market growth 2026-2030 | USD 8081.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.9% |

| Key countries | China, Australia, Japan, South Korea and Rest of APAC |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Plasterboard Market in APAC undergoes continuous structural evolution driven by the necessity for rapid dry-lining installation and sophisticated thermal management properties. Manufacturers are fundamentally altering product strategies by incorporating heavy-grade liner paper and specialized crystalline chemical additives to meet rigorous safety mandates.

- This strategic shift directly supports boardroom-level compliance initiatives, as adopting pre-engineered modular assemblies ensures adherence to stringent fire and acoustic regulations. Consequently, contractors utilizing these advanced multi-layered composite system configurations have achieved a 30% reduction in processing time during large-scale hospitality refurbishment cycles.

- The critical mitigation of hydrogen sulfide mitigation during anaerobic waste decomposition forces enterprises to invest in robust closed-loop recycling infrastructure, driving long-term ecological sustainability. By leveraging pre-decorated panel lamination, installation crews entirely bypass secondary finishing phases, establishing monolithic surface integration that satisfies premium aesthetic demands.

- Furthermore, enhanced volatile organic compound control within these panels improves indoor air quality, a metric increasingly demanded by modern healthcare hygiene compliance protocols.

What are the Key Data Covered in this APAC Plasterboard Market Research and Growth Report?

-

What is the expected growth of the APAC Plasterboard Market between 2026 and 2030?

-

USD 8.08 billion, at a CAGR of 11.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Square-edged, and Tapered-edged), End-user (Residential, and Non-residential), Product Type (Fire-resistant plasterboard, Impact-resistant plasterboard, and Others) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Rapid urbanization and infrastructure development, Escalating volatility in raw material costs and supply chain constraints

-

-

Who are the major players in the APAC Plasterboard Market?

-

Beijing New Building Materials, BGC Australia Pty Ltd, Chiyoda Ute Co. Ltd., Compagnie de Saint Gobain SA, CSR Gyprock, Etex Building Performance N.V., Etex NV, Gypsemna Co. LLC, Holcim Ltd., India Gypsum Pvt. Ltd., Jason Gypsum Board China Co, KCC Co. Ltd., Knauf Digital GmbH, National Gypsum Co., SCG International Corp Co. Ltd., Siam-Indo Gypsum Industry, Thai Gypsum Product Pcl, USG Corp. and Yoshino Gypsum Co. Ltd.

-

Market Research Insights

- Rapid project execution protocols define the Plasterboard Market in APAC, fundamentally altering interior space partitioning strategies. By prioritizing lightweight prefabricated components, contractors have increased daily installation output by 28% compared to conventional brickwork. This structural shift supports high-rise load reduction, driving a 15% decrease in foundational engineering costs for major commercial office retrofits.

- Furthermore, advanced raw material procurement strategies targeting alternative synthetic supplies have improved supply chain resilience by 22%, mitigating exposure to maritime freight logistics delays. The elimination of secondary wet trades through pre-finished panels ensures faster project handover, directly enhancing operational ROI and aligning with modern architectural aesthetic requirements.

We can help! Our analysts can customize this apac plasterboard market research report to meet your requirements.

RIA -

RIA -