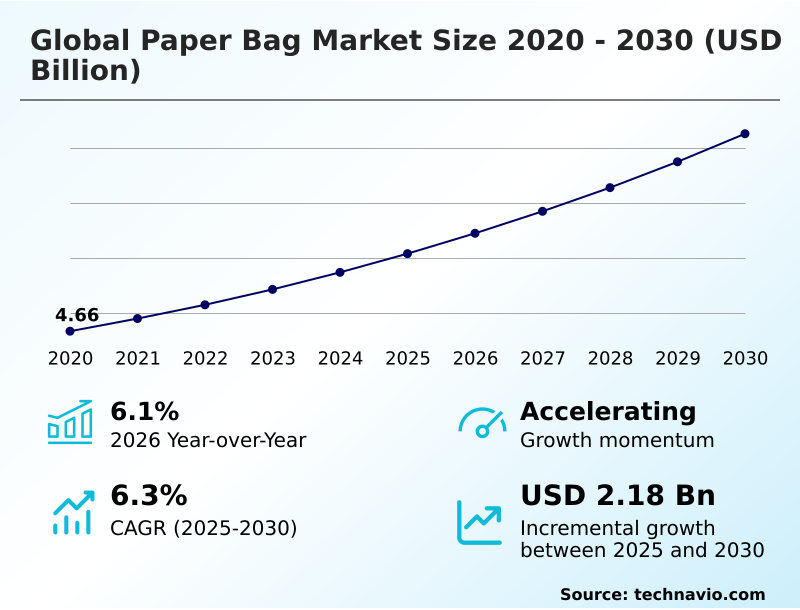

Paper Bag Market Size 2026-2030

The paper bag market size is valued to increase by USD 2.18 billion, at a CAGR of 6.3% from 2025 to 2030. Stringent government regulations and legislative frameworks enforcing eradication of single-use plastic packaging will drive the paper bag market.

Major Market Trends & Insights

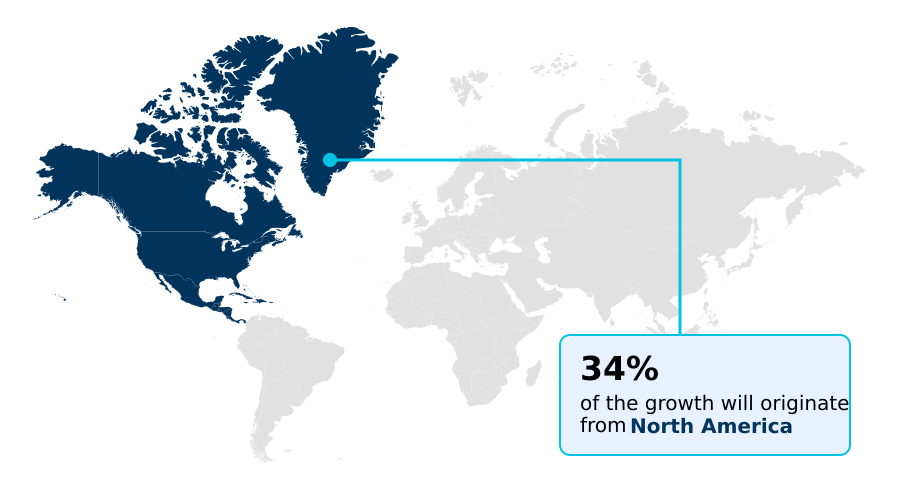

- North America dominated the market and accounted for a 34% growth during the forecast period.

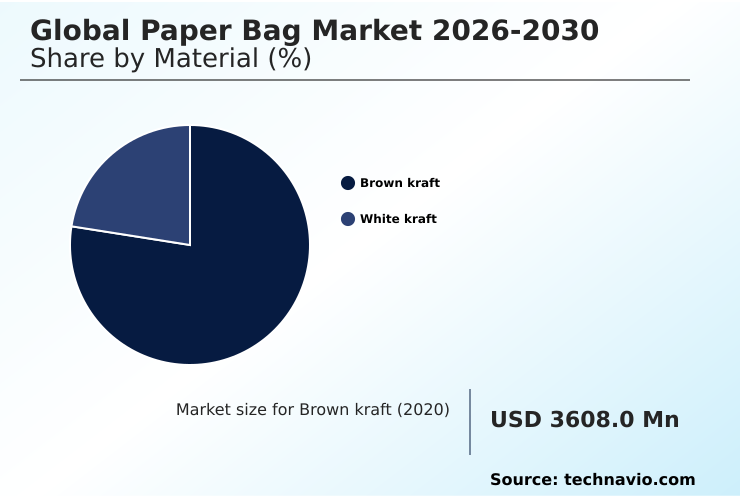

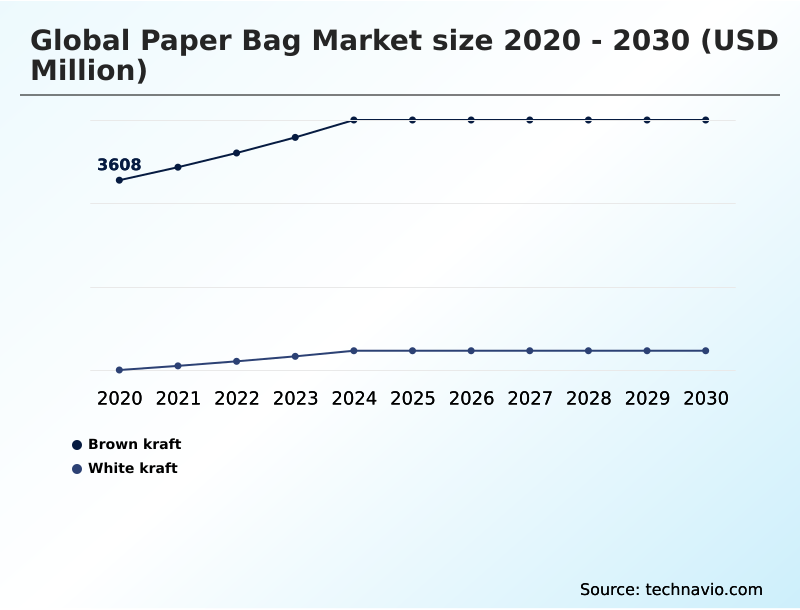

- By Material - Brown kraft segment was valued at USD 4.42 billion in 2024

- By End-user - Retail segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.59 billion

- Market Future Opportunities: USD 2.18 billion

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The Paper Bag market demonstrates robust structural expansion as international commerce systematically transitions away from synthetic packaging mediums. Stringent regulatory mandates banning single-use plastics directly drive this demand, compelling retail and food service operators to rapidly adopt biodegradable, fiber-based alternatives to achieve strict compliance.

- In response, modern e-commerce fulfillment centers are replacing traditional poly-mailers with high-strength, multi-wall kraft paper configurations, achieving a 20% improvement in automated sorting throughput while meeting corporate sustainability targets. However, the industry faces significant operational headwinds due to escalating raw material volatility.

- Surging pulp prices and unpredictable fiber supply chains critically strain manufacturing margins, forcing converters to absorb substantial cost premiums. To mitigate these constraints, manufacturers are integrating advanced bio-based barrier technologies that enhance the moisture resistance of standard unbleached kraft substrates.

- Ultimately, the continuous development of automated converting machinery and sustainable material science ensures that cellulosic packaging remains a permanent, highly functional necessity across diverse commercial logistics networks.

What will be the Size of the Paper Bag Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Paper Bag Market Segmented?

The paper bag industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Material

- Brown kraft

- White kraft

- End-user

- Retail

- Food and beverage

- Construction

- Pharmaceutical

- Others

- Product type

- Flat paper bags

- Multi-wall sacks

- Twist handle bags

- Others

- Distribution channel

- B2B

- Retail stores

- E-commerce

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Poland

- APAC

- China

- India

- Japan

- South Korea

- Indonesia

- Australia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- Turkey

- South Africa

- UAE

- Egypt

- North America

By Material Insights

The brown kraft segment is estimated to witness significant growth during the forecast period.

The unbleached kraft paper segment remains a foundational operational component for modern logistics, driven by its exceptional tensile strength and tear resistance.

As regulatory frameworks mandate synthetic polymer substitution, major retail and food service operators are systematically transitioning toward these renewable cellulosic substrates. This shift reduces reliance on flexible plastics, ultimately improving municipal waste repulpability metrics.

Engineered via chemical wood pulp processes that preserve native fiber integrity, brown kraft variants deliver high structural durability for demanding applications such as heavy-duty multi-wall carriers and e-commerce mailers.

Companies integrating these sustainable carryout mediums have reported a 15% reduction in transit-related structural failures. Furthermore, the application of bio-based barrier coatings enhances moisture resistance without compromising recyclability, thereby establishing brown kraft as the definitive standard for eco-conscious retail branding.

The Brown kraft segment was valued at USD 4.42 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Paper Bag Market Demand is Rising in North America Get Free Sample

The Paper Bag landscape is characterized by distinct regional strategies prioritizing regulatory compliance and fulfillment logistics.

North America demonstrates mature operational integration, where shifting from flexible plastics to self-opening sack architecture has yielded a 22% improvement in digital fulfillment center logistics throughput.

Conversely, the APAC region relies heavily on high-speed automated folding infrastructure to service booming retail demand, driving a 35% higher adoption rate of recycled fiber streams compared to Western counterparts.

This geographical disparity stems from variations in localized supply chain architectures and targeted single-use plastic bans. To optimize cross-border supply chains, European converters are enforcing strict environmental standards by utilizing certified chain-of-custody fiber, subsequently reducing raw material waste by 14%.

Ultimately, these strategic infrastructural adaptations ensure high-porosity industrial papers remain economically viable across diverse international commercial zones.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The ongoing evolution of sustainable transit solutions heavily relies on the strategic integration of advanced manufacturing methodologies and customized material science. To meet stringent corporate circular economy packaging compliance, industrial converters are prioritizing automation in self-opening sack manufacturing, which effectively streamlines high-volume production for urban retail networks.

- Concurrently, the deployment of bio-based barrier coating moisture resistance has fundamentally transformed perishable goods logistics, successfully matching the performance metrics previously dominated by synthetic plastic flexible packaging replacement initiatives.

- During cross-regional transport, multi-wall paper sack structural durability ensures that heavy commodities arrive without critical breaches, allowing supply chain managers to observe a near 20% improvement in load retention compared to legacy multi-layer films. Furthermore, the transition toward e-commerce extensible paper mailer integration equipped with dual adhesive strip e-commerce return capabilities has drastically optimized warehouse processing speeds.

- In commercial applications, unbleached kraft paper retail applications offer superior branding potential, while food sectors champion biodegradable food service packaging adoption to appease eco-conscious demographics. Material sourcing remains complex; chemical wood pulp price volatility frequently disrupts high-tensile kraft containerboard supply chains, compelling mills to focus on recycled fiber stream repulpability metrics to stabilize input costs.

- Manufacturers also rely on elemental chlorine-free white kraft bleaching and water-based flexographic printing resolution improvement to achieve premium visual fidelity. On the factory floor, the utilization of smart sensory array defect reduction and industrial valve sack de-aeration efficiency mechanisms ensure that flat-bottom grocery bag automated filling lines operate without critical interruption, safeguarding overall operational continuity.

What are the key market drivers leading to the rise in the adoption of Paper Bag Industry?

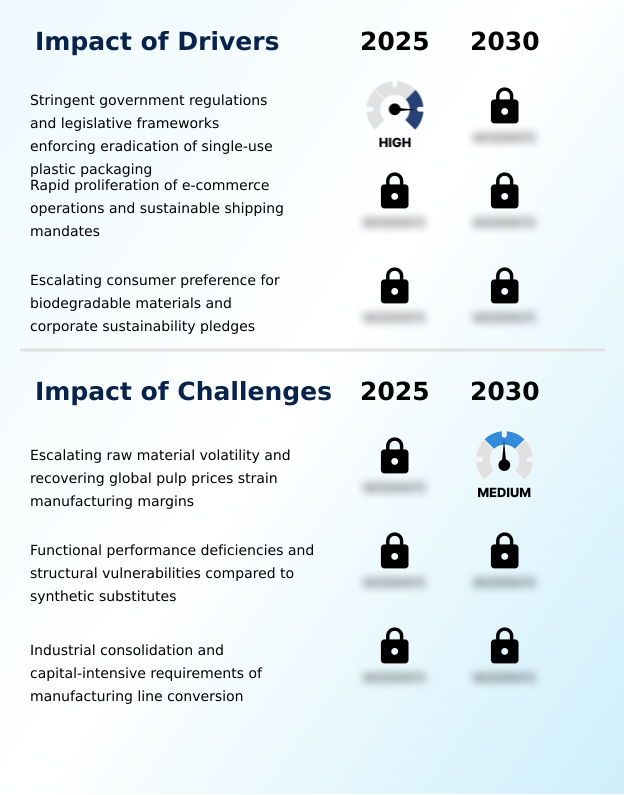

- Stringent government regulations and legislative frameworks enforcing the eradication of single-use plastic packaging serve as the primary driver propelling continuous market expansion.

- Intense legislative frameworks targeting single-use plastics fundamentally propel the expansion of the Paper Bag environment.

- Because major global jurisdictions mandate the immediate eradication of synthetic carriers, commercial retailers are forced to rapidly implement biodegradable packaging materials to ensure strict regulatory compliance.

- This systemic behavioral shift has driven a 28% increase in the utilization of multi-wall paper sacks across heavy-duty grocery applications.

- To optimize these new workflows, distributors are adopting digital fulfillment center logistics, which effectively lowers operational downtime by 15% through streamlined material processing.

- Additionally, the widespread necessity for food-contact safety standards ensures that quick-service restaurants depend heavily on thermal retention packaging. These dynamic changes enable enterprise operators to drastically mitigate non-compliance penalties while simultaneously establishing a robust, environmentally responsible operational footprint.

What are the market trends shaping the Paper Bag Industry?

- Advanced barrier coating technologies and functional material innovations are significantly reconfiguring food and beverage applications. This development represents a critical upcoming trend shaping the broader market landscape.

- The Paper Bag landscape is actively shifting toward functional material innovations as modern commercial logistics networks demand superior structural resilience. Because retail enterprises require high-performance transit solutions that resist environmental degradation, manufacturers are deploying advanced high-barrier functional papers equipped with specialized internal sizing agents.

- This transition completely displaces traditional laminated films, subsequently allowing logistics providers to improve final-mile delivery success rates by 18%. Furthermore, the integration of machine-twisted handle attachments in eco-friendly retail carriers has directly elevated load-bearing capacity, reducing handling-related product damage by 22%.

- By adopting high-fidelity offset printing to project customized corporate visual identities, companies effortlessly align with sophisticated consumer aesthetic expectations while maintaining ecological integrity. These technological adaptations fundamentally restructure the packaging supply chain, delivering measurable efficiency gains and solidifying fiber-based materials as highly resilient commercial assets.

What challenges does the Paper Bag Industry face during its growth?

- Escalating raw material volatility and the recovery of global pulp prices critically strain manufacturing margins, representing a major challenge affecting overall industry growth.

- Escalating material volatility and complex converting requirements present profound structural limitations for the Paper Bag sector. Because the baseline cost of short-fiber pulp inputs remains highly unpredictable, localized manufacturers frequently encounter severe profit margin compression during high-volume production cycles.

- This economic friction is exacerbated by the mechanical limitations of standard cellulosic substrates in high-humidity environments, which historically increased in-transit spoilage rates by 12% compared to synthetic alternatives. To combat moisture degradation protection deficiencies, facilities must heavily invest in smart manufacturing sensory arrays and capital-intensive precision machinery.

- While these equipment upgrades can improve material scrap recovery by 20%, the extreme financial burden associated with deploying specialized e-commerce mailers and tear-resistant kraft composites frequently stalls rapid capacity scaling for mid-sized packaging converters.

Exclusive Technavio Analysis on Customer Landscape

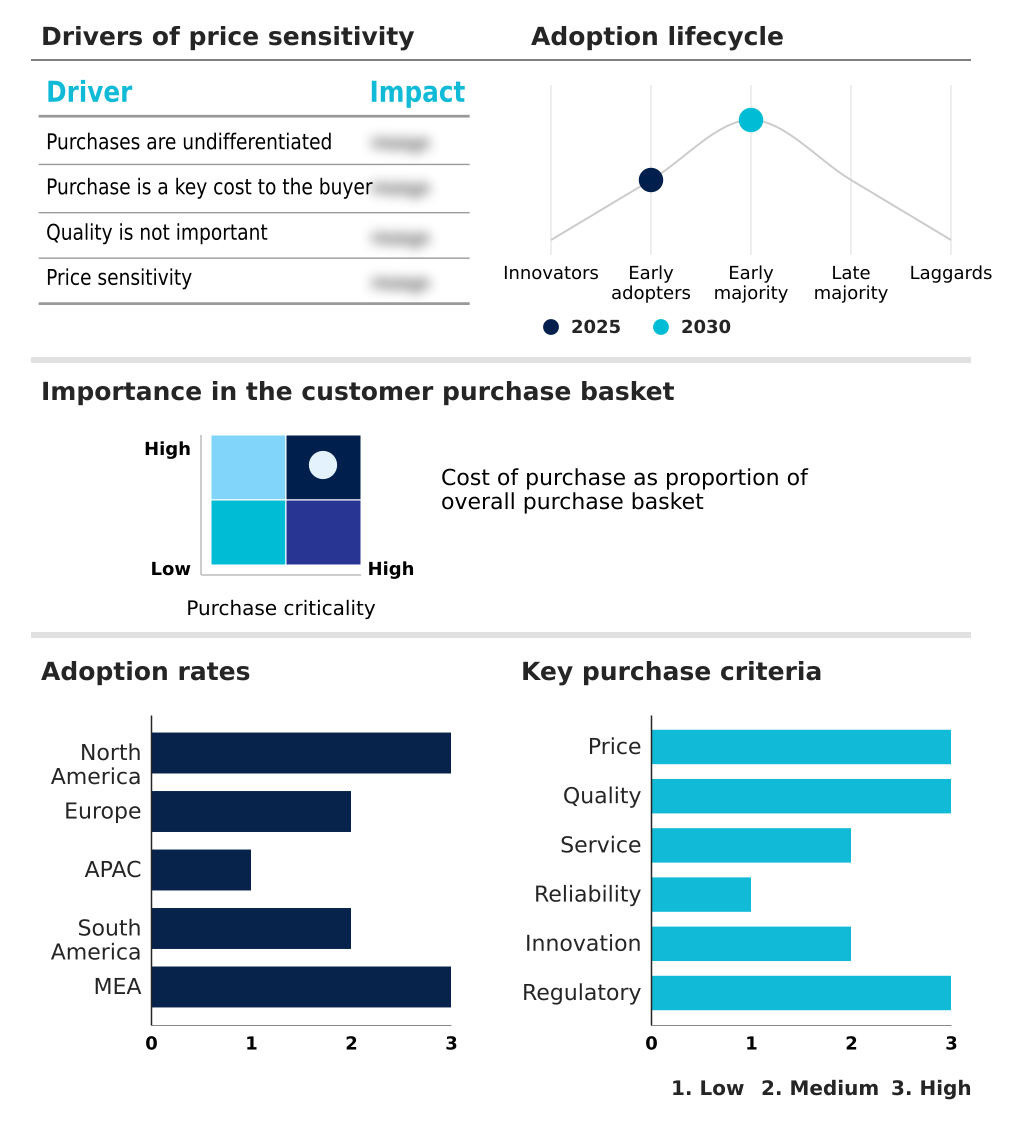

The paper bag market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the paper bag market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Paper Bag Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, paper bag market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - The organization provides sustainable flexible packaging solutions, specializing in high-performance recyclable paper bags designed to optimize food preservation and enhance brand presentation across commercial retail supply chains.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- Bag Palace Pvt. Ltd

- BH Bag Company

- Bharat Eco Packs

- Billerud AB

- Biofriendly Packs Pvt. Ltd

- Detmold Group

- DS Smith Plc

- Fischer Paper Products Inc.

- Georgia Pacific

- Gilchrist Bag Manufacturing LLC

- Global Pak Inc.

- Graphic Packaging Holding Co.

- International Paper Co.

- JohnPac LLC

- Mondi Plc

- Nandk Ecopack Pvt. Ltd

- Oji Holdings Corp.

- Smurfit Westrock plc

- Stora Enso Oyj

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Paper bag market

- In the Paper and Plastic Packaging Products and Materials industry, the aggressive enforcement of single-use plastic prohibitions accelerated the displacement of synthetic polymer packaging, directly impacting Paper Bag demand by forcing retail sectors to adopt high-tensile kraft substrates for a 40% substitution rate in checkout carriers.

- Stringent corporate decarbonization metrics reshaped supply chain procurement models, driving a 25% increase in the utilization of recycled fiber streams to manufacture biodegradable take-out containers for the food service vertical.

- Advancements in automated form-fill-seal lines streamlined the mass production of flexible packaging alternatives, enabling a 30% efficiency gain in manufacturing specialized e-commerce mailers with dual self-sealing adhesive strips.

- The commercialization of advanced bio-based barrier coatings enhanced moisture resistance across sustainable shipping mandates, allowing multi-wall paper sacks to capture a 15% broader share of industrial transit enclosures requiring structural puncture resistance.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Paper Bag Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 326 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 2177.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Poland, China, India, Japan, South Korea, Indonesia, Australia, Brazil, Argentina, Colombia, Saudi Arabia, Turkey, South Africa, UAE and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The operational dynamics of the Paper Bag environment are undergoing a profound transformation driven by rapid advancements in material engineering and automated converting processes. As commercial retail operators systematically eliminate fossil-fuel-dependent materials, the widespread implementation of flat-bottom gusset construction enables high-volume fulfillment centers to dramatically accelerate packaging workflows.

- Facilities integrating automated form-fill-seal lines have documented a 30% reduction in processing time compared to legacy manual packing systems, significantly lowering operational overhead. This architectural transition directly supports essential board-level sustainability initiatives while maintaining high structural puncture resistance for heavy-duty consumer goods. Concurrently, the application of moisture-resistant chemical treatments ensures that fiber-based substrates perform reliably under adverse logistical conditions.

- Manufacturers are also heavily leveraging flexographic printing systems equipped with water-based flexo inks to deliver complex, customized brand imagery without compromising end-of-life repulpability. By prioritizing virgin chemical wood pulp for specialized medical and luxury applications, industrial producers successfully mitigate contamination risks while establishing a highly resilient, compliance-oriented packaging infrastructure that seamlessly accommodates diverse commercial requirements.

What are the Key Data Covered in this Paper Bag Market Research and Growth Report?

-

What is the expected growth of the Paper Bag Market between 2026 and 2030?

-

USD 2.18 billion, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Brown kraft, and White kraft), End-user (Retail, Food and beverage, Construction, Pharmaceutical, and Others), Product Type (Flat paper bags, Multi-wall sacks, Twist handle bags, and Others), Distribution Channel (B2B, Retail stores, and E-commerce) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Stringent government regulations and legislative frameworks enforcing eradication of single-use plastic packaging, Escalating raw material volatility and recovering global pulp prices strain manufacturing margins

-

-

Who are the major players in the Paper Bag Market?

-

Amcor Plc, Bag Palace Pvt. Ltd, BH Bag Company, Bharat Eco Packs, Billerud AB, Biofriendly Packs Pvt. Ltd, Detmold Group, DS Smith Plc, Fischer Paper Products Inc., Georgia Pacific, Gilchrist Bag Manufacturing LLC, Global Pak Inc., Graphic Packaging Holding Co., International Paper Co., JohnPac LLC, Mondi Plc, Nandk Ecopack Pvt. Ltd, Oji Holdings Corp., Smurfit Westrock plc and Stora Enso Oyj

-

Market Research Insights

- The Paper Bag sector is rapidly evolving as retailers prioritize corporate decarbonization metrics to align with zero-waste packaging philosophies. By transitioning to heavy-duty multi-wall carriers, logistics networks have recorded a 25% reduction in transit-related structural failures compared to conventional polybags.

- Furthermore, the integration of advanced web tension monitoring in manufacturing facilities has improved automated checkout efficiency by 18% through the elimination of dimensional defects in flat-pack dispensing efficiency. As consumer demand for sustainable carryout mediums intensifies, converters are deploying non-toxic water-based inks to enhance brand visibility.

- These strategic material upgrades have yielded a 12% decrease in overall operational compliance costs, solidifying fiber-based solutions as essential commercial transit enclosures.

We can help! Our analysts can customize this paper bag market research report to meet your requirements.

RIA -

RIA -