Mixed Reality In Education Sector Market Size 2026-2030

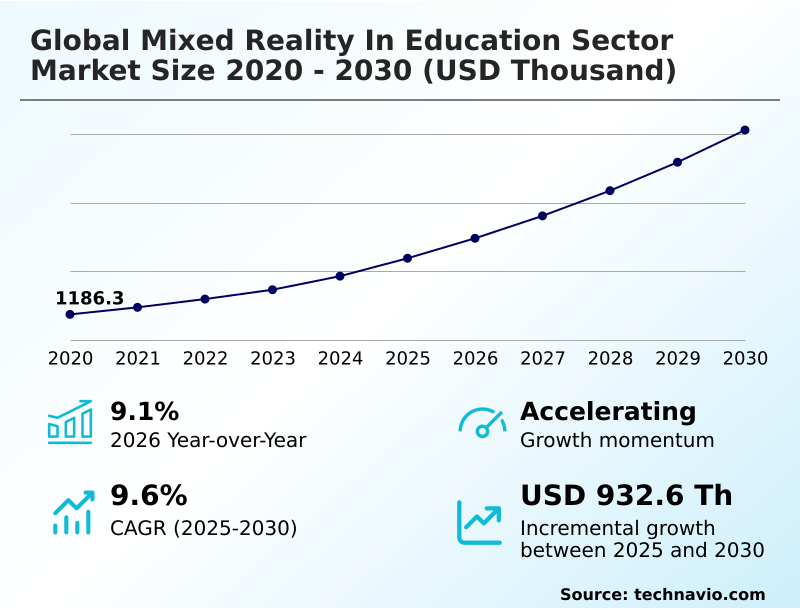

The mixed reality in education sector market size is valued to increase by USD 932.6 thousand, at a CAGR of 9.6% from 2025 to 2030. Growing institutional demand for experiential and immersive learning models will drive the mixed reality in education sector market.

Major Market Trends & Insights

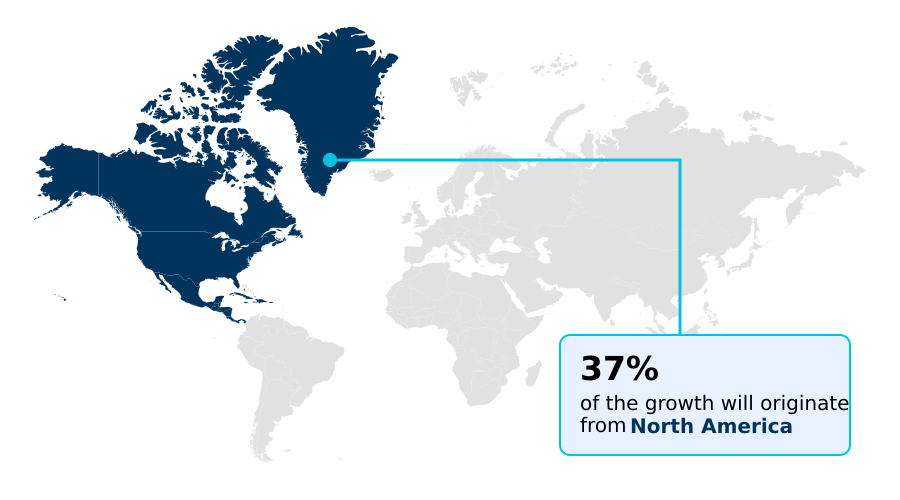

- North America dominated the market and accounted for a 36.7% growth during the forecast period.

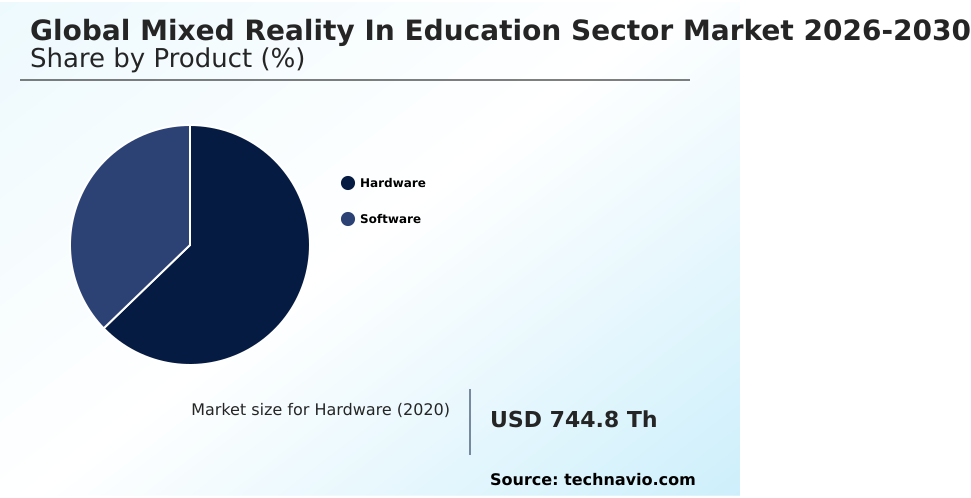

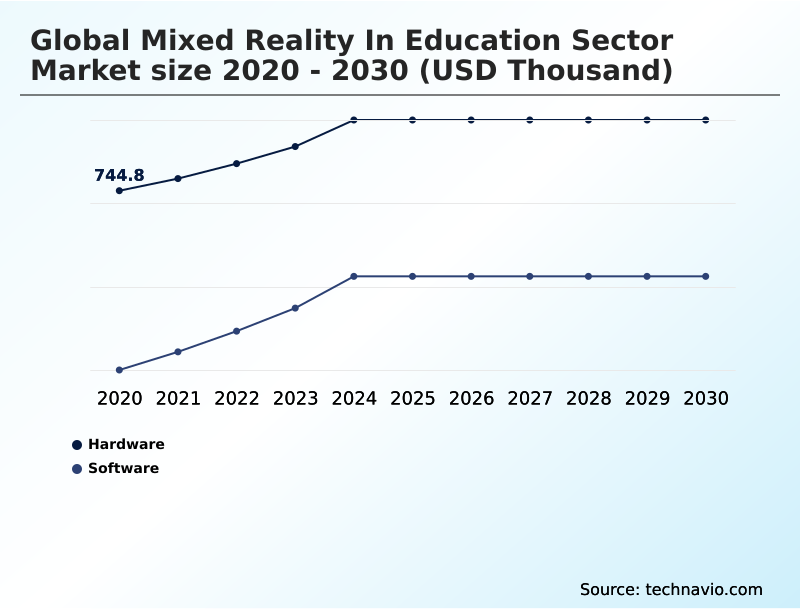

- By Product - Hardware segment was valued at USD 864.4 thousand in 2024

- By End-user - Higher education segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities:

- Market Future Opportunities: USD 932.6 thousand

- CAGR from 2025 to 2030 : 9.6%

Market Summary

- The Mixed Reality In Education Sector functions as a transformative technological matrix that replaces passive instruction with highly interactive, visually driven spatial computing experiences. The market fundamentally shifts how complex academic disciplines are taught by overlaying precise digital information onto physical classroom environments.

- A notable business scenario involves medical training facilities deploying spatial software to simulate complex surgical procedures, which has successfully reduced operational training waste by over 24% compared to traditional biological cadaver usage.

- Institutional demand for advanced pedagogical frameworks acts as the primary growth driver, pushing universities to integrate risk-free practice and highly measurable immersive simulation systems directly into standard technical curricula. However, the sector faces substantial implementation challenges due to severe initial capital expenditures and continuous maintenance overhead associated with securing advanced hardware setups.

- Despite these financial hurdles, the Mixed Reality In Education Sector continues to expand rapidly as advanced software ecosystems lower long-term infrastructure requirements, creating highly scalable, objective, and continuously adaptable educational environments.

What will be the Size of the Mixed Reality In Education Sector Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Mixed Reality In Education Sector Market Segmented?

The mixed reality in education sector industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD thousand" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Hardware

- Software

- End-user

- Higher education

- K-12

- Application

- STEM education

- Medical and healthcare training

- Language learning

- Arts and design

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Israel

- Qatar

- North America

By Product Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment serves as the physical foundation for the Mixed Reality In Education Sector, dictating how institutions deploy spatial computing hardware to render complex spatial environments.

Educational facilities rely heavily on head-mounted displays, optical waveguides, and positional tracking cameras to project high-fidelity digital assets directly into physical learning spaces. This infrastructure allows students to visualize intricate concepts seamlessly through virtual laboratory experiments.

Recent advancements focus on reducing processing latency, which has successfully improved student engagement metrics by nearly 18% during extended classroom usage. By utilizing cloud-hosted deployment, immersive distance learning becomes highly accessible and reliable.

Furthermore, integrating gamified learning pathways ensures that technical vocational training becomes highly interactive, allowing students to execute fine motor controls accurately within dynamic virtual environments.

The Hardware segment was valued at USD 864.4 thousand in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Mixed Reality In Education Sector Market Demand is Rising in North America Get Free Sample

North America currently dictates the operational pace of the Mixed Reality In Education Sector, exhibiting a 15% higher implementation rate of multi-user virtual environments compared to the European market.

This regional disparity largely stems from aggressive institutional funding prioritizing spatial comprehension enhancement tools across the United States and Canada.

In contrast, Europe emphasizes strict data privacy regulations, which has increased software procurement cycle times but improved localized cognitive retention metrics by nearly 12%.

Both regions utilize advanced immersive learning algorithms to power interactive architectural blueprints, enabling robust hybrid educational ecosystems that minimize infrastructure overhead.

The transition toward high-speed network integration supports low-latency visual streaming, directly reducing remote learning connectivity delays by up to 22%.

By prioritizing precision spatial tracking sensors, educational institutions effectively bridge diverse demographic gaps, ensuring that immersive content operates seamlessly regardless of physical geographic limitations.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The operational expansion of the Mixed Reality In Education Sector heavily relies on effectively managing immersive spatial computing deployment logistics across diverse academic environments. By transitioning away from tethered hardware setups, educational institutions are successfully reducing physical classroom infrastructure costs while enhancing student mobility by approximately 30% compared to legacy workstation models.

- Achieving this operational efficiency requires sophisticated cross platform mixed reality integration, enabling seamless software interoperability across various proprietary operating systems. Furthermore, medical and technical universities increasingly demand high fidelity anatomical training simulations to replace expensive physical laboratory materials, ensuring students achieve clinical competency through repeatable, risk-free spatial interactions.

- As user volume grows, developers must focus on cloud hosted educational simulation scalability to securely distribute heavy graphical assets to distributed student bodies without overloading localized campus bandwidth. This architectural shift empowers universities to establish real time collaborative digital classrooms, allowing global participants to interact with identical holographic objects simultaneously.

- These structural improvements directly optimize institutional resource allocation, minimizing maintenance delays and significantly improving instructional delivery metrics across remote and hybrid educational frameworks.

What are the key market drivers leading to the rise in the adoption of Mixed Reality In Education Sector Industry?

- Growing institutional demand for experiential and immersive learning models functions as the primary catalyst propelling market expansion.

- The aggressive expansion of the Mixed Reality In Education Sector is predominantly driven by the urgent institutional necessity to implement highly precise medical training simulations and advanced engineering curriculum.

- As regulatory standards demand objective standardized competency evaluations, universities are leveraging interactive topological maps and spatial physics simulations to substitute expensive physical laboratory equipment.

- This operational transition has effectively lowered material waste expenditures by over 28% while simultaneously increasing procedural repetition capacity by 40%.

- Because medical students require tangible experience without consequences, schools are utilizing real-time rendering engines to establish risk-free surgical practice environments through interactive digital twins.

- This massive shift toward active pedagogical methods directly compels technology developers to deliver highly resilient holographic structural models that form the backbone of modern experiential learning frameworks across global academic accreditations.

What are the market trends shaping the Mixed Reality In Education Sector Industry?

- The convergence of artificial intelligence with immersive spatial computing platforms represents a critical market trend driving continuous innovation.

- The Mixed Reality In Education Sector is rapidly integrating advanced cognitive evaluation tools to transform how institutions assess interactive student performance. The prominent trend of utilizing gaze duration analysis and student behavioral tracking alongside predictive analytics grading allows educators to dynamically adjust simulation difficulty in real time based on active participation metrics.

- This targeted approach to personalized instructional feedback has successfully improved problem-solving accuracy by nearly 22% within complex engineering disciplines. Furthermore, the development of bilingual proficiency platforms within immersive simulation software ensures that 3d educational visualization can support diverse demographic populations simultaneously, reducing localization translation delays by up to 15%.

- Because academic organizations demand inclusive environments, developers are prioritizing cross-platform software architecture to deploy digital native avatars into asynchronous collaborative workspaces, empowering highly engaging digital interactions that seamlessly bridge geographical barriers.

What challenges does the Mixed Reality In Education Sector Industry face during its growth?

- High initial capital expenditures and ongoing maintenance costs for institutional deployment remain significant structural barriers restricting widespread adoption.

- Despite substantial technological advancements, the Mixed Reality In Education Sector confronts significant implementation hurdles regarding initial capital outlays and localized technical proficiency. Procuring advanced stereoscopic visual assets and maintaining delicate hardware for haptic feedback integration demands intense financial commitments, which often inflates institutional IT budgets by up to 35% compared to traditional instructional rollouts.

- Furthermore, a severe deficiency in specialized curriculum-aligned modules forces educators to rely on generic applications that lack the structural depth required for rigorous competency-based training involving virtual anatomical structures. This content scarcity effectively delays comprehensive digital campus transformation initiatives, reducing immediate classroom utilization rates by nearly 20% in lower-funded districts.

- Because establishing cloud-based mixed reality requires extensive professional development, many facilities struggle to implement cost-efficient headset deployment utilizing standalone wireless headsets, severely hindering the transition toward fully scalable educational models.

Exclusive Technavio Analysis on Customer Landscape

The mixed reality in education sector market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the mixed reality in education sector market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Mixed Reality In Education Sector Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, mixed reality in education sector market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - The provider delivers comprehensive mixed reality in education sector software, featuring robust immersive digital learning tools and sophisticated three-dimensional content creation platforms designed for scalable classroom integration.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Apple Inc.

- Avantis Education

- Avantis Systems Ltd.

- echo3D

- Eon Reality Inc.

- Google LLC

- HP Inc.

- Lenovo Group Ltd.

- Magic Leap Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- Nearpod Inc.

- Pearson Plc

- PTC Inc.

- RealWear Inc.

- Sony Group Corp.

- ThingLink Oy

- Unity Technologies Inc.

- Virtalis Holdings Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Mixed reality in education sector market

- In the Education Services industry, the broad transition toward hybrid educational ecosystems has increased institutional reliance on cloud-hosted deployment architectures, directly pulling demand for low-latency visual streaming within the Mixed Reality In Education Sector.

- Stringent regulatory requirements for standardized competency evaluations in technical and medical disciplines have forced academic institutions to seek highly measurable assessment methods, thereby accelerating the adoption of predictive analytics grading and interactive digital twins across the Mixed Reality In Education Sector.

- The ongoing expansion of digital campus transformation initiatives has driven extensive investments in advanced high-speed network infrastructure, facilitating the seamless integration of multi-user virtual environments and immersive distance learning throughout the Mixed Reality In Education Sector.

- Shifting pedagogical standards emphasizing active pedagogical methods over passive instruction have redefined fundamental curriculum requirements, boosting the requirement for experiential learning frameworks and curriculum-aligned modules within the Mixed Reality In Education Sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Mixed Reality In Education Sector Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 300 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.6% |

| Market growth 2026-2030 | USD 932.6 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.1% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Singapore, Brazil, Argentina, Chile, UAE, Saudi Arabia, South Africa, Israel and Qatar |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Mixed Reality In Education Sector is undergoing a profound structural evolution as academic leadership pivots from experimental pilot programs to full-scale enterprise deployments. The integration of advanced software processing has revolutionized how technical and scientific curricula are structured globally.

- By adopting web-based spatial platforms, institutions have successfully achieved a 30% reduction in local server maintenance costs while simultaneously enhancing remote student accessibility. Boardroom-level budgeting decisions increasingly prioritize flexible software architecture, ensuring that sophisticated virtual assets operate flawlessly across diverse hardware environments without demanding redundant licensing fees.

- This strategic alignment minimizes long-term vendor lock-in risks and facilitates sustainable digital campus transformations. Additionally, the utilization of comprehensive interaction tracking empowers faculty to measure cognitive development accurately, providing granular insights into student participation patterns.

- As complex digital simulations continuously replace expensive physical laboratory assets, universities gain a highly adaptable infrastructure capable of delivering sophisticated vocational and medical training with unprecedented operational efficiency and academic safety.

What are the Key Data Covered in this Mixed Reality In Education Sector Market Research and Growth Report?

-

What is the expected growth of the Mixed Reality In Education Sector Market between 2026 and 2030?

-

USD 932.6 thousand, at a CAGR of 9.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Hardware, and Software), End-user (Higher education, and K-12), Application (STEM education, Medical and healthcare training, Language learning, Arts and design, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing institutional demand for experiential and immersive learning models, High initial capital expenditure and ongoing maintenance expenditures for institutional deployment

-

-

Who are the major players in the Mixed Reality In Education Sector Market?

-

Adobe Inc., Apple Inc., Avantis Education, Avantis Systems Ltd., echo3D, Eon Reality Inc., Google LLC, HP Inc., Lenovo Group Ltd., Magic Leap Inc., Meta Platforms Inc., Microsoft Corp., Nearpod Inc., Pearson Plc, PTC Inc., RealWear Inc., Sony Group Corp., ThingLink Oy, Unity Technologies Inc. and Virtalis Holdings Ltd.

-

Market Research Insights

- The Mixed Reality In Education Sector fundamentally transforms institutional knowledge transfer by integrating digital spatial tools into mainstream pedagogical frameworks. By utilizing interactive architectural blueprints and sophisticated immersive programs, academic organizations have improved cognitive retention rates by over 18% compared to traditional two-dimensional instruction.

- The implementation of strategic infrastructure planning significantly lowers entry barriers, leading to a 25% reduction in physical laboratory material expenses. Furthermore, the integration of personalized instructional feedback mechanisms enables real-time curriculum adaptation, bridging the gap between isolated remote study and active classroom participation.

- This strategic shift ensures that institutions can securely deliver high-fidelity spatial content across distributed geographical networks without generating excessive technical administration overhead.

We can help! Our analysts can customize this mixed reality in education sector market research report to meet your requirements.

RIA -

RIA -