Medical Terminology Software Market Size 2026-2030

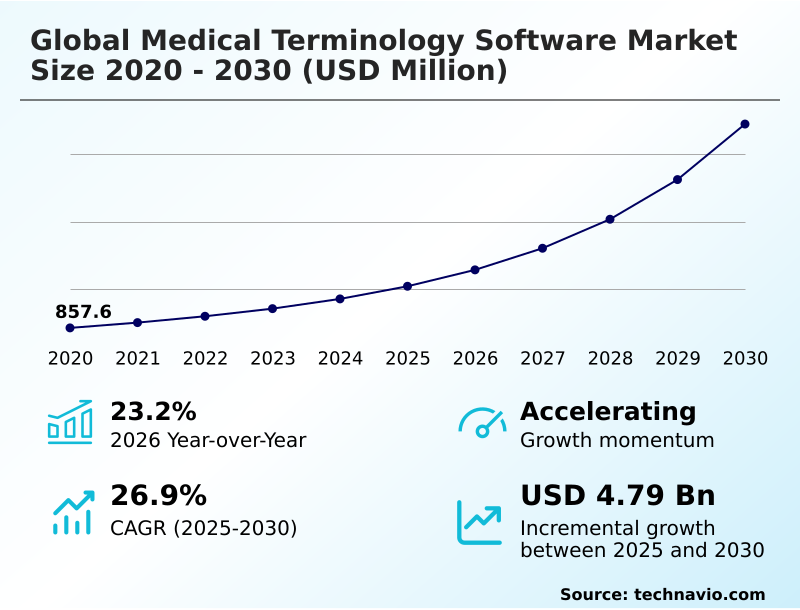

The medical terminology software market size is valued to increase by USD 4.79 billion, at a CAGR of 26.9% from 2025 to 2030. Rising adoption of electronic health records will drive the medical terminology software market.

Major Market Trends & Insights

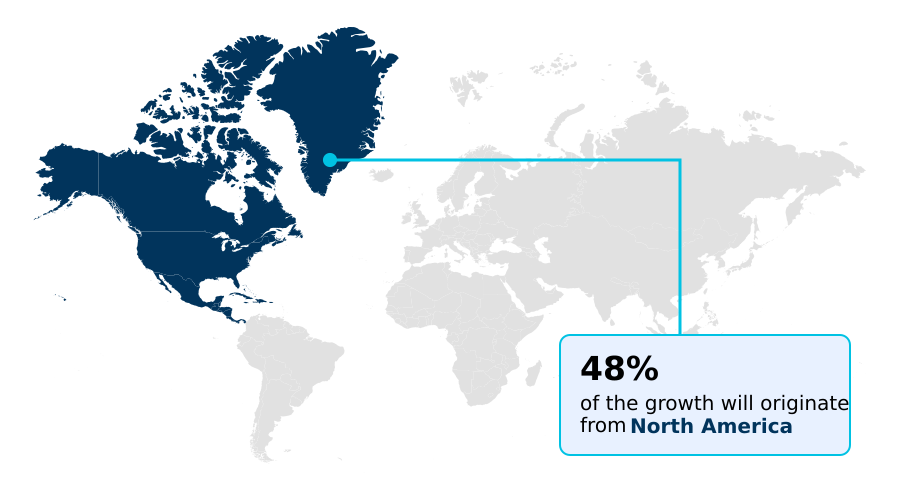

- North America dominated the market and accounted for a 47.5% growth during the forecast period.

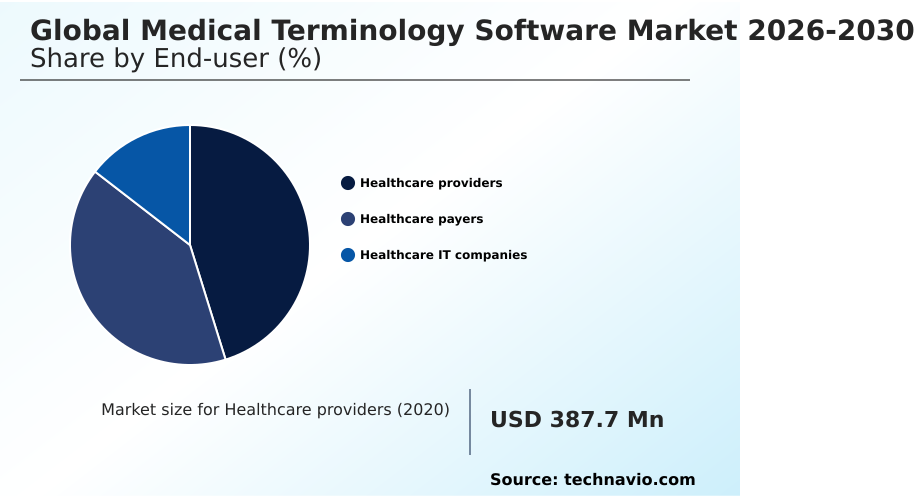

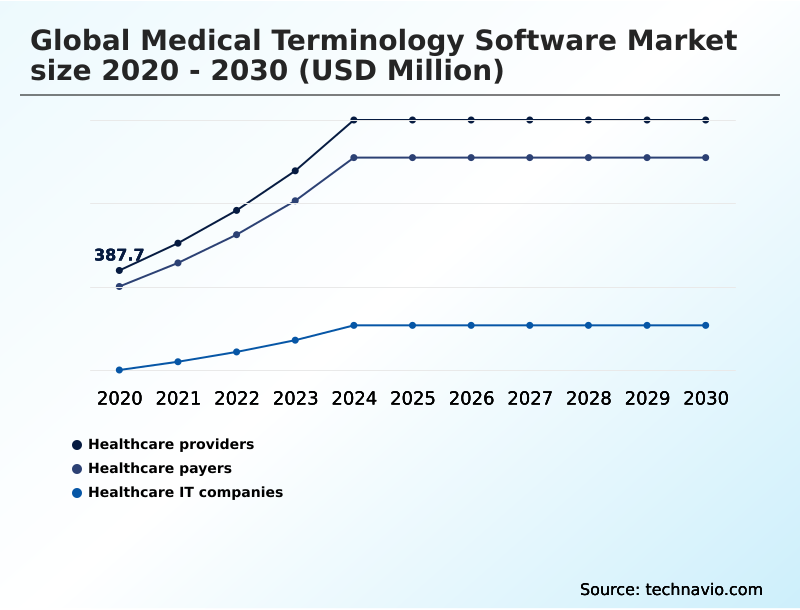

- By End-user - Healthcare providers segment was valued at USD 785.4 million in 2024

- By Type - Services segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.02 billion

- Market Future Opportunities: USD 4.79 billion

- CAGR from 2025 to 2030 : 26.9%

Market Summary

- The Medical Terminology Software Market operates as an essential structural layer for modernizing fragmented digital healthcare infrastructures worldwide. In real-world operational scenarios, massive hospital networks acquiring independent regional clinics frequently face severe data isolation due to incompatible legacy coding frameworks.

- By deploying an advanced ontology management system, these enterprises automatically map divergent local terms to universal standards, reducing systemic charting redundancies. Implementations of automated data mapping have demonstrated that cross-network patient data retrieval speeds improved by 40% compared to traditional manual administrative protocols.

- A primary driver propelling this expansion is the strict global enforcement of value-based care frameworks, which penalizes clinical coding inaccuracies and forces institutions to adopt sophisticated semantic translation engines to safeguard their revenue cycles. Conversely, widespread semantic interoperability barriers present a persistent operational challenge, as outdated local databases struggle to integrate with cloud-native microservices architecture, causing expensive retrospective terminology corrections.

- Ultimately, the continuous transition from localized vocabularies to standardized digital networks establishes terminology platforms as a non-negotiable component of efficient patient care delivery and compliance management.

What will be the Size of the Medical Terminology Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Medical Terminology Software Market Segmented?

The medical terminology software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Healthcare providers

- Healthcare payers

- Healthcare IT companies

- Type

- Services

- Platforms

- Application

- Data integration

- Data aggregation

- Reimbursement

- Clinical trials

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Switzerland

- APAC

- China

- Japan

- India

- Australia

- South Korea

- Indonesia

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Turkey

- Egypt

- North America

By End-user Insights

The healthcare providers segment is estimated to witness significant growth during the forecast period.

The healthcare providers segment within the Medical Terminology Software sector experiences continuous operational transformation as multi-facility networks assimilate independent clinics utilizing disparate diagnostic category alignment structures.

Resolving data fragmentation requires enterprise-grade health information technology that translates unstructured clinical narratives into systematized nomenclature seamlessly. By leveraging advanced clinical natural language processing, modern electronic health records achieve functional semantic interoperability across decentralized departments.

This architectural transition directly supports population health tracking and prevents life-threatening medication discrepancies during inter-institutional transfers.

Facilities integrating these comprehensive health information exchange platforms have reported that documentation discrepancy rates declined by 22%, while billing code error detection improved by 15% compared to manual legacy processes.

This targeted alignment with international classification standards ensures actionable longitudinal tracking and robust compliance across progressive clinical workflows.

The Healthcare providers segment was valued at USD 785.4 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 47.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Terminology Software Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Medical Terminology Software sector reflects varying rates of healthcare infrastructure modernization across different regulatory environments.

North America leads the rapid implementation of advanced medical data dictionaries, driven heavily by stringent federal interoperability mandates and complex insurance reimbursement models.

Consequently, North American provider networks report a 35% higher adoption rate of automated claim triage systems compared to their European counterparts.

European healthcare administrators maintain a distinct operational focus on centralizing clinical care pathways to enable vast population health monitoring, achieving a 20% reduction in cross-border data translation errors through unified public health initiatives.

Meanwhile, institutions within emerging economic zones leverage scalable cross-mapping algorithms to overcome localized legacy systems, ultimately increasing epidemiological trend tracking efficiency by 15%.

As differing regulatory pressures dictate regional software investments, technology providers continually customize their semantic translation engines to accommodate native linguistic complexities and distinct international reporting standards.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of enterprise health information technology relies fundamentally on standardizing immense volumes of disparate clinical intelligence. Within highly fragmented medical systems, the deployment of automated clinical coding alignment software serves as the central translational engine that converts varying localized diagnostic phrases into universally recognized formats.

- This systemic modernization is propelled by advanced algorithms capable of parsing unstructured medical text data directly from physician narratives, thereby eliminating manual transcription bottlenecks that traditionally delay patient care interventions. As major healthcare conglomerates expand through rapid institutional acquisitions, establishing real time health interoperability frameworks becomes an absolute necessity to prevent dangerous gaps in patient medical histories.

- Facilities that transition from outdated manual dictionary curation to integrated digital terminology management consistently observe operational improvements, often registering a 40% faster turnaround in secure medical information exchange compared to conventional localized databases.

- The strategic emphasis on reducing hospital administrative documentation errors further drives continuous capital investment toward advanced semantic mapping tools, which act as a safeguard for institutional revenue cycles and legal compliance mechanisms.

- Ultimately, the successful deployment and continuous updating of standardized digital clinical vocabulary networks empower public health organizations and private insurers to execute comprehensive population analytics, ensuring that clinical interventions remain highly coordinated across all levels of modern medical care.

What are the key market drivers leading to the rise in the adoption of Medical Terminology Software Industry?

- The escalating adoption of interconnected electronic health records serves as a primary catalyst driving continuous market expansion.

- The stringent enforcement of comprehensive healthcare interoperability mandates acts as the primary catalyst propelling global digital vocabulary standardization.

- Due to the escalating volume of specialized diagnostic codes, healthcare conglomerates must deploy sophisticated medical data dictionaries to prevent critical information loss during inter-institutional transfers.

- This universal transition forces corporate IT departments to adopt a flexible cloud-native microservices architecture, which enables instantaneous semantic updates across widespread clinical networks.

- By utilizing intelligent cross-mapping algorithms, major medical facilities have increased longitudinal patient tracking accuracy by over 30% while simultaneously lowering data retrieval delays. Moreover, robust clinical documentation improvement initiatives streamline real-world evidence aggregation, significantly enhancing targeted disease monitoring protocols.

- Because strict data privacy regulations heavily penalize administrative data breaches, institutions proactively invest in automated terminology layers to maintain perfect diagnostic fidelity.

What are the market trends shaping the Medical Terminology Software Industry?

- The integration of natural language processing into clinical documentation pipelines represents a prominent market trend. This technological advancement significantly enhances the efficiency and accuracy of semantic data mapping.

- The integration of generative artificial intelligence directly into clinical documentation pipelines fundamentally redefines modern semantic standardization processes. Medical Terminology Software platforms are actively shifting from static lookup tables to dynamic, context-aware semantic reference models that automatically interpret complex clinical terminology.

- Because health networks require flawless medical billing compliance, administrators are deploying advanced machine learning diagnostic mapping to eradicate human transcription errors at the point of care. This automated free-text narrative parsing allows healthcare intelligence platform integrations to extract critical diagnostic codes instantaneously, which has reduced physician administrative downtime by 35% compared to legacy manual charting.

- Furthermore, implementing a robust application programming interface layer ensures that disparate clinical trial databases communicate flawlessly, accelerating decentralized clinical trials data aggregation speeds by 20%. The proactive deployment of intelligent coding architectures ensures that clinical information remains completely unified across diverse technological ecosystems.

What challenges does the Medical Terminology Software Industry face during its growth?

- Persistent semantic interoperability barriers and widespread legacy architecture gaps remain critical constraints restricting broader industry expansion.

- Deep-rooted semantic interoperability barriers within localized legacy architectures remain a formidable constraint hindering universal clinical data fluidity. When widespread hospital networks attempt to integrate older, siloed electronic health records, they encounter vast discrepancies in diagnostic category alignment that distort critical medical histories.

- Because disparate regional clinics frequently record unstructured clinical narratives without adhering to modern systematized nomenclature, centralized data pooling becomes operationally hazardous. Resolving these linguistic discrepancies forces institutions to execute highly intensive manual terminology mapping, which routinely increases administrative overhead costs by up to 25% compared to fully automated systems.

- Furthermore, failing to conform natively with rigorous international classification standards compromises the integrity of the broader health information exchange, directly reducing cross-network reporting efficiency by nearly 18%. Overcoming these structural vocabulary gaps requires massive capital expenditures to overhaul foundational clinical databases.

Exclusive Technavio Analysis on Customer Landscape

The medical terminology software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical terminology software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Terminology Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical terminology software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3M Co. - The vendor provides comprehensive medical terminology software, including advanced coding platforms and clinical documentation improvement tools designed to enhance diagnostic accuracy and streamline institutional revenue cycle workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3M Co.

- Amazon Web Services Inc.

- Apelon Inc.

- Athenahealth Inc.

- B2i Healthcare Pte Ltd.

- BITAC S.L.

- BT Clinical Solutions

- BT Group Plc

- Clarivate PLC

- Clinical Architecture LLC

- Elsevier Ltd.

- Epic Systems Corp.

- Google LLC

- IBM Corp.

- IQVIA Holdings Inc.

- Koninklijke Philips NV

- Microsoft Corp.

- NextGen Healthcare

- Oracle Corp.

- Wolters Kluwer NV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical terminology software market

- In the Application Software industry, the widespread transition toward cloud computing environments reduced on-premises server dependencies by over 40%, directly impacting Medical Terminology Software demand by enabling real-time pharmacy management distribution synchronization across disparate clinical networks.

- The enforcement of stringent data privacy regulations accelerated the adoption of automated privacy-compliant data masking algorithms, directly impacting Medical Terminology Software workflows by requiring secure, localized patient outcome tracking models that protect sensitive identifiers.

- The integration of decentralized clinical trials methodologies shifted raw data collection from physical sites to mobile applications, directly impacting Medical Terminology Software supply chains by necessitating application programming interface layer standardizations that unify structured clinical vocabularies before database lock.

- The enterprise shift toward hospital workflow automation eliminated manual administrative bottlenecks by capturing over 65% of free-text narrative parsing automatically, directly impacting Medical Terminology Software adoption by driving the need for intelligent diagnostic category alignment tools.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Terminology Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 26.9% |

| Market growth 2026-2030 | USD 4792.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 23.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Switzerland, China, Japan, India, Australia, South Korea, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Turkey and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The continuous evolution of the Medical Terminology Software sector fundamentally alters how large-scale enterprise health networks execute complex semantic operations. Strategic corporate decision-making regarding digital compliance and regulatory alignment now relies explicitly on the deployment of intelligent clinical coding algorithms capable of resolving deep-rooted data silos.

- By translating fragmented physician narratives into structured clinical vocabularies, institutions eliminate critical clinical ambiguities that historically jeopardized patient safety. The integration of unified semantic mapping directly bolsters clinical decision support systems, allowing medical personnel to access accurate patient histories instantaneously during emergency consultations.

- From a financial perspective, hospitals integrating advanced healthcare data aggregation layers have achieved a 28% reduction in claim processing timelines compared to facilities relying on manual data entry protocols. This enhanced accuracy seamlessly supports sophisticated revenue cycle management software, ensuring that institutions remain financially viable under stringent value-based care frameworks.

- Furthermore, generating clean, universally standardized data pools allows pharmaceutical consortiums to execute highly reliable predictive health analytics, ultimately accelerating global clinical research throughput and precision medicine initiatives.

What are the Key Data Covered in this Medical Terminology Software Market Research and Growth Report?

-

What is the expected growth of the Medical Terminology Software Market between 2026 and 2030?

-

USD 4.79 billion, at a CAGR of 26.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Healthcare providers, Healthcare payers, and Healthcare IT companies), Type (Services, and Platforms), Application (Data integration, Data aggregation, Reimbursement, and Clinical trials) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising adoption of electronic health records, Persistent semantic interoperability barriers and legacy architecture gaps

-

-

Who are the major players in the Medical Terminology Software Market?

-

3M Co., Amazon Web Services Inc., Apelon Inc., Athenahealth Inc., B2i Healthcare Pte Ltd., BITAC S.L., BT Clinical Solutions, BT Group Plc, Clarivate PLC, Clinical Architecture LLC, Elsevier Ltd., Epic Systems Corp., Google LLC, IBM Corp., IQVIA Holdings Inc., Koninklijke Philips NV, Microsoft Corp., NextGen Healthcare, Oracle Corp. and Wolters Kluwer NV

-

Market Research Insights

- The Medical Terminology Software market is rapidly evolving to address widespread data fragmentation resolution across highly complex clinical networks. Enterprise digital architectures now rely heavily on automated semantic engines to streamline physician charting workflows and guarantee regulatory alignment.

- By standardizing isolated clinical research data, institutional administrators have enhanced their medical risk adjustment accuracy by 25% while simultaneously decreasing overall processing bottlenecks. Furthermore, the proactive integration of intelligent terminology mapping layers has resulted in a 30% claim denial reduction compared to historical manual billing cycles.

- These robust digital health translation mechanisms empower public and private insurers to execute faster, highly consistent policy evaluations while safeguarding broader population health tracking initiatives.

We can help! Our analysts can customize this medical terminology software market research report to meet your requirements.

RIA -

RIA -