Medical Device Manufacturing Outsourcing Market Size 2026-2030

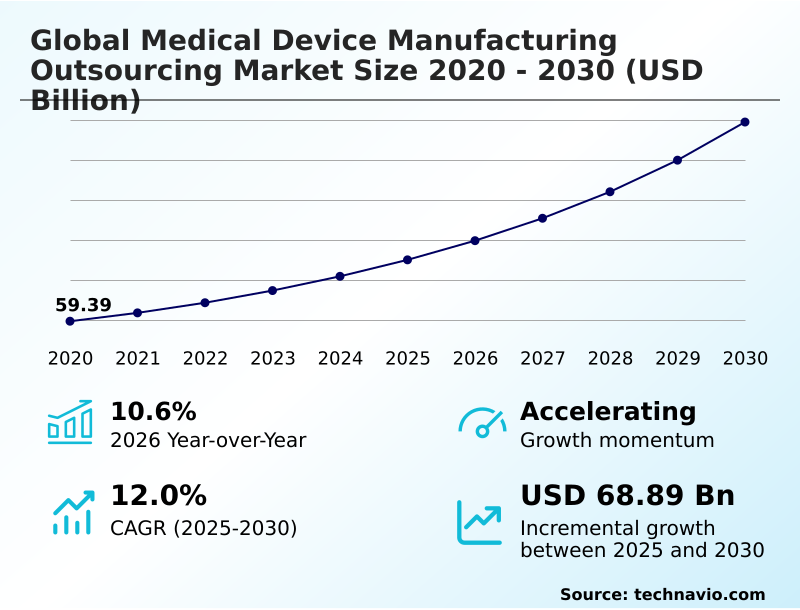

The medical device manufacturing outsourcing market size is valued to increase by USD 68.89 billion, at a CAGR of 12% from 2025 to 2030. Technological advancement and proliferation of connected digital healthcare infrastructure will drive the medical device manufacturing outsourcing market.

Major Market Trends & Insights

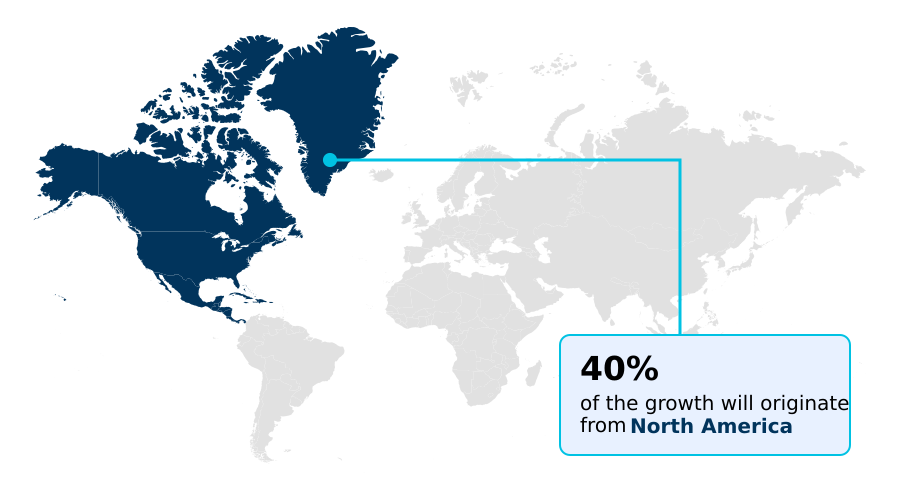

- North America dominated the market and accounted for a 39.7% growth during the forecast period.

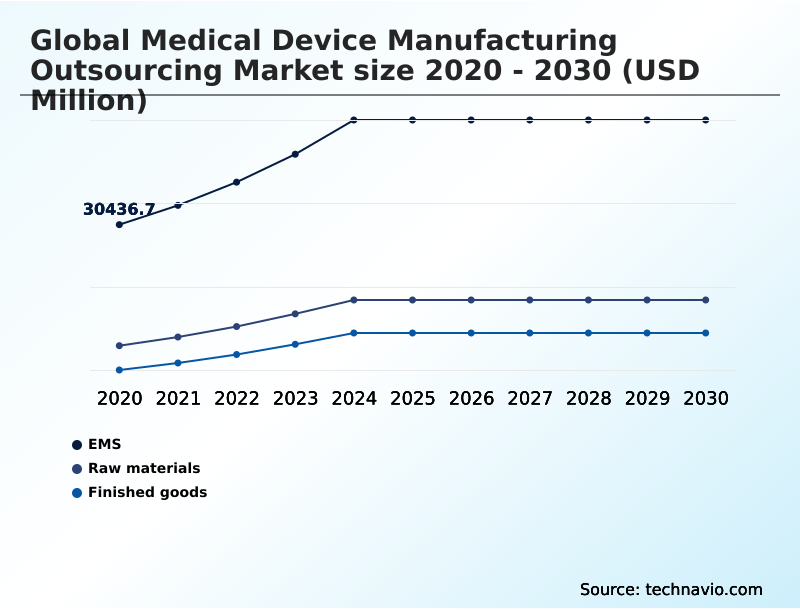

- By Product - EMS segment was valued at USD 42.98 billion in 2024

- By Class Type - Class II segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 99.59 billion

- Market Future Opportunities: USD 68.89 billion

- CAGR from 2025 to 2030 : 12%

Market Summary

- The Medical Device Manufacturing Outsourcing framework is rapidly transforming from basic component sourcing into comprehensive, highly technical engineering partnerships. Original equipment manufacturers are aggressively transitioning complex electro mechanical assembly workloads to specialized contract manufacturers to avoid steep capital expenditures.

- For example, by utilizing third-party cleanrooms for advanced drug delivery device assembly, healthcare brands optimize supply chain logistics and successfully compress commercialization timelines without building internal manufacturing infrastructure. This asset-light model allows medical innovators to cut internal capital expenditures by an estimated 20%.

- The proliferation of connected digital healthcare infrastructure serves as a major driver, as brands require external expertise in printed circuit board fabrication to maintain product viability. Conversely, vulnerabilities in sub-tier component traceability restrict market integration, as minor raw material anomalies can trigger widespread clinical failures. By shifting production to compliant external facilities, companies systematically minimize their legal exposures.

What will be the Size of the Medical Device Manufacturing Outsourcing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Medical Device Manufacturing Outsourcing Market Segmented?

The medical device manufacturing outsourcing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- EMS

- Raw materials

- Finished goods

- Class type

- Class II

- Class III

- Class I

- Service type

- Manufacturing services

- Quality assurance and testing

- Device development and design services

- Regulatory and certification support

- End-user

- Medical device companies

- Pharmaceutical and biotech firms

- Hospitals and clinics

- Research institutions

- Geography

- North America

- US

- Canada

- Mexico

- Asia

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- Rest of World (ROW)

- North America

By Product Insights

The ems segment is estimated to witness significant growth during the forecast period.

Electronic manufacturing services anchor modern clinical infrastructure by facilitating the integration of wireless connectivity into active diagnostic and therapeutic hardware.

Outsourcing the intricate surface mount technology placement and micro electronics packaging required for patient monitoring systems shields medical technology brands from rapid technological obsolescence.

This strategic delegation enables fabricators to deploy advanced in-circuit testing protocols, which improves defect detection accuracy by 15% across high-volume production lines.

Because active implantable devices demand absolute precision, relying on external partners guarantees strict adherence to international electromagnetic compatibility standards. Implementing automated quality assurance frameworks within these dedicated electronic assembly facilities significantly minimizes product scrap expenses.

This continuous operational optimization allows hardware innovators to compress early-stage validation lifecycles and streamline complex electronic assembly workflows without executing massive internal facility expansions.

The EMS segment was valued at USD 42.98 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Medical Device Manufacturing Outsourcing Market Demand is Rising in North America Get Free Sample

Regional manufacturing capabilities heavily dictate the distribution of advanced clinical hardware assembly across international borders. North America dominates complex therapeutic engineering, capturing a massive 39.7% share of incremental volume, driven by demand for life-sustaining cardiovascular and neurological implants.

In contrast, APAC serves as a rapidly expanding hub for high-volume automated manufacturing, scaling localized output by nearly 20% to bypass transcontinental maritime freight premiums.

Because Western original equipment manufacturers face escalating domestic labor inflation, they aggressively establish facilities in emerging regions to ensure supply chain resilience and secure localized access to medical grade polymers and high purity titanium.

This deliberate geographic diversification helps fabricators navigate strict regulatory compliance frameworks while satisfying regional green procurement mandates. Consequently, localized production networks reduce cross-border transportation delays by 25%.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The operational landscape for clinical hardware is heavily dependent on advanced engineering partnerships capable of managing highly regulated workflows. As healthcare innovators push the boundaries of connected therapeutics, the demand for advanced drug delivery combination products has surged, requiring intricate electro mechanical integration.

- Contract manufacturers actively deploy specialized high risk surgical robotics infrastructure to validate complex automated mechanisms before full-scale commercialization. This transition reduces internal prototyping costs and accelerates market entry. To maintain flawless quality metrics, outsourced facilities heavily invest in automated laboratory diagnostic equipment integration, aligning multi jurisdictional validation protocols under a unified digital framework.

- Furthermore, implantable medical device trace verification ensures that active components comply with stringent international safety guidelines. Because modern cleanroom particle count automated monitoring replaces manual environmental testing, manufacturers can reduce atmospheric contamination risks by approximately 22%. This indirect operational enhancement protects sensitive micro-electronics from bio-fluid intrusion, ensuring that complete diagnostic platforms achieve flawless structural reproducibility.

- By leveraging these comprehensive technological ecosystems, original equipment manufacturers successfully insulate their corporate supply lines from volatile capital expenditure cycles while delivering cutting-edge therapeutic hardware to the global healthcare network.

What are the key market drivers leading to the rise in the adoption of Medical Device Manufacturing Outsourcing Industry?

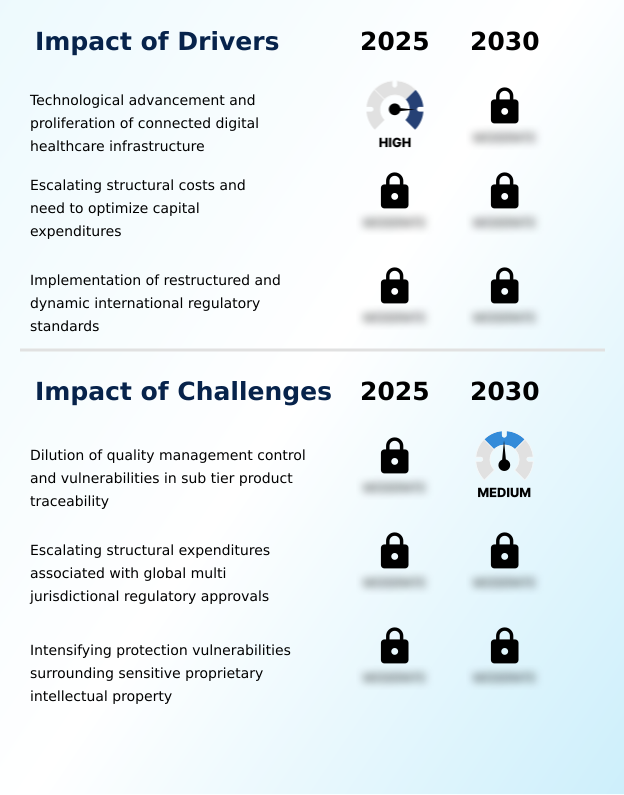

- Continuous technological advancement and the proliferation of connected digital healthcare infrastructure serve as the primary drivers propelling market expansion.

- Escalating structural costs and the demand for connected healthcare infrastructure compel original equipment manufacturers to scale external production partnerships. Modern clinical hardware requires sophisticated cleanroom assembly and precise embedded software integration, demanding specialized engineering capabilities that many brands lack internally.

- By transitioning production to expert outsourced facilities, device innovators achieve massive capital expenditure optimization and reduce internal operational costs by an estimated 15%.

- This structural shift enables healthcare brands to access advanced design for manufacturability assessments without building new cleanrooms, improving product commercialization timelines by nearly 20%.

- Because building high-grade cleanrooms involves massive financial risk, relying on third-party fabricators successfully converts fixed operational costs into variable expenses, allowing brands to focus on core research and clinical trials.

What are the market trends shaping the Medical Device Manufacturing Outsourcing Industry?

- The accelerated transition toward comprehensive, end-to-end contract development and manufacturing service models acts as a prominent trend redefining the operational landscape.

- The Medical Device Manufacturing Outsourcing landscape is transitioning from fragmented component sourcing toward highly integrated, end-to-end operational partnerships. Implementing advanced automated optical inspection systems powered by convolutional neural networks allows fabricators to identify sub-micron structural anomalies in real time.

- This technological shift directly improves quality control throughput, as inspection downtime is reduced by 30% while defect detection accuracy improves by 18%. Because hospital networks enforce zero-tolerance quality thresholds, contract partners rely on machine learning networks to maintain flawless component reproducibility. By substituting manual reviews with autonomous validation, manufacturers establish unalterable electronic quality records that accelerate time-to-market.

- The integration of artificial intelligence across assembly floors optimizes capital expenditures and delivers an estimated 25% boost in overall manufacturing efficiency.

What challenges does the Medical Device Manufacturing Outsourcing Industry face during its growth?

- The dilution of quality management control and vulnerabilities in sub-tier product traceability remain critical challenges constraining seamless industry integration.

- Maintaining direct oversight over operational workflows presents a major structural limitation for distributed supply chains. When brands delegate fabrication to external partners, vulnerabilities in sub tier product traceability emerge, increasing the risk of unvalidated material substitutions. This loss of direct quality control negatively impacts compliance timelines, as identifying micro-electronic defects requires complex sterile barrier validation across extended supplier networks.

- Furthermore, escalating financial burdens associated with multi jurisdictional validation compress the profit margins of contract manufacturers by nearly 12% during inflationary cycles. Because shared production environments handle multiple competing medical technology brands simultaneously, maintaining strict intellectual property containment becomes exceptionally difficult.

- Consequently, original equipment manufacturers face a 25% increase in administrative overhead to audit external facilities and ensure secure data isolation.

Exclusive Technavio Analysis on Customer Landscape

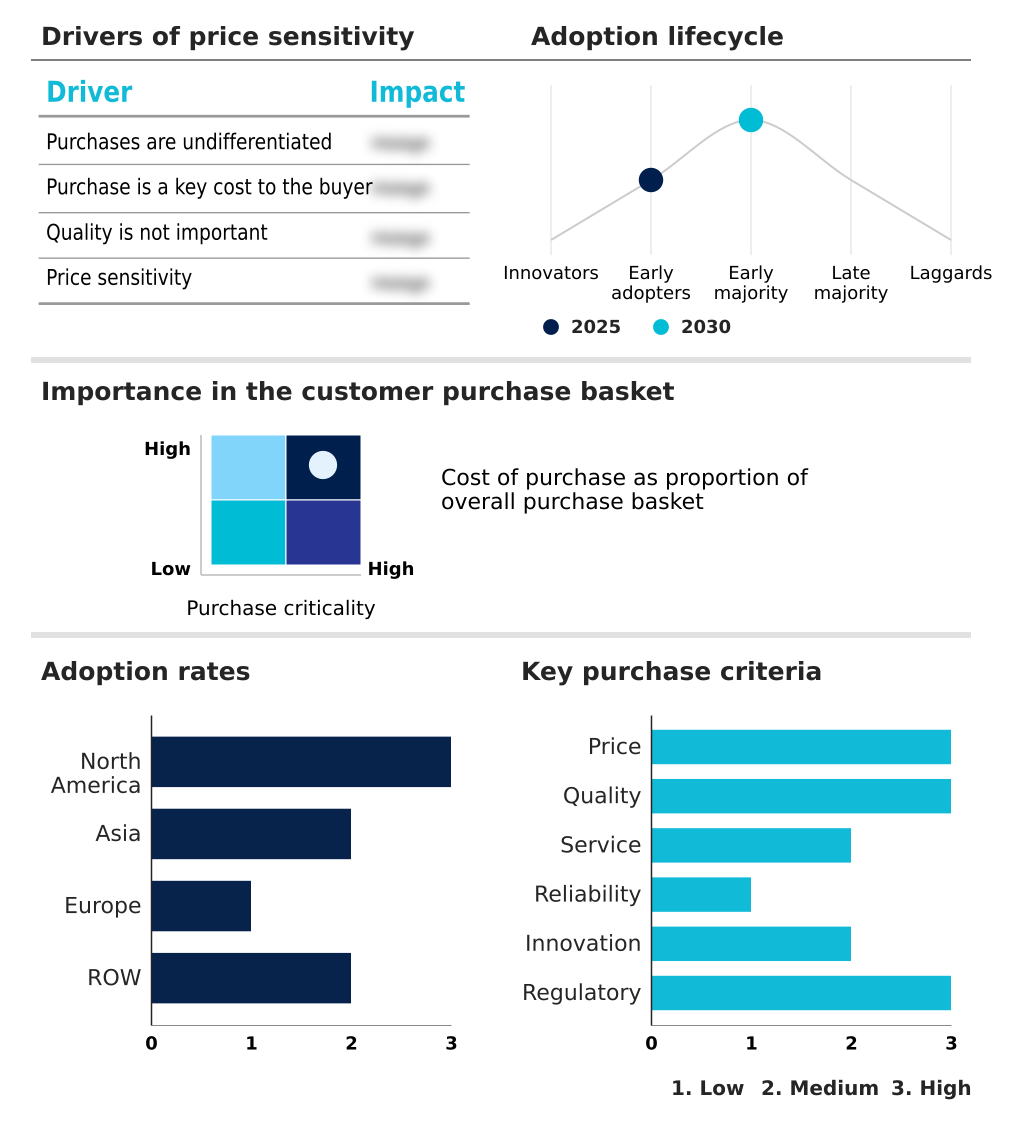

The medical device manufacturing outsourcing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the medical device manufacturing outsourcing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Medical Device Manufacturing Outsourcing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, medical device manufacturing outsourcing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Benchmark Electronics Inc. - Comprehensive medical device manufacturing outsourcing includes complex component assembly, precision micro molding, and regulatory compliance testing, ensuring reliable production scale for advanced healthcare technology developers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Benchmark Electronics Inc.

- Cadence Inc.

- Celestica Inc.

- Charles River

- Eurofins Scientific SE

- Flex Ltd.

- Gerresheimer AG

- Integer Holdings Corp.

- Intertek Group Plc

- IQVIA Holdings Inc.

- Jabil Inc.

- Nortech Systems Inc.

- Plexus Corp.

- Sanmina Corp.

- SGS SA

- TE Connectivity plc

- Tecan Trading AG

- Thermo Fisher Scientific Inc.

- West Pharma Services Inc.

- WuXi AppTec Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Medical device manufacturing outsourcing market

- In the Health Care Equipment industry, the rapid integration of artificial intelligence-powered diagnostic imaging platforms has accelerated the need for sophisticated sensor integration, directly impacting Medical Device Manufacturing Outsourcing demand by requiring specialized cleanroom electronic assembly.

- The global transition toward decentralized home-based patient monitoring systems has increased the production volume of wireless telemetry components, directly impacting Medical Device Manufacturing Outsourcing demand by driving investments in automated micro-molding and surface mount technology capacities.

- Strict enforcement of the European Medical Device Regulation has imposed rigorous total component traceability mandates across the supply chain, directly impacting Medical Device Manufacturing Outsourcing demand by compelling OEMs to partner exclusively with digitally integrated, highly compliant fabricators.

- Advancements in high-performance bio-compatible polymers for minimally invasive surgical tools have shifted raw material processing requirements, directly impacting Medical Device Manufacturing Outsourcing demand by increasing reliance on external extrusion and custom thermoplastic molding specialists.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Medical Device Manufacturing Outsourcing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 328 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12% |

| Market growth 2026-2030 | USD 68893.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.6% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Thailand, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Saudi Arabia, UAE, South Africa, Argentina, Colombia, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Strategic reliance on third-party engineering infrastructure allows medical technology brands to navigate volatile macroeconomic cycles while maintaining continuous product innovation. The integration of advanced artificial intelligence into factory quality control systems enables contract manufacturers to identify structural anomalies in real time.

- This technological shift directly supports boardroom-level compliance and budgeting strategies by converting massive fixed facility costs into variable operational expenses. As a result, companies have achieved a 30% reduction in processing time for complex electro mechanical assemblies. Furthermore, the rapid geographic decentralization of manufacturing assets into emerging high-capability hubs protects original equipment manufacturers from cross-border trade disruptions.

- By establishing localized production nodes, fabricators ensure uninterrupted access to critical surgical components and bio compatible ceramics. The continuous adoption of deep learning optical setups effectively replaces slow human review loops, establishing an unalterable ledger of compliance that safeguards proprietary intellectual property. These operational enhancements provide a highly resilient supply chain foundation.

What are the Key Data Covered in this Medical Device Manufacturing Outsourcing Market Research and Growth Report?

-

What is the expected growth of the Medical Device Manufacturing Outsourcing Market between 2026 and 2030?

-

USD 68.89 billion, at a CAGR of 12%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (EMS, Raw materials, and Finished goods), Class Type (Class II, Class III, and Class I), Service Type (Manufacturing services, Quality assurance and testing, Device development and design services, and Regulatory and certification support), End-user (Medical device companies, Pharmaceutical and biotech firms, Hospitals and clinics, and Research institutions) and Geography (North America, Asia, Europe, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Asia, Europe and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Technological advancement and proliferation of connected digital healthcare infrastructure, Dilution of quality management control and vulnerabilities in sub tier product traceability

-

-

Who are the major players in the Medical Device Manufacturing Outsourcing Market?

-

Benchmark Electronics Inc., Cadence Inc., Celestica Inc., Charles River, Eurofins Scientific SE, Flex Ltd., Gerresheimer AG, Integer Holdings Corp., Intertek Group Plc, IQVIA Holdings Inc., Jabil Inc., Nortech Systems Inc., Plexus Corp., Sanmina Corp., SGS SA, TE Connectivity plc, Tecan Trading AG, Thermo Fisher Scientific Inc., West Pharma Services Inc. and WuXi AppTec Co. Ltd.

-

Market Research Insights

- The Medical Device Manufacturing Outsourcing ecosystem is defined by structural shifts toward advanced automation and localized supply chain resilience. Escalating structural costs and the need for capital expenditure optimization compel original equipment manufacturers to adopt robust quality management systems through third-party partnerships.

- Implementing automated optical inspection reduces manual review delays and improves overall testing accuracy by 18%, significantly lowering post market surveillance risks. Furthermore, shifting high-volume production to nearshore geographic zones minimizes cross-border logistics costs by an estimated 15%.

- This strategic reliance on external product commercialization timelines allows medical innovators to maintain strict adherence to good manufacturing practices without sustaining massive internal overhead, thereby driving long-term operational efficiency.

We can help! Our analysts can customize this medical device manufacturing outsourcing market research report to meet your requirements.

RIA -

RIA -