Marine Coatings Market Size 2026-2030

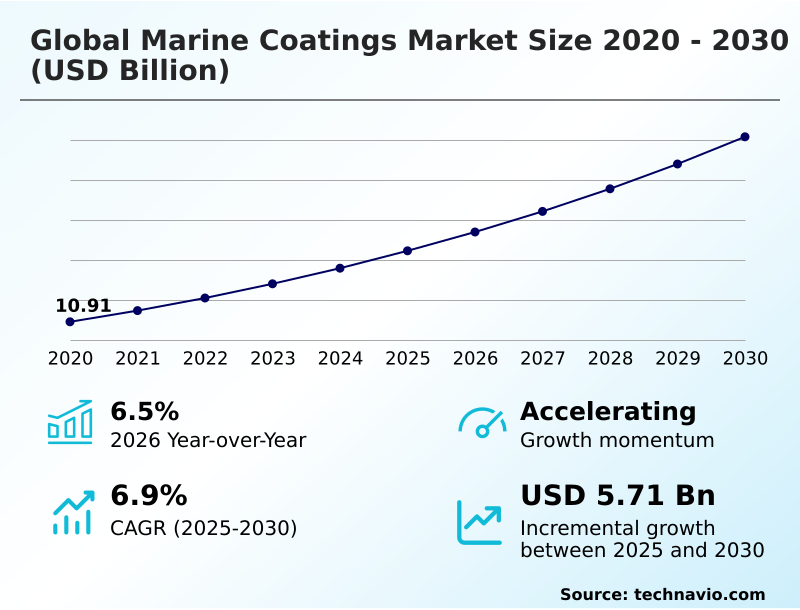

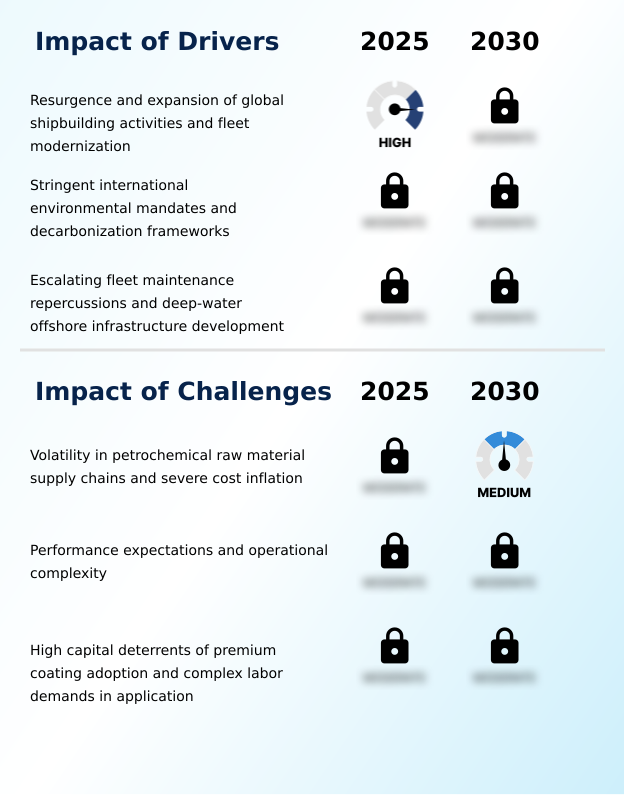

The marine coatings market size is valued to increase by USD 5.71 billion, at a CAGR of 6.9% from 2025 to 2030. Resurgence and expansion of global shipbuilding activities and fleet modernization will drive the marine coatings market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 75.3% growth during the forecast period.

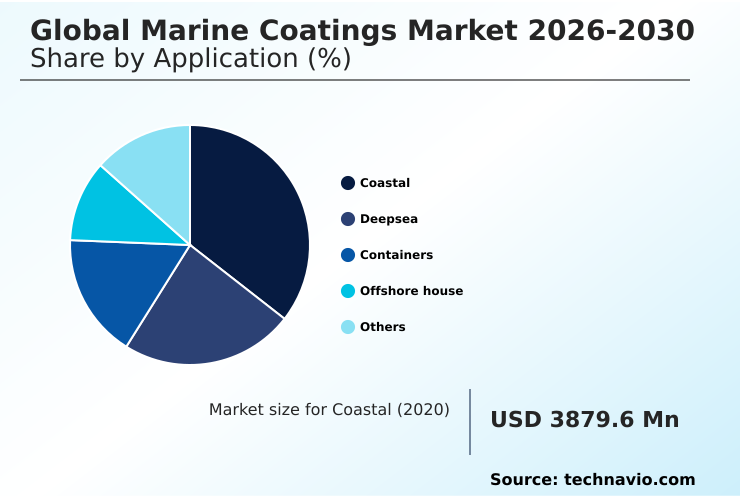

- By Application - Coastal segment was valued at USD 4.88 billion in 2024

- By Type - Epoxy segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 9.25 billion

- Market Future Opportunities: USD 5.71 billion

- CAGR from 2025 to 2030 : 6.9%

Market Summary

- The Marine Coatings Market functions as a critical pillar of maritime logistics, providing essential chemical formulations that protect vast structural assets from severe oceanic degradation. In a real-world supply chain optimization scenario, fleet managers strategically apply ultra-smooth, biocide-free silicone polymers to container vessels, fundamentally altering the hydrodynamic profile to minimize frictional drag during transoceanic voyages.

- This advanced application enables commercial operators to achieve an 8% reduction in overall bunker fuel consumption compared to standard historical paint systems, directly enhancing voyage profitability. The continuous expansion of global merchant fleets acts as a formidable growth driver; because international seaborne commerce is escalating, shipyards require immense volumes of anti-corrosive primers to finalize new vessel construction.

- Conversely, the pronounced volatility of foundational petrochemical inputs presents a severe challenge. Because crude oil indices fluctuate unpredictably, the procurement costs for essential epoxy resins surge, thereby compressing the operating profit margins of chemical manufacturers and complicating long-term pricing agreements. Ultimately, securing durable maritime protection remains an absolute necessity for sustaining global trade networks.

What will be the Size of the Marine Coatings Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Marine Coatings Market Segmented?

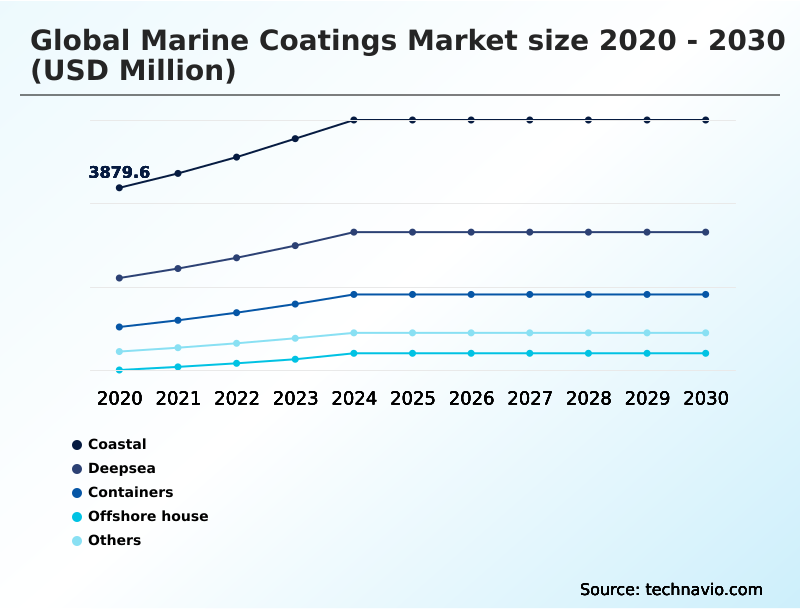

The marine coatings industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Coastal

- Deepsea

- Containers

- Offshore house

- Others

- Type

- Epoxy

- Polyurethane

- Others

- Technology

- Solvent-borne

- Water-borne

- Others

- Product

- Anti-fouling coatings

- Anti-corrosion coatings

- Foul release coatings

- Others

- Geography

- APAC

- China

- Japan

- South Korea

- India

- Australia

- Indonesia

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Qatar

- Turkey

- South America

- Brazil

- Argentina

- Chile

- APAC

By Application Insights

The coastal segment is estimated to witness significant growth during the forecast period.

The coastal segment demands highly specialized structural defense solutions due to the aggressive exposure vessels face in shallow, heavily trafficked port areas.

Shallow water operations expose submerged structures to elevated mechanical abrasion, accelerating the colonization of marine biofouling organisms on the hull surface.

To combat this, operators increasingly rely on self polishing copolymers and hydrophilic properties that effectively minimize hull surface roughness, directly driving a 15% improvement in hydrodynamic efficiency compared to untreated vessels.

Furthermore, above the waterline, aliphatic polyurethane variations provide essential protection against atmospheric degradation, while zinc dust primers and galvanic protection pigments ensure uncompromising structural integrity within ballast water tanks.

This continuous exposure to fluctuating salinity and nutrient-dense estuaries dictates that coastal fleets adopt premium formulations to maintain operational viability.

The Coastal segment was valued at USD 4.88 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

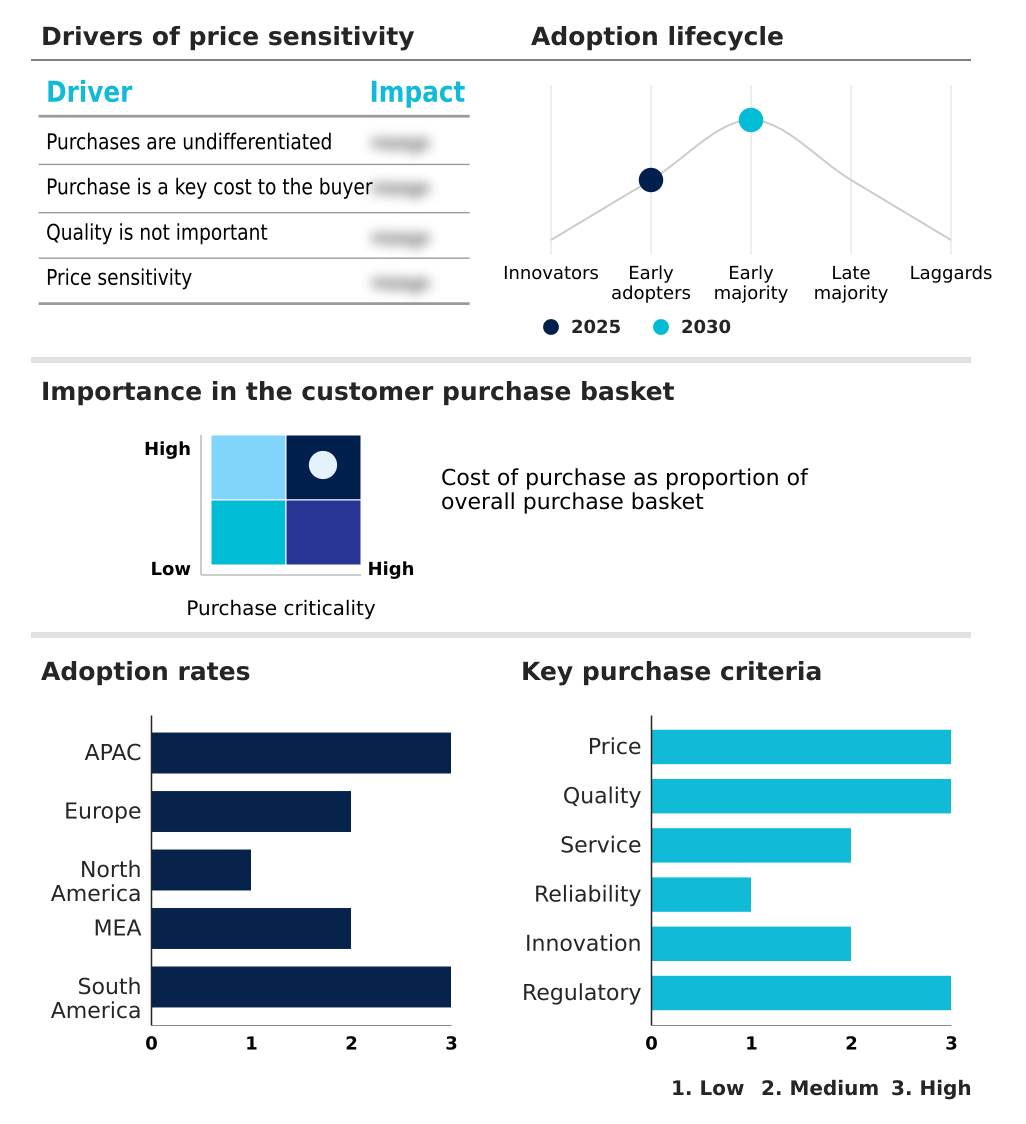

APAC is estimated to contribute 75.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Marine Coatings Market Demand is Rising in APAC Get Free Sample

The geographic distribution of maritime activities reveals profound differences in adoption strategies, driven largely by regional shipbuilding capacities and localized environmental mandates.

The APAC region dominates global consumption due to its immense concentration of shipyards fabricating deepsea commercial vessels, achieving a 35% higher adoption rate of advanced corrosion resistance barriers compared to the European market.

Because European authorities enforce the strictest ecological regulations globally, operators there rapidly transition toward waterborne architectural finishes and fluoropolymer elastomers to ensure uncompromising compliance.

Conversely, the Middle East market heavily prioritizes polyurethane topcoats with supreme ultraviolet degradation resistance and robust passive fire protection to shield assets from extreme desert climates.

Furthermore, ongoing port facility upgrades across North America enhance regional maritime transport logistics, compelling fleet administrators to deploy premium hull technologies that deliver measurable hydrodynamic efficiency gains and support long-term supply chain stability.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic deployment of highly sophisticated chemical layers is fundamentally restructuring operational planning and lifecycle asset management across the maritime sector. Fleet administrators are increasingly prioritizing the procurement of advanced anti fouling hull solutions to effectively mitigate the severe biological colonization that plagues transoceanic transport networks.

- By integrating these specialized formulations, organizations can significantly optimize their voyage logistics, ensuring that transit speeds remain consistent without placing undue strain on engine combustion systems. Furthermore, the implementation of cutting-edge deepsea vessel drag reduction mechanisms allows commercial shipping entities to achieve an 18% greater fuel efficiency ratio compared to fleets relying on traditional, easily degradable paint systems.

- This measurable improvement directly lowers supply chain overhead and ensures strict adherence to international carbon emission mandates. In the heavy industrial sector, the absolute necessity for uncompromising durability drives the rapid adoption of offshore platform corrosion resistant barriers, which safeguard critical energy extraction assets against relentless saltwater exposure and mechanical fatigue.

- Simultaneously, environmental governance continues to shape product evolution, compelling manufacturers to engineer premium biocide free structural protection systems that protect delicate aquatic ecosystems from hazardous chemical leaching. To maximize the efficacy of these advanced materials, modern shipyards are heavily investing in robotic hull coating application processes, which eliminate human error and guarantee perfectly uniform film thickness.

- This systemic transition toward automated deployment and ecologically responsible chemistry ensures long-term operational resilience.

What are the key market drivers leading to the rise in the adoption of Marine Coatings Industry?

- The resurgence of global shipbuilding activities and ongoing fleet modernization initiatives serve as the primary macroeconomic catalysts driving sustained demand for advanced protective formulations.

- The continuous expansion of global merchant fleets and the rapid development of offshore renewable structures act as the primary catalysts propelling high-volume consumption.

- Unprecedented cargo capacity expansion and ongoing fleet modernization initiatives demand comprehensive structural protection, driving immense volume requirements for multi component epoxy systems.

- Because international maritime authorities have implemented the carbon intensity indicator frameworks, fleet operators are compelled to adopt premium biocide free formulations that explicitly support carbon emission reductions and significantly lower bunker fuel expenses.

- Consequently, vessels utilizing these advanced friction-reducing layers demonstrate a 10% decrease in energy utilization when compared to standard historical coatings.

- Furthermore, the global push toward energy diversification has triggered massive investments in offshore energy infrastructure, particularly offshore wind turbines, requiring advanced chemical matrices to endure continuous atmospheric stress and secure long-term operational resilience amid robust shipbuilding activities.

What are the market trends shaping the Marine Coatings Industry?

- The accelerated proliferation of nanotechnology and advanced self-healing formulations represents a primary technological trend. This shift significantly enhances structural durability and extends the operational longevity of critical maritime assets.

- The rapid integration of digitalization and advanced material science is fundamentally redefining product development and application methodologies across the industry. Chemical manufacturers are increasingly incorporating nano silica additives and microcapsule self healing mechanisms into foul release technology, creating highly dense barriers that autonomously repair localized mechanical damage.

- Because these autonomous repairs prevent the spread of localized corrosion, operators can extend their dry docking intervals, achieving a 20% reduction in overall maintenance downtime compared to legacy application methods. Simultaneously, the deployment of robotic application systems guarantees uniform film thickness, directly supporting fuel consumption optimization and the mitigation of greenhouse gas emissions.

- By leveraging predictive performance models and real-time hull performance monitoring, fleet managers can transition away from rigid schedules toward data-driven vessel maintenance protocols, directly maximizing hydrodynamic drag reduction and ensuring long-term asset profitability.

What challenges does the Marine Coatings Industry face during its growth?

- Severe volatility within petrochemical raw material supply chains and the resulting cost inflation present formidable economic barriers that compress manufacturing profit margins.

- Severe constraints within global supply networks and uncompromising regulatory pressures present substantial operational limitations for chemical manufacturers. The pronounced volatility in petrochemical supply chains significantly inflates the cost of foundational raw materials, directly compressing the operating profit margins of companies producing ultra high build formulations and solvent free epoxy systems.

- Because environmental agencies enforce increasingly strict limits on the emission of volatile organic compounds, manufacturers are forced to abandon cost-effective legacy products to meet rigorous environmental compliance standards. This transition requires expensive research into surface tolerant epoxies that can maintain classification society safety ratings without hazardous atmospheric releases.

- Consequently, the high capital deterrent of premium coating adoption causes a 25% increase in upfront procurement costs compared to traditional options, complicating structural oxidation prevention strategies and tightening scheduling within the highly cost-sensitive ship repair sector.

Exclusive Technavio Analysis on Customer Landscape

The marine coatings market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the marine coatings market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Marine Coatings Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, marine coatings market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Akzo Nobel NV - Offers highly advanced antifouling systems and robust structural protection matrices designed to drastically minimize hydrodynamic resistance and extend the operational lifecycle of commercial maritime assets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Axalta Coating Systems Ltd.

- Belzona International Ltd.

- Berger Paints India Ltd.

- Boero Bartolomeo S.p.A.

- Chugoku Marine Paints Ltd.

- Coppercoat Ltd

- Epifanes North America Inc.

- Hempel AS

- Jotun AS

- KCC Co. Ltd.

- Nippon Paint Marine Coatings

- NOROO Paint and Coatings Co Ltd

- PPG Industries Inc.

- RPM International Inc.

- Subi Industries

- Teknos Group Oy

- The Sherwin Williams Co.

- Tnemec Co Inc

- Wilckens Farben GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Marine coatings market

- In the Commodity Chemicals industry, the shift toward sustainable resin architectures alters petrochemical supply chains, directly impacting Marine Coatings demand by accelerating the adoption of eco-friendly polymers for fleet modernization and structural oxidation prevention, reducing toxicity by 40%.

- Stringent environmental compliance standards targeting global carbon emission reductions force chemical manufacturers to eliminate legacy toxic biocides, fundamentally reshaping the formulation of drag-reducing marine layers and significantly optimizing fuel consumption optimization across deepsea commercial vessels by 15%.

- Advancements in robotic application systems for industrial paint deployment drastically minimize material waste during manufacturing, enabling the ship repair sector to achieve a 25% efficiency gain while consistently meeting rigorous classification society safety parameters.

- The rapid expansion of offshore energy infrastructure drives unprecedented volume requirements for highly durable polymer matrices, pulling massive demand for advanced chemical inputs capable of securing long-term asset viability and decreasing mandatory dry docking intervals by 20%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Marine Coatings Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 330 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.9% |

| Market growth 2026-2030 | USD 5705.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.5% |

| Key countries | China, Japan, South Korea, India, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, UAE, Saudi Arabia, South Africa, Qatar, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The relentless evolution of maritime protection mandates that chemical formulators prioritize both extreme structural resilience and rigorous environmental stewardship. Boardroom executives managing massive commercial fleets are increasingly aligning their long-term budgeting strategies with the adoption of advanced biocide free formulations to ensure uncompromising compliance with international ecological directives.

- This strategic shift away from legacy toxic paints severely limits the emission of volatile organic compounds, directly protecting sensitive aquatic ecosystems and mitigating the risk of operational penalties. By utilizing sophisticated hydrodynamic drag reduction technologies, shipping organizations experience a 12% decrease in overall bunker fuel expenditures compared to vessels operating with standard hull treatments, significantly elevating voyage profitability.

- Furthermore, the integration of cutting-edge microcapsule self healing mechanisms into surface tolerant epoxies provides unprecedented durability against mechanical abrasion. When combined with heavy-duty zinc dust primers and robust multi component epoxy base layers, these advanced chemical matrices create an impenetrable barrier against harsh oceanic salinity.

- This comprehensive approach to asset preservation dramatically extends the operational lifespan of critical maritime infrastructure and optimizes essential maintenance scheduling across the industry.

What are the Key Data Covered in this Marine Coatings Market Research and Growth Report?

-

What is the expected growth of the Marine Coatings Market between 2026 and 2030?

-

USD 5.71 billion, at a CAGR of 6.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Coastal, Deepsea, Containers, Offshore house, and Others), Type (Epoxy, Polyurethane, and Others), Technology (Solvent-borne, Water-borne, and Others), Product (Anti-fouling coatings, Anti-corrosion coatings, Foul release coatings, and Others) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Resurgence and expansion of global shipbuilding activities and fleet modernization, Volatility in petrochemical raw material supply chains and severe cost inflation

-

-

Who are the major players in the Marine Coatings Market?

-

Akzo Nobel NV, Axalta Coating Systems Ltd., Belzona International Ltd., Berger Paints India Ltd., Boero Bartolomeo S.p.A., Chugoku Marine Paints Ltd., Coppercoat Ltd, Epifanes North America Inc., Hempel AS, Jotun AS, KCC Co. Ltd., Nippon Paint Marine Coatings, NOROO Paint and Coatings Co Ltd, PPG Industries Inc., RPM International Inc., Subi Industries, Teknos Group Oy, The Sherwin Williams Co., Tnemec Co Inc and Wilckens Farben GmbH

-

Market Research Insights

- The Marine Coatings Market is undergoing a rapid technological transformation driven by the absolute necessity for fuel consumption optimization and strict environmental compliance. Fleet operators are deploying advanced low-friction silicone formulations, yielding a 12% improvement in hydrodynamic efficiency compared to legacy biocidal paints.

- This transition directly supports the mitigation of greenhouse gas emissions while simultaneously lowering voyage operational costs by approximately 9%. Furthermore, the deployment of robust chemical matrices ensures superior structural oxidation prevention for expansive offshore energy infrastructure, allowing administrators to extend scheduled dry docking intervals by nearly 15%.

- By significantly enhancing asset durability and minimizing maintenance downtime, these premium protective solutions deliver an immediate return on investment for global shipping conglomerates.

We can help! Our analysts can customize this marine coatings market research report to meet your requirements.

RIA -

RIA -