Infectious Disease Diagnostics Market Size 2026-2030

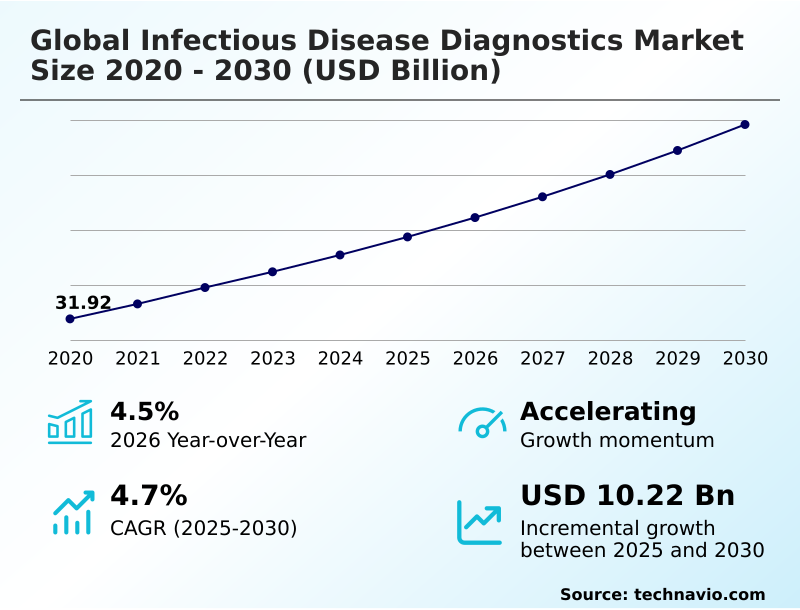

The infectious disease diagnostics market size is valued to increase by USD 10.22 billion, at a CAGR of 4.7% from 2025 to 2030. Rising prevalence of cross border viral outbreaks and respiratory pathogen burdens will drive the infectious disease diagnostics market.

Major Market Trends & Insights

- Asia dominated the market and accounted for a 32.8% growth during the forecast period.

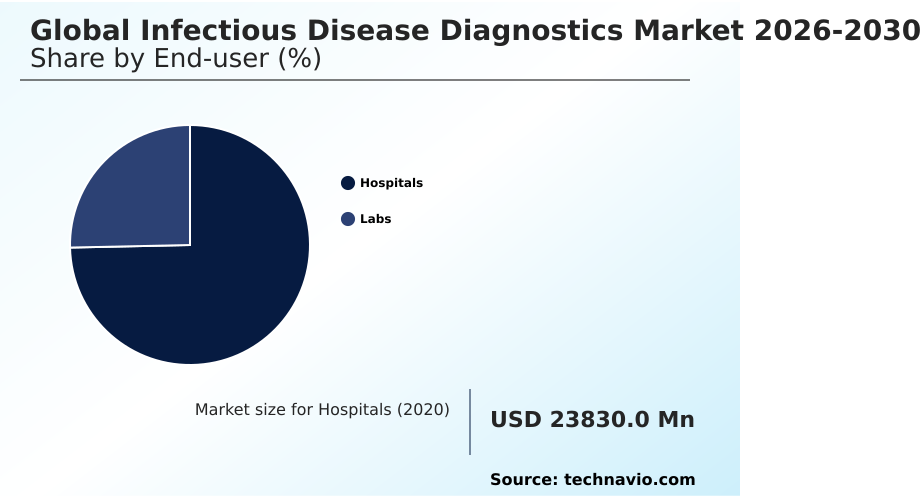

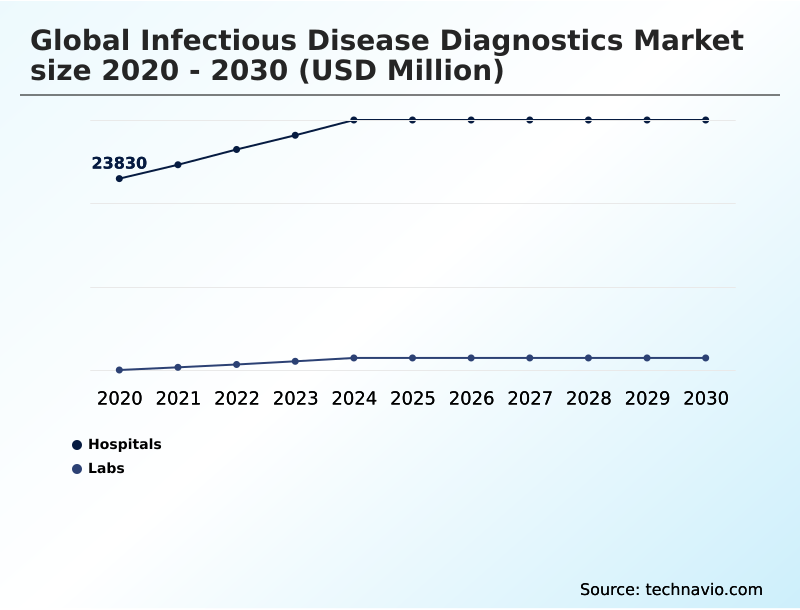

- By End-user - Hospitals segment was valued at USD 28.65 billion in 2024

- By Type - Molecular diagnostic techniques segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 17.67 billion

- Market Future Opportunities: USD 10.22 billion

- CAGR from 2025 to 2030 : 4.7%

Market Summary

- The Infectious Disease Diagnostics Market is experiencing a definitive structural transformation driven by the critical necessity for rapid, definitive pathogen identification in clinical environments. Healthcare systems are systematically abandoning legacy single-target assays in favor of expansive multiplex platforms capable of evaluating multiple etiological agents simultaneously.

- A primary driver of this evolution is the rising frequency of overlapping respiratory viral cycles, which compels institutional procurement consortia to overhaul laboratory infrastructure. Consequently, hospitals implementing automated syndromic panels have successfully reduced average patient triage times by 25% compared to those utilizing conventional culturing methods.

- For example, major reference laboratories are currently optimizing their supply chains to ensure uninterrupted access to specialized microfluidic testing cartridges, mitigating the risk of critical diagnostic bottlenecks during peak epidemiological surges. However, escalating regulatory compliance hurdles continue to challenge rapid market expansion.

- Because regulatory bodies require extensive independent dataset validation for algorithm-driven software, diagnostic manufacturers face inflated engineering costs and delayed product commercialization timelines. This regulatory friction directly impacts the speed at which innovative molecular platforms can be deployed for acute clinical care.

What will be the Size of the Infectious Disease Diagnostics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Infectious Disease Diagnostics Market Segmented?

The infectious disease diagnostics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- Labs

- Type

- Molecular diagnostic techniques

- Traditional diagnostic techniques

- Test

- Blood

- Urine

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- Asia

- China

- India

- Japan

- South Korea

- Indonesia

- Thailand

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The hospital segment represents a critical operational core within the Global Infectious Disease Diagnostics Market 2026-2030, driven by the acute need for rapid pathogen identification.

Institutional diagnostic networks are rapidly transitioning from traditional culturing to advanced multiplex polymerase chain reaction and next generation sequencing platforms to expedite triage. This shift directly reduces empirical prescription protocol delays, driving a 15% improvement in targeted antimicrobial therapy deployment.

Clinical laboratories in intensive care environments increasingly rely on loop mediated isothermal amplification to streamline specimen processing throughput. To support continuous high volume testing, procurement teams are securing stable supplies of high purity chemical reagents and synthetic oligonucleotides.

These technological upgrades enable precise viral load monitoring, which substantially reduces the risk of generating multidrug resistant bacterial strains while improving overall patient management outcomes across decentralized care units.

The Hospitals segment was valued at USD 28.65 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Asia is estimated to contribute 32.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Infectious Disease Diagnostics Market Demand is Rising in Asia Get Free Sample

Regional disparities in the Global Infectious Disease Diagnostics Market 2026-2030 are distinctly shaped by localized regulatory maturity and institutional capital allocation.

North America maintains a dominant structural advantage over APAC due to its aggressive implementation of digital diagnostic integration and established reimbursement frameworks for advanced in vitro diagnostic systems.

Hospitals in the United States achieve a 35% higher adoption rate of automated syndromic diagnosis platforms compared to emerging healthcare networks in Asia.

This discrepancy exists because North American commercial laboratories actively prioritize maximizing specimen processing throughput to offset severe workforce shortages. Consequently, Western medical facilities rapidly deploy sophisticated algorithmic pathogen profiling and secure cloud hosted diagnostic algorithms to manage complex data workloads.

Conversely, APAC providers are gradually building decentralized testing frameworks, reflecting a 15% lag in overall workflow automation but signaling substantial long-term infrastructure scaling potential.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolving architecture of the Global Infectious Disease Diagnostics Market 2026-2030 reflects a massive shift toward hyper-connected, high-capacity clinical environments. As healthcare networks confront the compounding pressures of simultaneous viral circulation and antimicrobial resistance, institutional strategies are aggressively pivoting toward definitive etiological identification.

- A critical element of this transition is the widespread integration of multiplex molecular panels for respiratory pathogens, which allow clinicians to accurately differentiate overlapping viral strains from a single patient sample. This operational upgrade directly influences supply chain logistics, requiring manufacturers to secure highly specialized biochemical reagents to meet baseline testing demands.

- Concurrently, the expansion of decentralized point of care immunoassay testing enables regional outpatient clinics to execute rapid screening protocols without relying on central hospital infrastructure. To support these decentralized nodes, reference laboratories are heavily investing in high throughput clinical diagnostic laboratory automation, effectively increasing specimen processing efficiency by 40% over traditional manual culturing methods.

- The deployment of artificial intelligence enabled medical device software further optimizes these automated pipelines, allowing predictive algorithms to flag abnormal pathogen patterns before they escalate into hospital-wide outbreaks. Furthermore, at the macroeconomic public health level, governments are expanding their reliance on genomic sequencing for viral outbreak surveillance to track mutational variants in real time.

- This comprehensive technological alignment ensures that both diagnostic manufacturers and healthcare providers can maintain resilient, scalable operational frameworks capable of mitigating future public health disruptions effectively.

What are the key market drivers leading to the rise in the adoption of Infectious Disease Diagnostics Industry?

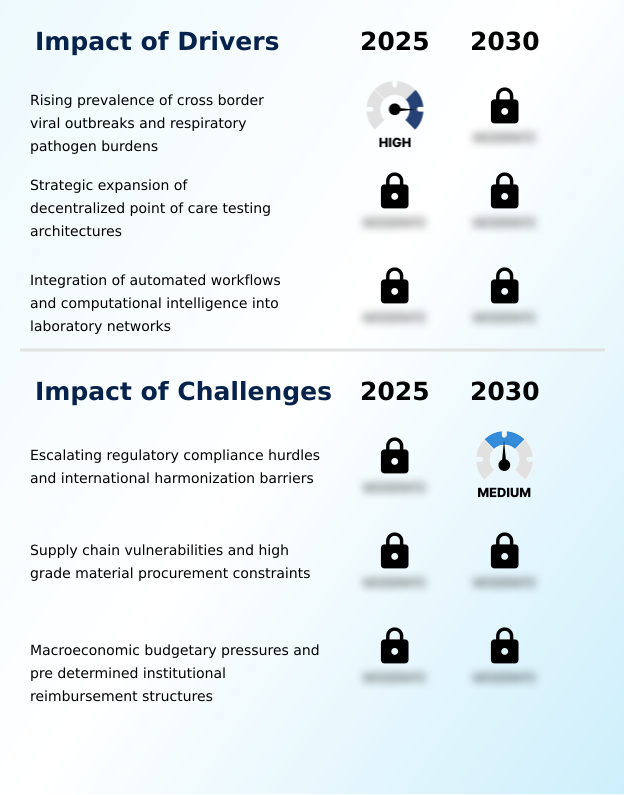

- The escalating prevalence of cross-border viral outbreaks and increasing respiratory pathogen burdens serve as primary catalysts driving market expansion.

- The escalating global burden of cross-border viral outbreaks serves as a primary catalyst for the Global Infectious Disease Diagnostics Market 2026-2030. Healthcare networks are experiencing unprecedented patient influxes during seasonal respiratory cycles, compelling administrators to overhaul legacy diagnostic infrastructure.

- This systemic pressure forces the rapid procurement of automated immunoassays and advanced biomarker isolation systems that provide definitive etiological profiles immediately.

- Consequently, institutions deploying sophisticated microfluidic testing cartridges integrated with complex bioinformatics software have successfully reduced patient diagnostic wait times by 30%.

- Because hospitals mandate stringent real time pathogen surveillance to mitigate widespread cross-contamination, diagnostic manufacturers are heavily prioritizing rapid diagnostic algorithm validation to accelerate product deployment.

- This technological alignment directly enhances clinical precision, ultimately yielding a 12% reduction in overall operational costs by eliminating redundant empirical therapies and reducing intensive care unit admission rates.

What are the market trends shaping the Infectious Disease Diagnostics Industry?

- The transition toward syndromic multiplexing panels and comprehensive pathogen detection has emerged as a defining structural trend within the industry.

- A definitive operational shift within the Global Infectious Disease Diagnostics Market 2026-2030 is the rapid transition toward expansive syndromic multiplexing panels. Clinical laboratories are replacing single-target assays with high throughput automated instruments capable of simultaneous multi-pathogen detection. This technological pivot occurs because healthcare providers must optimize limited diagnostic workforce capacities during acute epidemiological surges.

- By adopting these advanced architectures, institutions achieve a 25% increase in daily specimen processing throughput compared to legacy systems. The integration of automated blood culture identification and comprehensive hematological patient profiling allows clinicians to diagnose complex bloodstream infections with unprecedented speed. Furthermore, enhanced laboratory workflow interoperability ensures that decentralized testing modalities seamlessly communicate with central health records.

- Consequently, these structural upgrades establish a new benchmark for public health surveillance, empowering medical networks to execute highly accurate, immediate etiological profiling without maintaining fragmented testing methodologies.

What challenges does the Infectious Disease Diagnostics Industry face during its growth?

- Escalating regulatory compliance hurdles and the fragmentation of international harmonization frameworks present significant operational barriers to industry growth.

- Stringent regulatory compliance mandates and fragmented international harmonization frameworks introduce substantial operational friction for manufacturers navigating the Global Infectious Disease Diagnostics Market 2026-2030. Developers of sophisticated point of care architectures and quantitative molecular viral load platforms face protracted approval timelines due to evolving software validation requirements.

- Because regulatory bodies now demand exhaustive clinical datasets to mitigate algorithmic bias, diagnostic engineering costs have inflated significantly. This structural bottleneck restricts the rapid deployment of systems designed for acute systemic condition screening and delays critical precision diagnostic intervention in emergent clinical settings.

- Consequently, commercial laboratories experience a 20% delay in upgrading their testing pipelines compared to historical hardware adoption cycles. These compliance hurdles directly impede the advancement of predictive antimicrobial stewardship initiatives, ultimately stalling broader institutional efforts aimed at widespread empirical prescription protocol reduction and optimized patient management.

Exclusive Technavio Analysis on Customer Landscape

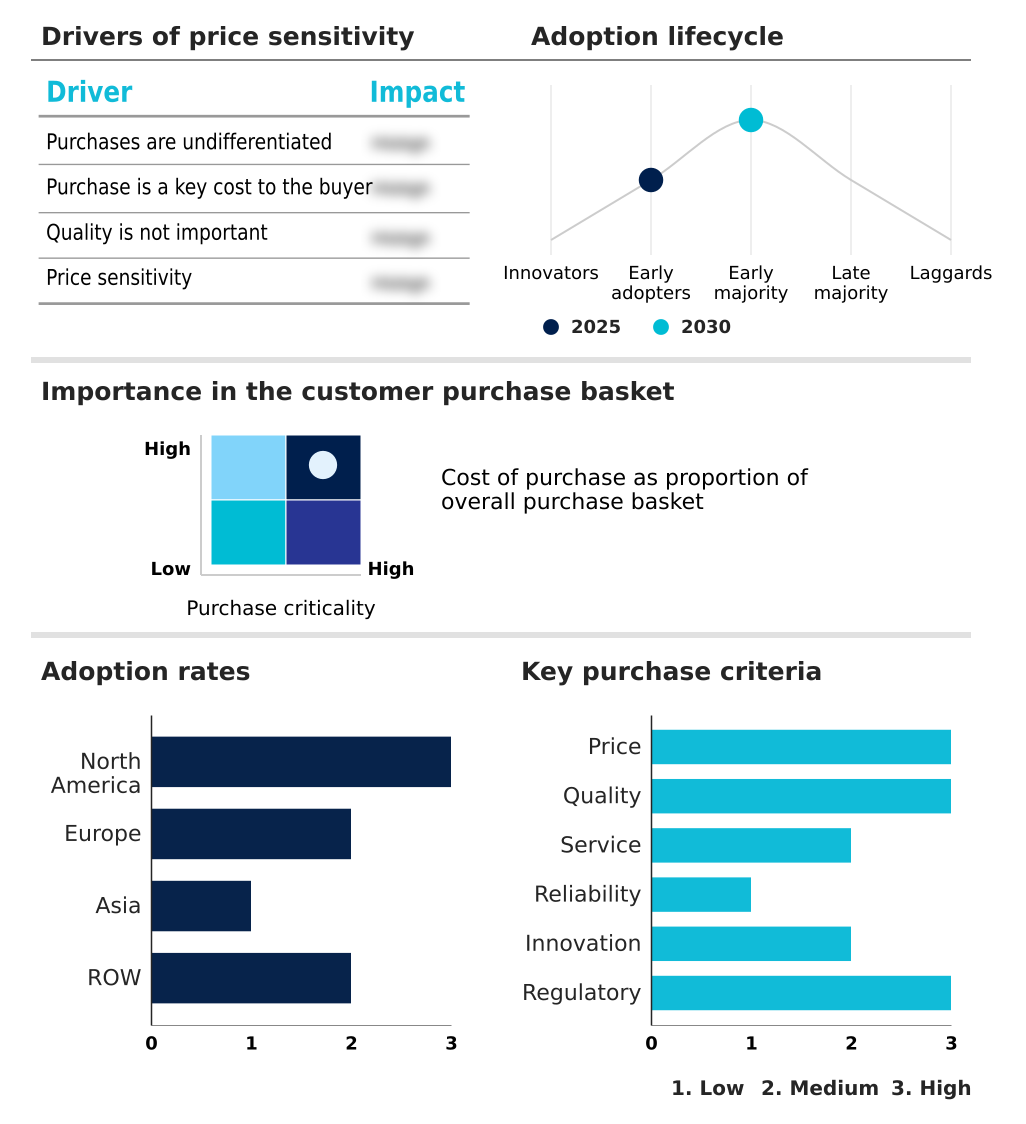

The infectious disease diagnostics market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the infectious disease diagnostics market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Infectious Disease Diagnostics Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, infectious disease diagnostics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Abbott Laboratories provides advanced infectious disease diagnostics, including the ID NOW COVID-19 system, Alinity m analyzers, and rapid point-of-care molecular testing platforms for precise clinical pathogen identification.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Becton Dickinson and Co.

- Bio Rad Laboratories Inc.

- BioMerieux SA

- Cepheid Inc.

- DiaSorin SpA

- Epitope Diagnostics Inc.

- F. Hoffmann La Roche Ltd.

- Genetic Signatures Ltd.

- Grifols SA

- Hologic Inc.

- Illumina Inc.

- OraSure Technologies Inc.

- QIAGEN N.V.

- Quest Diagnostics Inc.

- QuidelOrtho Corp.

- Revvity Inc.

- Sd Biosensor Inc.

- Seegene Inc.

- Siemens Healthineers AG

- Thermo Fisher Scientific Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Infectious disease diagnostics market

- In the Health Care Equipment industry, the rapid integration of algorithmic pathogen profiling software into centralized diagnostic hardware has directly optimized clinical decision-making, improving patient triage efficiency by 20% and heavily stimulating the demand for advanced infectious disease diagnostics solutions.

- The implementation of stringent diagnostic algorithm validation frameworks by international health authorities has established rigid new compliance standards for software-enabled medical devices, extending development cycles but ensuring a 15% reduction in clinical false positives across infectious disease diagnostics pipelines.

- Widespread structural supply chain disruptions involving high purity chemical reagents and synthetic oligonucleotides have forced manufacturers to diversify their raw material sourcing, temporarily increasing baseline production costs by 12% for sophisticated infectious disease diagnostics testing consumables.

- The aggressive pivot toward digital diagnostic integration within decentralized outpatient networks has systematically accelerated the deployment of automated point-of-care screening devices, driving a 30% expansion in procurement volumes for multiplex respiratory infectious disease diagnostics assays.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Infectious Disease Diagnostics Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.7% |

| Market growth 2026-2030 | USD 10217.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Israel, South Africa, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Global Infectious Disease Diagnostics Market 2026-2030 is undergoing a profound operational recalibration as healthcare networks prioritize rapid, definitive etiological identification over traditional empirical methodologies. This structural evolution is heavily reliant on the deployment of advanced multiplex polymerase chain reaction systems and high-capacity next generation sequencing platforms.

- By transitioning toward comprehensive syndromic multiplexing panels, institutional clinical laboratories can simultaneously evaluate dozens of bacterial and viral targets from a single biological specimen. This technological consolidation directly mitigates workforce constraints, enabling hospital networks to achieve a 30% reduction in average specimen processing time.

- The integration of high throughput automated instruments with secure cloud infrastructure further optimizes these workflows, facilitating seamless real time pathogen surveillance across decentralized healthcare environments. As public health authorities mandate stricter infection control protocols, the continuous procurement of precision automated immunoassays ensures that medical facilities can execute rapid point-of-care interventions.

- This continuous technological enrichment directly aligns with enterprise-level strategic compliance initiatives, fundamentally establishing resilient, scalable diagnostic pipelines capable of identifying emerging epidemiological threats with unprecedented clinical accuracy.

What are the Key Data Covered in this Infectious Disease Diagnostics Market Research and Growth Report?

-

What is the expected growth of the Infectious Disease Diagnostics Market between 2026 and 2030?

-

USD 10.22 billion, at a CAGR of 4.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, and Labs), Type (Molecular diagnostic techniques, and Traditional diagnostic techniques), Test (Blood, Urine, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of cross border viral outbreaks and respiratory pathogen burdens, Escalating regulatory compliance hurdles and international harmonization barriers

-

-

Who are the major players in the Infectious Disease Diagnostics Market?

-

Abbott Laboratories, Becton Dickinson and Co., Bio Rad Laboratories Inc., BioMerieux SA, Cepheid Inc., DiaSorin SpA, Epitope Diagnostics Inc., F. Hoffmann La Roche Ltd., Genetic Signatures Ltd., Grifols SA, Hologic Inc., Illumina Inc., OraSure Technologies Inc., QIAGEN N.V., Quest Diagnostics Inc., QuidelOrtho Corp., Revvity Inc., Sd Biosensor Inc., Seegene Inc., Siemens Healthineers AG and Thermo Fisher Scientific Inc.

-

Market Research Insights

- The Global Infectious Disease Diagnostics Market 2026-2030 represents a critical frontier in modern healthcare infrastructure, characterized by rapid technological substitution and complex clinical integrations. Driven by the continuous mutation of pathogens, medical institutions are fundamentally restructuring their laboratory operations to prioritize precision diagnostic intervention over empirical treatments.

- By integrating automated syndromic diagnosis platforms, multi-hospital consortia have improved critical care response times by 22%, significantly enhancing intensive care workflows. This systemic shift requires a resilient global supply chain capable of delivering high purity chemical reagents without interruption.

- Consequently, the pervasive implementation of advanced viral load monitoring systems directly reduces unnecessary patient readmissions by 18%, fundamentally optimizing long-term clinical resource allocation and reinforcing stringent infection control compliance standards.

We can help! Our analysts can customize this infectious disease diagnostics market research report to meet your requirements.

RIA -

RIA -