India Used Car Market Size 2026-2030

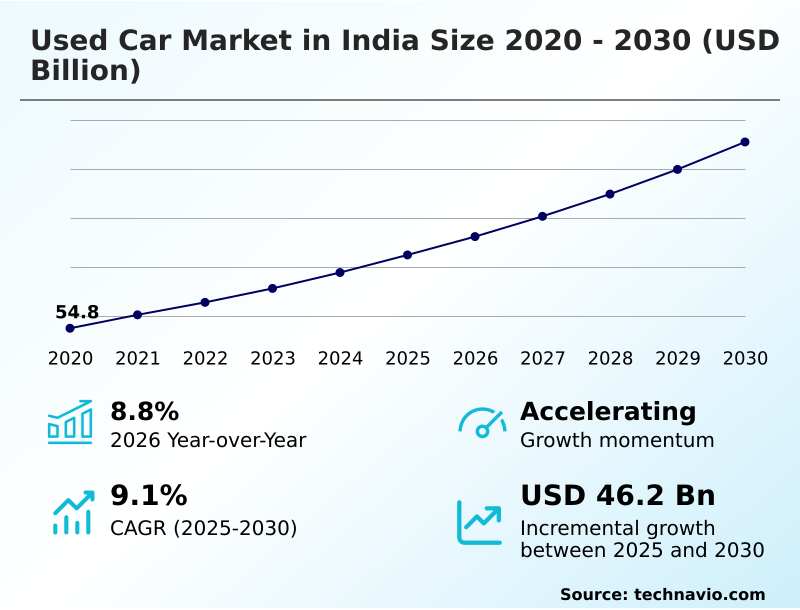

The india used car market size is valued to increase by USD 46.2 billion, at a CAGR of 9.1% from 2025 to 2030. Rising prices of new vehicles and economic accessibility will drive the india used car market.

Major Market Trends & Insights

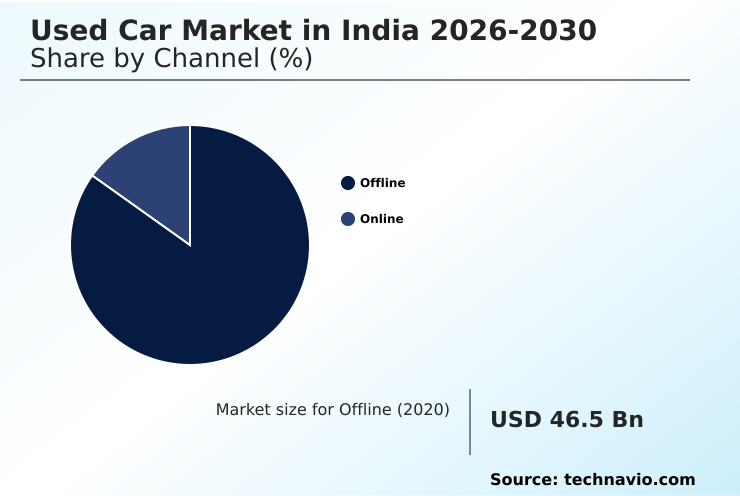

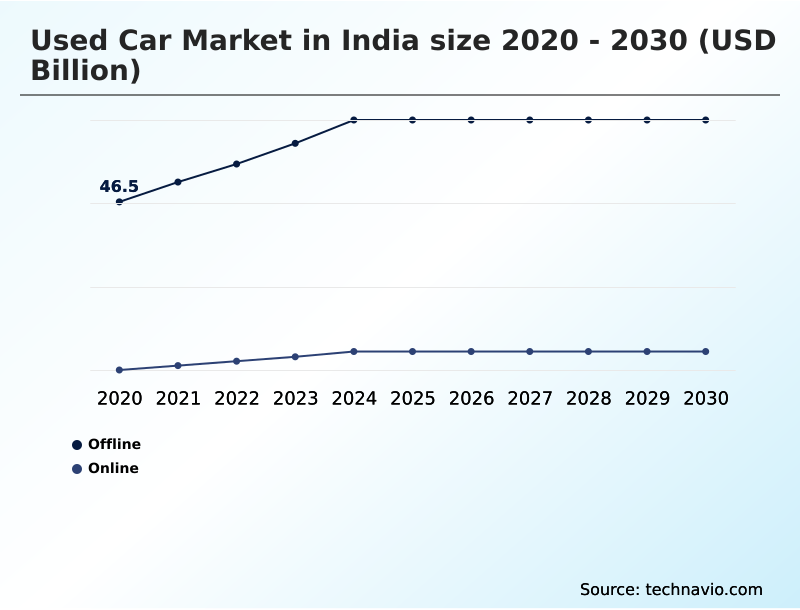

- By Channel - Offline segment was valued at USD 65.1 billion in 2024

- By Vehicle Type - Compact car segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 76.2 billion

- Market Future Opportunities: USD 46.2 billion

- CAGR from 2025 to 2030 : 9.1%

Market Summary

- The Used Car Market in India represents a highly dynamic ecosystem characterized by the continuous exchange of pre-owned passenger vehicles. The escalating affordability gap in the new vehicle segment acts as a structural driver, compelling middle-income households to leverage pre-owned assets for enhanced capital optimization and immediate mobility.

- In a practical business scenario, large-scale multi-brand dealerships have optimized their reverse logistics and refurbishment supply chains, utilizing standardized diagnostic checkpoints to improve vehicle processing efficiency by 24% compared to unorganized independent brokers. This formalization stabilizes year-round transaction volumes and mitigates seasonal procurement volatility.

- However, the systemic lack of a centralized vehicle history database creates a persistent challenge, leading to significant information asymmetry and opaque mechanical histories. This deficit compels buyers to require independent mechanical evaluations, increasing acquisition friction. As original equipment manufacturers expand their certified pre-owned infrastructure, the industry transitions toward a more transparent, digitally integrated mobility landscape.

What will be the Size of the India Used Car Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the India Used Car Market Segmented?

The india used car industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Channel

- Offline

- Online

- Vehicle type

- Compact car

- Mid size

- SUV

- Type

- Petrol

- Diesel

- Others

- Geography

- APAC

- India

- APAC

By Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The physical channel remains the structural foundation of the Used Car market in India, facilitating complex transactions through localized infrastructure. Physical retail nodes, encompassing both standalone entities and a highly organized multi-brand network, command significant transaction velocity.

Consumers prioritize direct pre-owned vehicle procurement to leverage physical test drive infrastructure and verify mechanical integrity. Dealership inventory management systems have modernized these spaces, implementing rigorous multi-point mechanical inspection protocols that improve defect detection by 22% compared to informal channels.

By standardizing the automotive refurbishment workflow, these physical hubs facilitate superior structural damage identification. The integration of aftermarket service ecosystems within certified pre-owned outlets ensures comprehensive support.

Consequently, certified pre-owned standardization acts as a critical friction-reducing mechanism for offline consumer purchasing behavior.

The Offline segment was valued at USD 65.1 billion in 2024 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The structural formalization of the Used Car infrastructure relies heavily on the aggressive deployment of specialized technological frameworks designed to enhance operational transparency and optimize asset lifecycle management. To mitigate the inherent risks of asymmetric information, industry participants are systematically integrating robust certified pre owned vehicle assessment protocols.

- These standardized evaluation mechanisms ensure structural integrity, resulting in a 25% improvement in defect identification compared to traditional localized inspection methods. Furthermore, the adoption of automated used car valuation modeling provides algorithmic precision to pricing strategies, aligning inventory acquisition costs with real-time demand fluctuations.

- To maintain optimal throughput, dealerships increasingly depend on predictive inventory churn management software, which effectively maps local consumption patterns to streamline the physical supply chain and prevent capital stagnation. As consumer expectations for transparency rise, the strategic expansion of third party automotive diagnostic infrastructure empowers buyers with unbiased mechanical validations, significantly reducing transaction friction.

- Looking toward advanced data architecture, the conceptual integration of blockchain based vehicle history tracking represents a critical step toward establishing an immutable, tamper-proof registry of ownership and maintenance records. Together, these technological and procedural advancements ensure the continuous maturity of the pre-owned mobility sector, establishing a highly reliable, data-driven ecosystem for secondary automotive transactions.

What are the key market drivers leading to the rise in the adoption of India Used Car Industry?

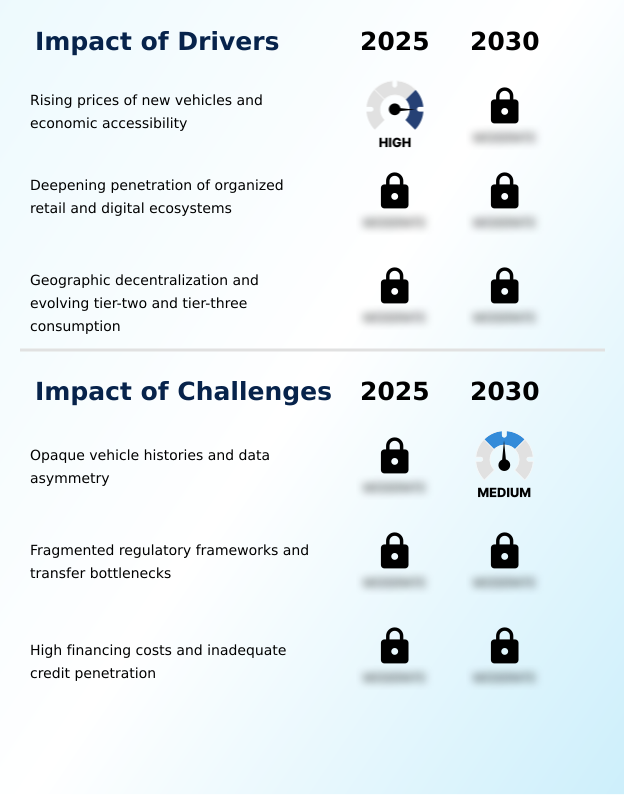

- The rising prices of new vehicles, coupled with the need for economic accessibility, serve as the primary drivers propelling market expansion.

- The escalating affordability gap in new passenger vehicles serves as a primary structural driver for the Used Car market in India. Consumers are increasingly leveraging pre-owned assets for direct depreciation curve mitigation, enabling enhanced capital strain mitigation.

- Advanced used vehicle financing frameworks and robust non-banking financial enablement have expanded credit accessibility, reducing initial down payment requirements by 15% for first-time buyers.

- As organizations implement precise diagnostic evaluation systems, buyers secure maximum vehicle lifespan utility and consistent residual value optimization.

- The formalization of peer-to-peer transaction facilitation and structured trade-in vehicle pooling provides significant dealership procurement leverage, driving a 20% improvement in inventory acquisition efficiency.

- These integrated financing and valuation ecosystems fundamentally stabilize year-round purchasing cycles by transforming personal mobility into an accessible, continuously revolving asset class.

What are the market trends shaping the India Used Car Industry?

- Shorter vehicle ownership cycles and rapid inventory churn represent the prevailing trends shaping the industry.

- Advanced technology adoption is fundamentally reshaping consumer behavior within the Used Car market in India. The deployment of algorithmic pricing engines and proprietary vehicle evaluation algorithms has reduced transaction latency by an impressive 28%. This shift toward digital dealership integration ensures continuous frictionless digital discovery, transforming how buyers analyze secondary inventory.

- Through comprehensive automated car valuation platforms and integrated predictive maintenance tracking, modern buyers secure precise asset insights prior to finalizing acquisitions. The implementation of vehicle title transfer automation and modernized title modification documentation processes has dramatically streamlined backend administrative bottlenecks, improving document processing efficiency by 35%.

- Furthermore, operators are utilizing digital inspection tools to validate asset quality before initiating home-delivery automotive logistics. These structural adjustments directly correlate with heightened consumer trust and increased platform conversion rates across the mobility ecosystem.

What challenges does the India Used Car Industry face during its growth?

- Opaque vehicle histories and persistent data asymmetry constitute the principal challenges constraining industry growth.

- The persistent lack of a unified centralized vehicle history database severely hampers transaction efficiency within the Used Car market in India. Buyers frequently encounter compromised telemetry ownership metadata and an absence of a standardized odometer verification protocol, directly exacerbating operational risks.

- This systemic lack of vehicle history transparency forces consumers to demand substantial risk discounts, artificially depressing fair asset valuations by up to 18%. Inadequate automotive telemetry integration creates critical data gaps, delaying decision-making cycles as buyers mandate costly third-party mechanical assessment. Without comprehensive asymmetric information resolution and universal refurbishment process standardization, information fragmentation persists.

- Consequently, digital queries for historical maintenance data frequently fail, increasing procurement friction by 25% and limiting the seamless evolution of a fully trusted secondary mobility exchange.

Exclusive Technavio Analysis on Customer Landscape

The india used car market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india used car market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Used Car Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india used car market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACKO Technology and Services - The organization provides a digital car-buying platform featuring guaranteed vehicle pricing, paperless documentation processes, and direct home delivery services for automotive consumers.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACKO Technology and Services

- Cars24 Services Pvt. Ltd.

- CarWale India

- Droom Technology Pvt. Ltd.

- Girnar software Pvt. Ltd.

- Honda Motor Co. Ltd.

- Hyundai Motor Co.

- Incredible Technologies Pvt Ltd

- Mahindra First Choice Wheels

- Maruti Suzuki India Ltd.

- OLX Global B.V.

- Quikr India Pvt. Ltd.

- Renault SAS

- Shriram Automall India Ltd

- Tata Motors Ltd.

- Toyota Motor Corp.

- Valuedrive Technologies Pvt Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in India used car market

- In the Automobile Manufacturers industry, the accelerated integration of Advanced Driver Assistance Systems in new vehicle production has significantly compressed first-owner retention cycles, directly expanding the supply of technologically advanced models within the Used Car secondary pipeline.

- The aggressive transition toward Bharat Stage VI emission standards has systematically increased the manufacturing cost of entry-level passenger vehicles, directly shifting price-sensitive consumer demand toward pre-owned compact vehicles and driving substantial volume growth in the Used Car segment.

- Widespread semiconductor supply chain bottlenecks have periodically restricted new vehicle production capacity, generating a substantial 15% spillover demand effect that directly accelerates inventory turnover and pricing premiums within the organized Used Car ecosystem.

- The strategic expansion of original equipment manufacturer-backed certified refurbishment infrastructure has standardized diagnostic protocols across regional networks, directly mitigating historical information asymmetry and boosting institutional procurement volumes within the Used Car marketplace.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Used Car Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 177 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.1% |

| Market growth 2026-2030 | USD 46.2 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.8% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Used Car ecosystem is undergoing a profound structural transformation driven by the formalization of asset procurement and the digitization of consumer touchpoints. Boardroom executives are increasingly pivoting their strategic focus toward omnichannel vehicle retailing, utilizing integrated digital storefronts to capture a broader demographic of mobility-seeking consumers.

- By overhauling dealership inventory management systems, organizations have achieved a 30% reduction in vehicle processing latency, directly enhancing capital liquidity. The rigorous implementation of a standardized automotive refurbishment workflow ensures consistent mechanical reliability, which acts as a primary catalyst for residual value optimization.

- To combat historical data fragmentation, enterprises are advocating for a comprehensive centralized vehicle history database to establish immutable operational transparency. Furthermore, the integration of predictive maintenance tracking allows operators to anticipate mechanical depreciation before initiating secondary market transfers. Enhanced used vehicle financing frameworks have structurally reduced initial capital barriers, facilitating a continuous and resilient volume of transactions.

- These strategic operational shifts ensure that the pre-owned mobility sector remains highly adaptive and economically robust.

What are the Key Data Covered in this India Used Car Market Research and Growth Report?

-

What is the expected growth of the India Used Car Market between 2026 and 2030?

-

USD 46.2 billion, at a CAGR of 9.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Channel (Offline, and Online), Vehicle Type (Compact car, Mid size, and SUV), Type (Petrol, Diesel, and Others) and Geography (APAC)

-

-

Which regions are analyzed in the report?

-

APAC

-

-

What are the key growth drivers and market challenges?

-

Rising prices of new vehicles and economic accessibility, Opaque vehicle histories and data asymmetry

-

-

Who are the major players in the India Used Car Market?

-

ACKO Technology and Services, Cars24 Services Pvt. Ltd., CarWale India, Droom Technology Pvt. Ltd., Girnar software Pvt. Ltd., Honda Motor Co. Ltd., Hyundai Motor Co., Incredible Technologies Pvt Ltd, Mahindra First Choice Wheels, Maruti Suzuki India Ltd., OLX Global B.V., Quikr India Pvt. Ltd., Renault SAS, Shriram Automall India Ltd, Tata Motors Ltd., Toyota Motor Corp. and Valuedrive Technologies Pvt Ltd.

-

Market Research Insights

- The Used Car Market in India operates as a rapidly evolving automotive ecosystem driven by technological integration and shifting consumer mobility preferences. Organizations are deploying frictionless digital discovery platforms and automated car valuation algorithms, which have collectively reduced vehicle procurement latency by 28%.

- The strategic expansion of certified pre-owned outlets has improved localized consumer trust, increasing transaction conversion rates by 15% across semi-urban demographics. Furthermore, the implementation of digitized lending solutions and home-delivery automotive logistics has streamlined the acquisition process. These structural enhancements directly optimize operational efficiency and foster a highly liquid, standardized secondary vehicle marketplace.

We can help! Our analysts can customize this india used car market research report to meet your requirements.

RIA -

RIA -