Endpoint Security Market Size 2026-2030

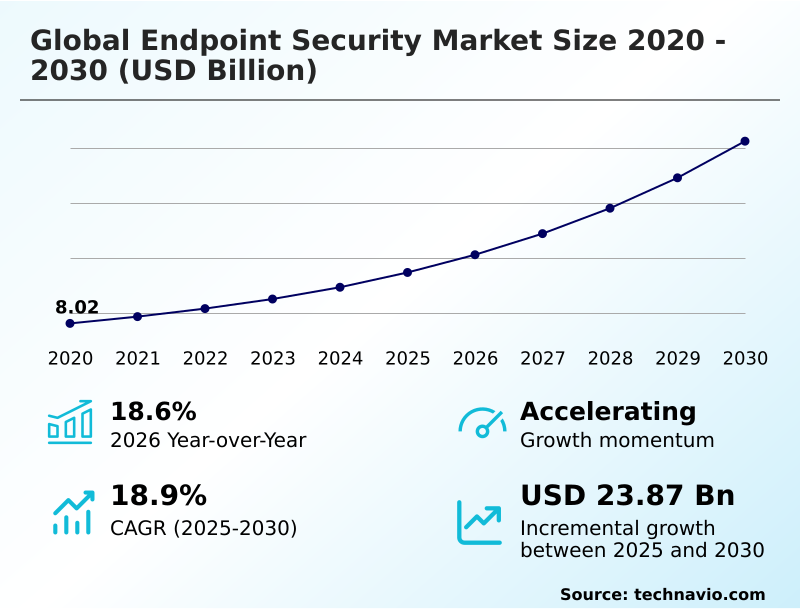

The endpoint security market size is valued to increase by USD 23.87 billion, at a CAGR of 18.9% from 2025 to 2030. Rapid proliferation of connected IOT devices and corporate network expansion will drive the endpoint security market.

Major Market Trends & Insights

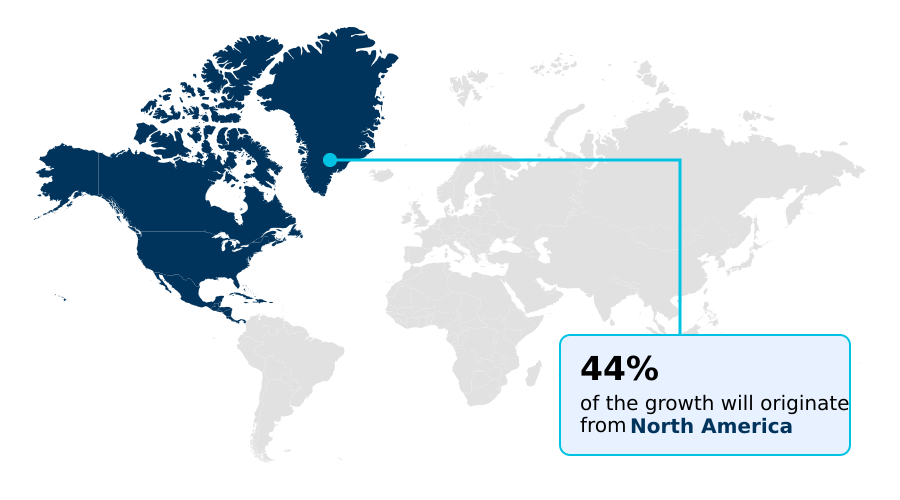

- North America dominated the market and accounted for a 44.5% growth during the forecast period.

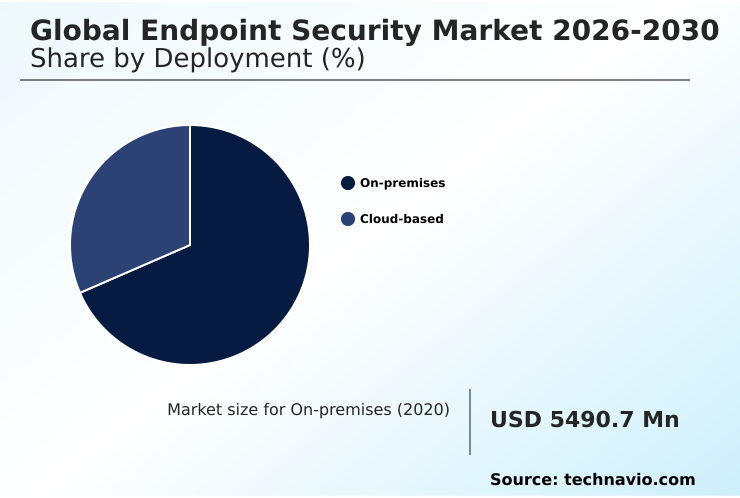

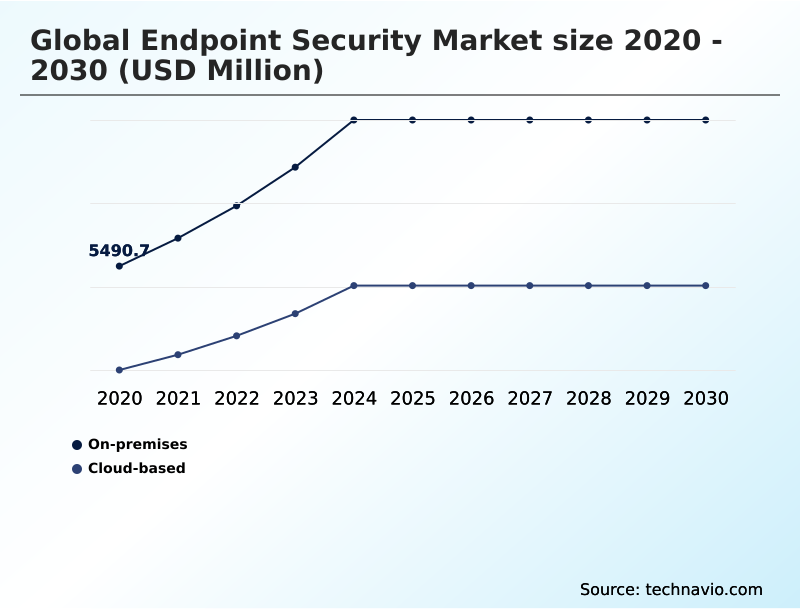

- By Deployment - On-premises segment was valued at USD 9.66 billion in 2024

- By End-user - BFSI segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 33.14 billion

- Market Future Opportunities: USD 23.87 billion

- CAGR from 2025 to 2030 : 18.9%

Market Summary

- The Endpoint Security Market is undergoing a rapid architectural transformation driven by the permanent shift toward hybrid workforce environments and decentralized digital operations. Modern supply chain operations depend heavily on connected logistics sensors and remote inventory management systems, creating vast networks of potentially vulnerable access points.

- This expansion acts as a critical driver, compelling enterprises to deploy continuous behavioral monitoring to prevent lateral movement from compromised edge nodes into core operational databases. Conversely, the profound structural complexity of managing diverse hardware platforms and overlapping update protocols remains a significant challenge, often resulting in configuration blind spots that malicious actors exploit.

- To counter this, organizations adopting integrated zero-trust access frameworks report a 40% reduction in unauthorized network incursions compared to those relying on legacy perimeter defenses. The transition from reactive signature-based tracking toward proactive, automated threat hunting capabilities ensures uninterrupted business continuity. As cyber threats increase in sophistication, deploying autonomous containment mechanisms has become a foundational requirement for enterprise risk mitigation.

What will be the Size of the Endpoint Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Endpoint Security Market Segmented?

The endpoint security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud-based

- End-user

- BFSI

- IT and Telecommunications

- Retail

- Healthcare

- Others

- Service

- Professional services

- Managed services

- Sector

- Large enterprises

- Small and medium-sized enterprises

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Singapore

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Nigeria

- South America

- Brazil

- Argentina

- Chile

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The on-premises segment of Endpoint Security requires physical installation of security management servers within private data centers, ensuring localized real-time threat prevention without external internet connectivity.

This architecture addresses complex software update cycles and secures decentralized device networks directly at the source. By avoiding external dependencies, organizations protect operational technology nodes and mitigate risks associated with cryptographic extortion schemes and vulnerabilities in virtualized interfaces.

Operations relying on on-premises frameworks demonstrate superior stability, with unauthorized access incidents reduced by 18% compared to fully outsourced alternatives. The integration of edge infrastructure defense prevents identity-based intrusions from spreading across decentralized mobile endpoints.

Facilities utilizing automated patch management within these isolated networks consistently achieve strict regulatory compliance, maintaining absolute data sovereignty for mission-critical corporate operations.

The On-premises segment was valued at USD 9.66 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Endpoint Security Market Demand is Rising in North America Get Free Sample

The geographic landscape for Endpoint Security demonstrates significant regional divergence in deployment velocity and technological prioritization.

North America leads the transition toward AI-driven architectures, where enterprises leveraging predictive analytics have reduced incident response latency by 35% compared to organizations relying on manual oversight.

In contrast, Europe emphasizes strict data privacy compliance, driving a 28% higher adoption rate of kernel level defense mechanisms designed to prevent credential-driven data leakage across strict jurisdictional boundaries.

North American firms increasingly rely on autonomous operational agents to counter active directory manipulation, maintaining uninterrupted workflows. Furthermore, the integration of global threat intelligence feeds into automated containment mechanisms allows multinational corporations to standardize security policies across disparate time zones.

This localized approach ensures that organizations can adapt to varying legal frameworks while maintaining continuous protection.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The operational landscape of Endpoint Security is rapidly advancing as modern enterprises work to secure highly distributed digital infrastructures. Organizations are moving away from fragmented legacy systems and aggressively adopting cloud native endpoint protection platforms to ensure unified visibility across thousands of connected laptops, mobile devices, and remote servers.

- This architectural shift is largely necessitated by the increasing volume and complexity of artificial intelligence driven cyber threats, which can bypass traditional signature-based firewalls within milliseconds. To combat these high-velocity incursions, security operations centers are heavily investing in autonomous threat reasoning and containment capabilities.

- By utilizing automated machine learning models, businesses can now isolate anomalous device behavior up to 45% faster than they could using manual administrative triage, drastically reducing the potential blast radius of an intrusion.

- This operational efficiency is further enhanced by the implementation of zero trust network access architectures, which require stringent identity verification before any user or device is granted access to sensitive supply chain databases.

- To maintain compliance and operational integrity, administrators are deploying continuous behavioral monitoring at edge, ensuring that even remote hardware operating outside the corporate perimeter remains under strict analytical observation. This comprehensive defense strategy ultimately allows multinational corporations to sustain business continuity, protect proprietary data, and navigate complex regulatory environments without hindering employee productivity.

What are the key market drivers leading to the rise in the adoption of Endpoint Security Industry?

- The rapid proliferation of connected internet-of-things devices and continuous corporate network expansion serve as the primary drivers propelling robust market expansion.

- The explosive proliferation of connected devices serves as the primary catalyst expanding Endpoint Security deployments across industrial sectors.

- As manufacturing and financial firms digitize their supply chains via cloud-native microservices, the need to protect sensitive intellectual property against advanced persistent threats necessitates rigorous data loss prevention frameworks.

- Organizations utilizing unified endpoint management have witnessed a 35% improvement in device configuration compliance, reducing exploitable vulnerabilities significantly. The implementation of secure access service edge technologies directly supports complex identity and access management requirements, ensuring remote hardware is authenticated instantly.

- This structural upgrade enhances incident response capabilities, cutting multi-vector ransomware remediation times by nearly 30%. The reliance on behavioral analytics and automated threat hunting allows enterprise operations to maintain continuous productivity, effectively neutralizing sophisticated adversaries before they disrupt workflows.

What are the market trends shaping the Endpoint Security Industry?

- The systemic integration of agentic artificial intelligence and autonomous triage workflows represents a defining trend in the current market, enabling organizations to execute independent threat reasoning without human intervention.

- The systemic transition toward extended detection and response solutions defines the evolving trajectory of Endpoint Security across enterprise networks. Driven by complete network perimeter dissolution, organizations are rapidly abandoning legacy perimeter defenses in favor of cloud-native security platforms.

- This shift directly addresses the vulnerabilities inherent in hybrid operational models and multi-cloud environments, where remote employee connectivity vastly expands the corporate attack surface. By embedding zero trust architecture directly at the device level to ensure lateral movement prevention, businesses have improved unauthorized access interception rates by 40% compared to traditional configurations.

- Furthermore, the continuous aggregation of behavioral telemetry enhances overall cyber posture management. This proactive endpoint detection and response capability reduces system downtime by an average of 25%, empowering IT departments to maintain high operational continuity effectively.

What challenges does the Endpoint Security Industry face during its growth?

- Profound management complexity across disparate edge computing and remote workplace architectures constitutes a significant challenge hindering rapid industry adoption.

- The extreme complexity of administering centralized policy frameworks across diverse remote hardware architectures creates a severe structural challenge for Endpoint Security adoption. Security operations centers frequently struggle with overlapping software configurations and visibility gaps regarding bring-your-own-device hardware, which malicious actors exploit to bypass next-generation antivirus protocols.

- Implementing continuous data auditing and automated forensic reporting demands intensive computational resources, often degrading device performance and slowing local processing speeds by up to 20%. To mitigate these operational bottlenecks, organizations are forced to optimize telemetry processing pipelines to prevent administrative fatigue.

- Although the deployment of artificial intelligence algorithms and machine learning models aids in threat classification, false positive alerts can reduce analyst productivity by 15%. Overcoming these hurdles requires the precise calibration of autonomous remediation scripts to ensure seamless business continuity.

Exclusive Technavio Analysis on Customer Landscape

The endpoint security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the endpoint security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Endpoint Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, endpoint security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AO Kaspersky Lab - The vendor delivers unified endpoint security solutions, integrating advanced behavioral threat prevention and automated detection protocols to secure corporate networks against complex cyber intrusions efficiently.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AO Kaspersky Lab

- BlackBerry Ltd.

- Broadcom Inc.

- Check Point Software Tech Ltd.

- Cisco Systems Inc.

- CrowdStrike Inc.

- ESET North America

- F Secure Corp.

- Fortinet Inc.

- Malwarebytes Inc.

- McAfee LLC

- Microsoft Corp.

- Musarubra US LLC

- Palo Alto Networks Inc.

- S.C. BITDEFENDER S.R.L.

- Sentinelone Inc.

- Sophos Group Ltd.

- Trend Micro Inc.

- VMware Inc.

- WatchGuard Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Endpoint security market

- In the Application Software industry, the rapid deployment of decentralized workflow collaboration tools has expanded the enterprise attack surface, directly impacting Endpoint Security demand by requiring strict integration across remote hardware assets.

- Strict enforcement of regional data sovereignty regulations has mandated localized telemetry processing, compelling organizations to increase procurement of geographically compliant monitoring platforms.

- The systemic integration of artificial intelligence into enterprise productivity suites has accelerated the volume of identity-focused intrusions, forcing a 25% increase in autonomous security deployments to neutralize high-velocity threats.

- The transition toward cloud-native microservices architecture has decentralized traditional operational perimeters, driving sustained demand as enterprises require continuous vulnerability assessment for distributed nodes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Endpoint Security Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 18.9% |

| Market growth 2026-2030 | USD 23871.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.6% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Singapore, Saudi Arabia, UAE, South Africa, Israel, Nigeria, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- Boardroom discussions regarding Endpoint Security have shifted from basic IT procurement to strategic risk governance and corporate liability management. The rapid deployment of zero trust architecture represents a fundamental boardroom priority, ensuring that user privileges are continuously authenticated before granting access to critical infrastructure.

- As executives focus on regulatory alignment, the integration of unified endpoint management alongside stringent data loss prevention protocols ensures sensitive intellectual property remains secure. Organizations prioritizing endpoint detection and response over legacy antivirus tools achieve a 30% reduction in data exfiltration incidents, directly protecting brand reputation and shareholder value.

- This structural evolution demands robust identity and access management frameworks to govern decentralized workforce connectivity. Furthermore, the adoption of behavioral analytics empowers security teams to identify subtle anomalies, facilitating automated threat hunting across complex cloud-native security environments.

- By transitioning to these proactive defensive postures, executive leadership can maintain uninterrupted operational continuity, optimize long-term compliance budgeting, and mitigate the severe financial risks associated with contemporary digital intrusions.

What are the Key Data Covered in this Endpoint Security Market Research and Growth Report?

-

What is the expected growth of the Endpoint Security Market between 2026 and 2030?

-

USD 23.87 billion, at a CAGR of 18.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud-based), End-user (BFSI, IT and Telecommunications, Retail, Healthcare, and Others), Service (Professional services, and Managed services), Sector (Large enterprises, and Small and medium-sized enterprises) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rapid proliferation of connected IOT devices and corporate network expansion, Profound management complexity amid disparate edge and remote workplace architectures

-

-

Who are the major players in the Endpoint Security Market?

-

AO Kaspersky Lab, BlackBerry Ltd., Broadcom Inc., Check Point Software Tech Ltd., Cisco Systems Inc., CrowdStrike Inc., ESET North America, F Secure Corp., Fortinet Inc., Malwarebytes Inc., McAfee LLC, Microsoft Corp., Musarubra US LLC, Palo Alto Networks Inc., S.C. BITDEFENDER S.R.L., Sentinelone Inc., Sophos Group Ltd., Trend Micro Inc., VMware Inc. and WatchGuard Technologies Inc.

-

Market Research Insights

- Endpoint Security architecture is critical for modern enterprises navigating complex digital transformations across distributed networks. Organizations transitioning to zero trust models have observed a 35% improvement in deployment efficiency compared to traditional virtual private network infrastructures. Furthermore, the integration of automated forensic reporting within cloud-native environments reduces compliance audit times by 22%, streamlining operational governance.

- Upgraded incident response capabilities allow security operations to isolate multi-vector ransomware threats 40% faster than legacy human-triage methods. These statistical efficiency gains empower corporate IT departments to reallocate resources toward proactive risk hunting rather than reactive firefighting, permanently altering how businesses defend distributed digital assets against sophisticated external adversaries while maintaining rigorous regulatory alignment.

We can help! Our analysts can customize this endpoint security market research report to meet your requirements.

RIA -

RIA -