Dental Equipment Market Size 2026-2030

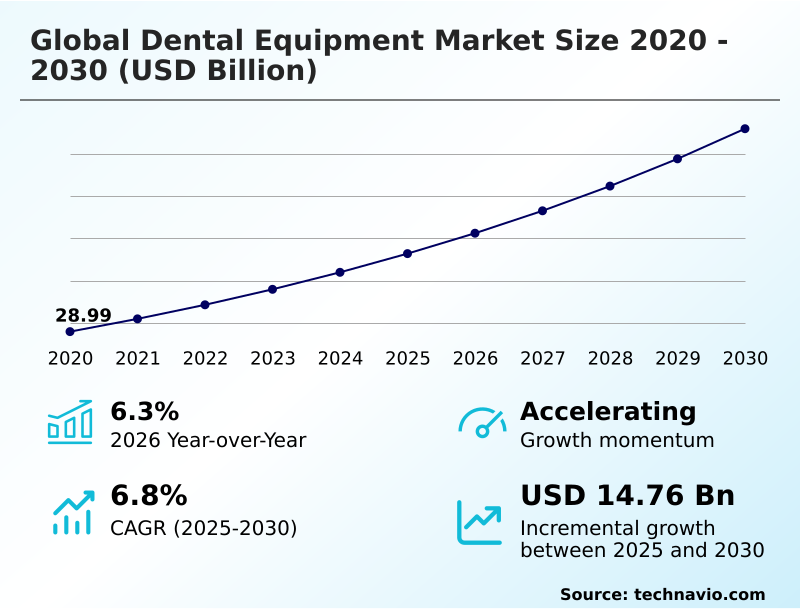

The dental equipment market size is valued to increase by USD 14.76 billion, at a CAGR of 6.8% from 2025 to 2030. Technological advancements and digital transformation of dentistry will drive the dental equipment market.

Major Market Trends & Insights

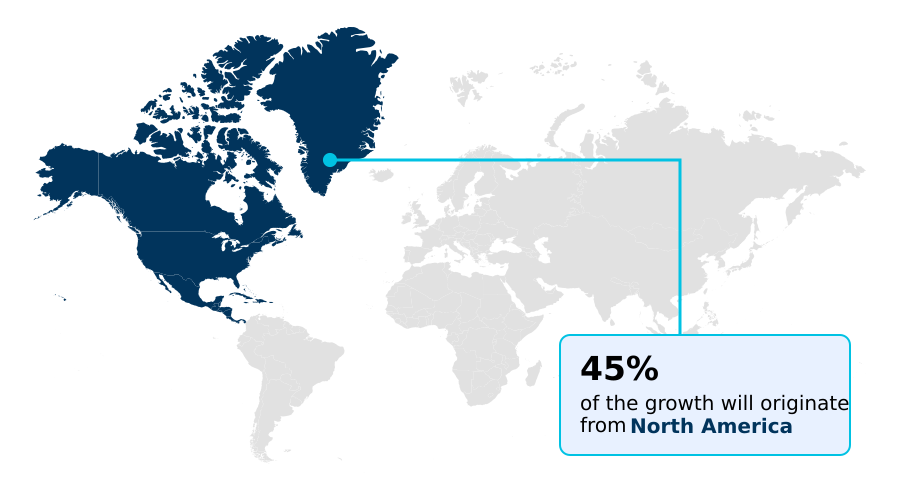

- North America dominated the market and accounted for a 45.1% growth during the forecast period.

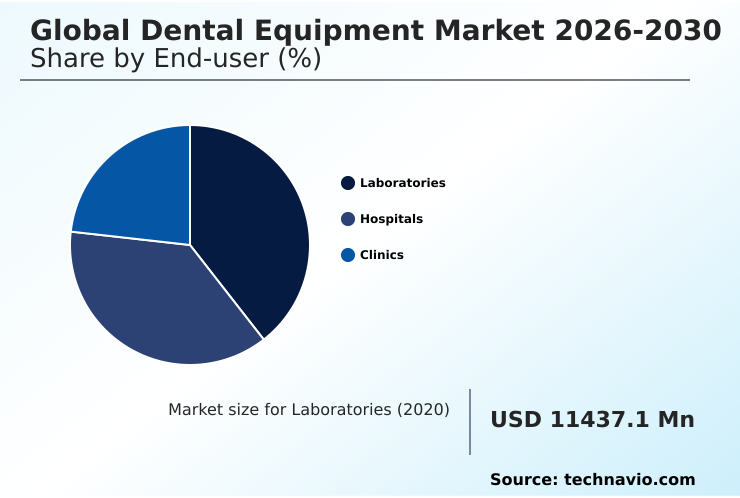

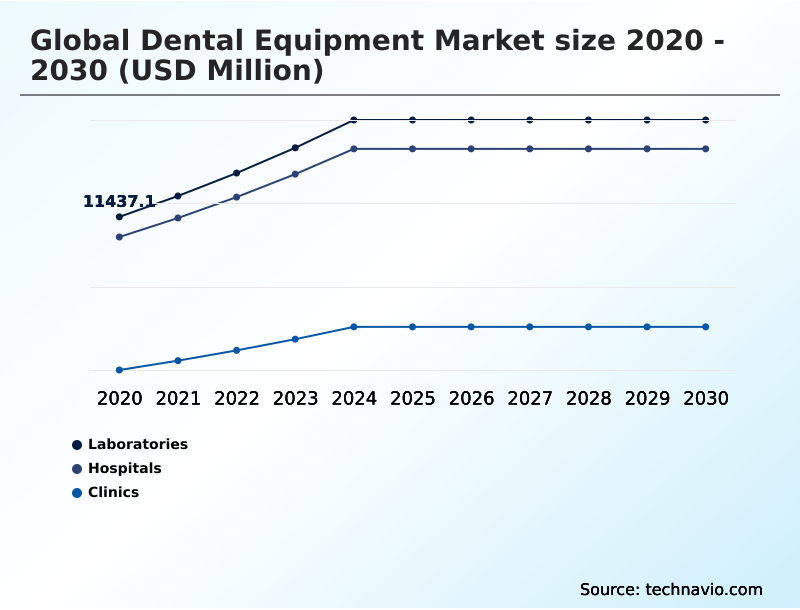

- By End-user - Laboratories segment was valued at USD 14.41 billion in 2024

- By Product - Dental diagnostics and surgical equipment segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 23.98 billion

- Market Future Opportunities: USD 14.76 billion

- CAGR from 2025 to 2030 : 6.8%

Market Summary

- The Dental Equipment market demonstrates robust expansion driven by the rapid transition toward digitized clinical ecosystems and increasing demand for minimally invasive interventions. Technological advancements, specifically the integration of artificial intelligence machines and automated radiographic image pathology detection, serve as a primary driver by significantly improving diagnostic accuracy and accelerating treatment planning.

- Conversely, the high acquisition costs of advanced hardware and stringent regulatory compliance protocols pose a substantial challenge, limiting accessibility for smaller independent practitioners. In real-world operational scenarios, large dental service organizations leverage centralized procurement strategies to standardize digital radiography systems and practice management software across multi-site networks.

- This consolidation approach allows corporate networks to achieve up to a 20% improvement in equipment utilization rates compared to fragmented solo practices. By investing in sophisticated intraoral scanners and advanced biomimetic materials, practitioners can execute same-day restorative workflows, thereby elevating clinical throughput and minimizing patient chair time.

- This systemic evolution ensures higher care standards while demanding continuous capital investment in state-of-the-art diagnostic and surgical infrastructure.

What will be the Size of the Dental Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Dental Equipment Market Segmented?

The dental equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Laboratories

- Hospitals

- Clinics

- Product

- Dental diagnostics and surgical equipment

- Dental consumables

- Dental laser

- Application

- Solo practices

- DSO or group practices

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Italy

- Spain

- The Netherlands

- Asia

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Rest of World (ROW)

- North America

By End-user Insights

The laboratories segment is estimated to witness significant growth during the forecast period.

The laboratories segment within the Dental Equipment space is undergoing a profound structural evolution, fundamentally driven by the replacement of traditional analog processes with integrated digital methodologies.

This transition involves the accelerated adoption of intraoral scanners, computer aided design software, and chairside milling units to fabricate prosthetics with superior precision.

The integration of advanced ceramic blocks and high performance polymer pucks into these environments allows technicians to handle complex cases more efficiently.

By fully adopting digital impression systems and advanced radiographic image analysis, production centers have achieved a 25% reduction in manual adjustment times.

This efficiency gain directly stems from optimized clinical workflows and streamlined communication between clinics and technicians, ultimately elevating the quality of minimally invasive treatment and complex periodontal therapy while maximizing operational throughput.

The Laboratories segment was valued at USD 14.41 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dental Equipment Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Dental Equipment sector reveals stark contrasts in technology adoption and supply chain maturity, particularly between North America and APAC.

North America maintains a dominant position, driven by corporate networks that leverage data analytics technologies and fog computing to standardize equipment procurement.

Clinics in the United States and Canada utilizing advanced surgical navigation systems and teledentistry platforms have increased in-house restorative production by 35% compared to traditional outsourcing. Conversely, the market in APAC is experiencing accelerated modernization due to rising dental tourism.

Facilities in APAC upgrading their prosthetic solutions and regenerative dentistry solutions report a 20% improvement in patient throughput.

While North America focuses on integrating augmented reality systems to enhance clinical precision and osseointegration success rates, APAC prioritizes expanding baseline access to advanced surgical equipment, reflecting divergent regional strategies in capitalizing on digital advancements.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous evolution of the Dental Equipment sector is heavily reliant on the seamless integration of sophisticated hardware and intelligent software solutions. Practitioners are increasingly prioritizing advanced digital imaging systems integration to streamline diagnostic workflows and enhance communication with external laboratories.

- This technological pivot allows large corporate dental networks to achieve a 25% faster turnaround time for prosthetic fabrications compared to clinics relying on conventional analog impressions. The utilization of in office computer aided design fabrication empowers clinicians to deliver immediate restorative treatments, optimizing supply chain logistics by reducing dependence on third-party manufacturers.

- Furthermore, the deployment of automated radiographic image pathology detection software mitigates diagnostic variability, ensuring consistent and predictable clinical outcomes across diverse practice environments. By leveraging three dimensional anatomical data reconstruction, oral surgeons can execute complex implant procedures with unprecedented accuracy, minimizing postoperative complications.

- Additionally, the rising consumer preference for aesthetic enhancements has driven the adoption of specialized lasers for minimally invasive soft tissue contouring, reducing patient recovery periods and improving overall satisfaction.

- These interconnected advancements demonstrate how the strategic implementation of digital dentistry not only elevates the standard of patient care but also drives operational resilience, cost efficiency, and competitive differentiation within a highly dynamic healthcare landscape.

What are the key market drivers leading to the rise in the adoption of Dental Equipment Industry?

- Technological advancements and the digital transformation of dentistry serve as primary market drivers.

- The relentless technological advancement and the digital transformation of clinical protocols serve as the primary catalysts propelling the Dental Equipment sector.

- The critical need for precise interventions has driven the widespread adoption of diode lasers and erbium lasers for tissue management. By implementing these advanced therapeutic devices alongside accurate caries detection devices, clinics report a 30% reduction in patient recovery times.

- Additionally, the integration of bioactive materials and biomimetic materials within connected product ecosystems enhances the longevity of restorative work. This shift enables dental organizations to standardize workflows using smart sensors and artificial intelligence machines, lowering long-term operational costs by 18%.

- The continuous refinement of dental air purification systems ensures alignment with value based care objectives, allowing practitioners to deliver highly durable, safe solutions that sustain demand for advanced hardware.

What are the market trends shaping the Dental Equipment Industry?

- The rise of teledentistry platforms and remote dental consultations represents an upcoming trend.

- The prominent trend shaping the Dental Equipment landscape is the rapid acceleration of additive manufacturing and the implementation of virtual care models. As patient expectations shift toward immediate care, practices are integrating three dimensional printing and clear aligner therapy workflows to bring prosthetic fabrication in-house.

- This strategic shift reduces reliance on external laboratories, thereby decreasing component delivery delays by up to 40%. Concurrently, the deployment of remote dental consultations via high-resolution diagnostic cameras allows clinical networks to triage cases efficiently, improving scheduling accuracy by 25%. By leveraging specialized photopolymer resins for customized surgical guides and anatomical models, practitioners achieve superior predictability.

- This modernization trend, deeply integrated with practice management software and electronic health records, fundamentally redefines operational logistics, lowering external expenditures and expanding clinical capacity alongside cone beam computed tomography capabilities.

What challenges does the Dental Equipment Industry face during its growth?

- The high cost of equipment and financial barriers to entry pose key challenges.

- The substantial capital requirements and complex integration hurdles act as significant challenges constraining the rapid expansion of the Dental Equipment sector. Transitioning to a digital environment demands heavy upfront investments in carbon dioxide lasers, sophisticated endodontic motors, and robust computer aided manufacturing platforms.

- For smaller clinics, these financial barriers often delay the acquisition of advanced digital radiography systems and ultrasonic scalers, leading to a 20% gap in operational efficiency compared to heavily capitalized networks. Furthermore, achieving seamless cross device connectivity and adapting to cloud based delivery models require intensive staff training and continuous application re engineering.

- Implementing stringent sterilization protocols and comprehensive infection control protocols frequently causes workflow disruptions, initially reducing daily patient throughput by 15% and highlighting the operational difficulties practitioners face during technological modernization.

Exclusive Technavio Analysis on Customer Landscape

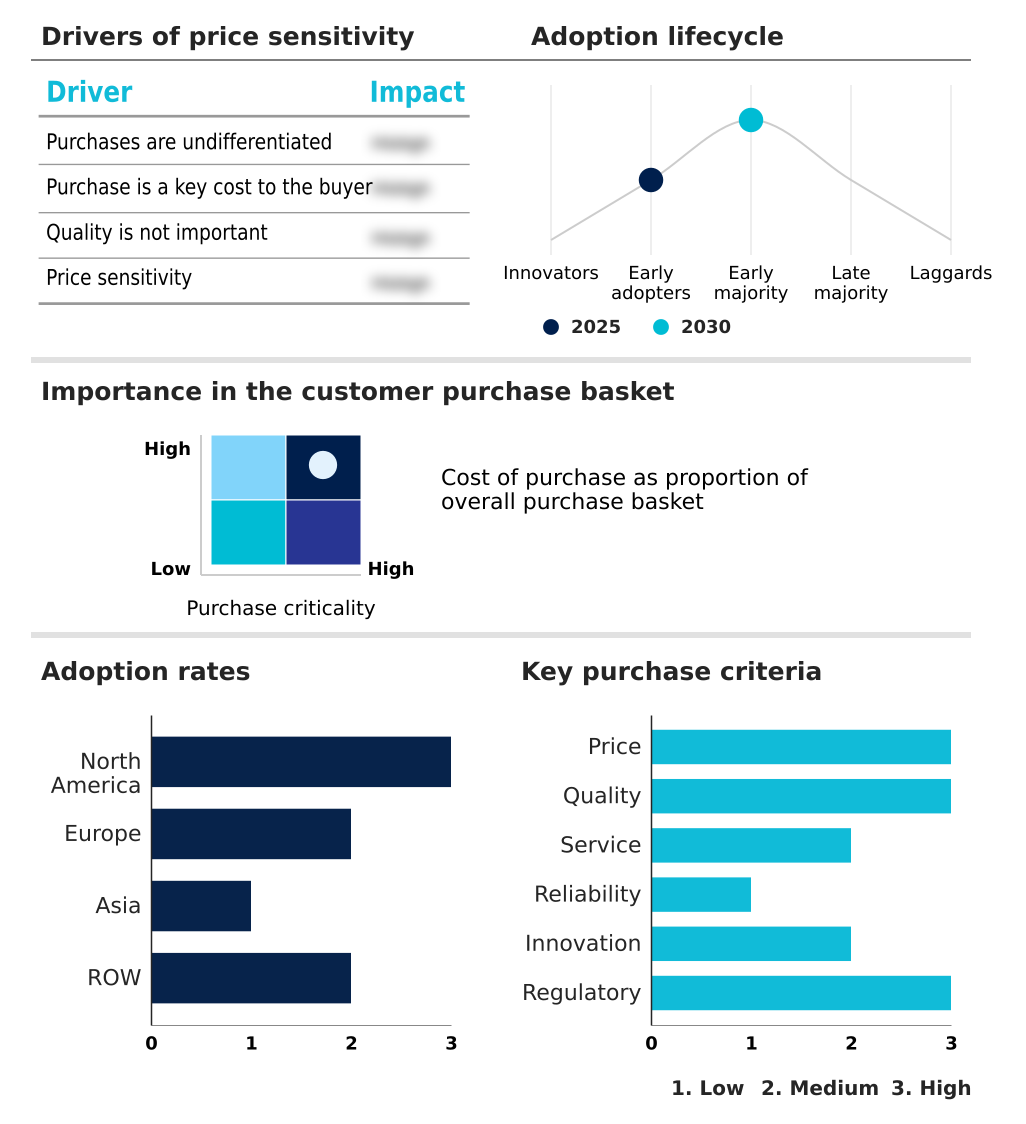

The dental equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dental equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Dental Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dental equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3Shape AS - Provides advanced intraoral scanners, design software, and digital impression systems to enhance clinical workflows and improve restorative precision for modern dental professionals.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3Shape AS

- A dec Inc.

- ACTEON Group

- Air Techniques Inc.

- Align Technology Inc.

- BEGO GmbH and Co. KG

- Bien Air Dental SA

- Carestream Dental LLC

- DentalEZ Inc.

- Dentsply Sirona Inc.

- Envista Holdings Corp.

- GC Corp.

- GENORAY Co. Ltd.

- Institut Straumann AG

- Ivoclar Vivadent AG

- KaVo Dental GmbH

- Midmark Corp.

- Morita Holdings Corp.

- VATECH America Inc

- W and H

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dental equipment market

- In the Health Care Equipment industry, the widespread adoption of AI-driven diagnostic imaging software has automated pathology detection, directly impacting Dental Equipment demand by necessitating the integration of compatible cone beam computed tomography devices in clinical workflows.

- The implementation of stringent infection control protocols for medical device sterilization has driven the transition toward advanced dental air purification systems and upgraded autoclaves within modern operative settings.

- The shift toward minimally invasive treatment paradigms has accelerated the utilization of highly precise surgical navigation systems, significantly influencing the procurement of erbium lasers and diode lasers for hard and soft tissue applications.

- The expansion of cloud based delivery models for electronic health records has facilitated seamless cross device connectivity, pulling demand for smart sensors and teledentistry platforms that enable remote clinical consultations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dental Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.8% |

| Market growth 2026-2030 | USD 14762.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.3% |

| Key countries | US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Argentina, South Africa, Turkey, Colombia and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Dental Equipment sector represents a critical frontier in modern healthcare technology, characterized by the widespread transition from analog procedures to fully integrated digital ecosystems. The deployment of high-resolution intraoral scanners and computer aided design software enables practitioners to eliminate traditional impression materials, dramatically increasing procedural accuracy.

- When combined with computer aided manufacturing and state-of-the-art chairside milling units, clinical facilities can execute same-day restorative treatments, driving a 30% reduction in overall treatment timelines compared to conventional multi-visit approaches. This shift toward digital dentistry necessitates substantial investments in photopolymer resins and advanced ceramic blocks to ensure durable and aesthetically pleasing prosthetic solutions.

- Furthermore, the integration of teledentistry platforms facilitates robust remote triage and monitoring capabilities, directly optimizing clinical scheduling and resource allocation. As regulatory requirements for infection control tighten, the strategic acquisition of these advanced technologies allows dental organizations to maintain compliance while simultaneously enhancing patient throughput, solidifying the vital role of sophisticated diagnostic and surgical infrastructure in modern clinical operations.

What are the Key Data Covered in this Dental Equipment Market Research and Growth Report?

-

What is the expected growth of the Dental Equipment Market between 2026 and 2030?

-

USD 14.76 billion, at a CAGR of 6.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Laboratories, Hospitals, and Clinics), Product (Dental diagnostics and surgical equipment, Dental consumables, and Dental laser), Application (Solo practices, DSO or group practices, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Technological advancements and digital transformation of dentistry, High cost of equipment and financial barriers to entry

-

-

Who are the major players in the Dental Equipment Market?

-

3Shape AS, A dec Inc., ACTEON Group, Air Techniques Inc., Align Technology Inc., BEGO GmbH and Co. KG, Bien Air Dental SA, Carestream Dental LLC, DentalEZ Inc., Dentsply Sirona Inc., Envista Holdings Corp., GC Corp., GENORAY Co. Ltd., Institut Straumann AG, Ivoclar Vivadent AG, KaVo Dental GmbH, Midmark Corp., Morita Holdings Corp., VATECH America Inc and W and H

-

Market Research Insights

- The Dental Equipment market is characterized by the rapid adoption of digital impression systems and advanced data analytics technologies that streamline clinical workflows. Dental practices deploying connected product ecosystems experience a 30% reduction in diagnostic processing times compared to traditional analog methods.

- Furthermore, the integration of value based care models has incentivized the adoption of remote dental consultations, expanding patient access while decreasing non-critical in-person visits by 15%. Implementing rigorous sterilization protocols and cross device connectivity allows multi-specialty clinics to enhance operational efficiency by 22%.

- These measurable improvements highlight how modern diagnostic tools and management software optimize resource allocation, lower overhead costs, and elevate the overall standard of patient care.

We can help! Our analysts can customize this dental equipment market research report to meet your requirements.

RIA -

RIA -